Save life

-

So far in our discussion on blockchain, we’ve touched on a number of topics including exactly what makes blockchain transactions immutable and how blockchain technology can provide trust between parties involved in a financial transaction.

So far in our discussion on blockchain, we’ve touched on a number of topics including exactly what makes blockchain transactions immutable and how blockchain technology can provide trust between parties involved in a financial transaction.

What we have yet to cover is if, and how, blockchain technology could disintermediate attorneys in transactions. This is where the concept of “smart contracts” comes in.

As we start to dig into this topic, it merits stating that, despite the name, a smart contract is not a contract in the traditional sense, nor does it replace same. A smart contract is a software program that “sits” on top of the blockchain and takes actions (e.g., posts transactions) on the blockchain based on certain data conditions that are detected in the blockchain. If that definition sounds vague to you, it’s because smart contracts can potentially serve many uses.

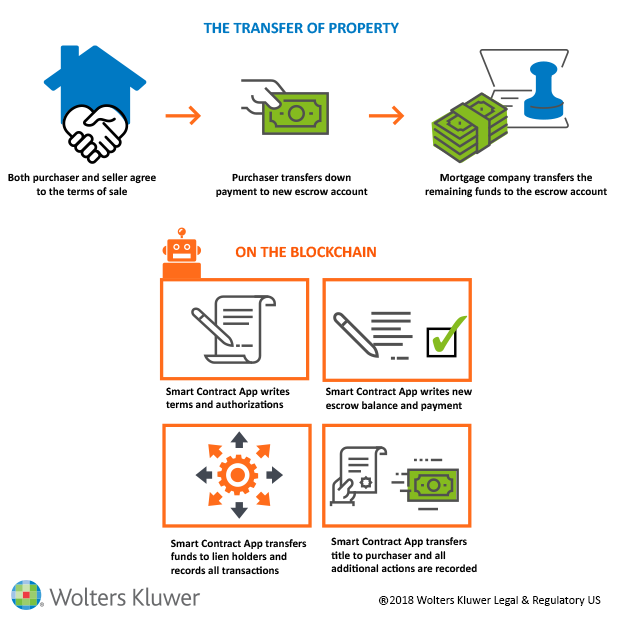

For the purpose of this article, we will continue to look the transfer of property example that we explored in last month’s article. In order for transfer of property to occur, the following things[1] have to happen (assuming purchase terms and conditions have already been agreed to)

:• The purchaser pays a portion (down payment) of the agreed upon funds for purchase.

• Assuming that the purchaser is borrowing funds, the mortgage company pays the remaining balance required for purchase.

• Purchase funds are used to clear outstanding liens (e.g., mortgages, unpaid taxes, etc.) on the property.

• Remaining purchase funds are distributed to the seller.

• Any requisite new liens (e.g., the purchaser’s mortgage) are added to the property.

• Title is transferred from the seller to the purchaser.

Given that the average purchase price of a new house in the U.S. is roughly $400K,[2] the funds associated with purchase are not insignificant — so it makes sense for each of the parties to look for a trusted intermediary, such as a closing attorney, to help facilitate the transaction.

The parties typically agree on a title company to prepare and file all required paperwork and (most importantly) to hold funds in escrow while each of the above steps are taken. This ensures, among other things, that the seller doesn’t simply abscond with the purchase funds and leave the purchaser with a lien-ridden property.

So how does the blockchain and the concept of smart contracts fit into such a transaction? To start, the necessary data to complete the transaction would all have to be stored in a single blockchain system.

At a minimum, a central, most likely government-owned system that includes property and lien records would have to exist. In addition, the system would need to be able to transfer payment between users through either some form of cryptocurrency or a more traditional automated clearing house-based (ACH) payment mechanism.

Assuming that all of the above were in place, then one could write a computer program (a smart contract) that would be capable of monitoring all of the data referenced above. In order to execute the transaction, the following steps would be required:

1. Both purchaser and seller agree to the terms of sale, input those terms into the smart contract, and digitally sign their acceptance. The smart contract application writes the terms and authorizations into a blockchain transaction.

2. At closing, the purchaser transfers down payment funds through the smart contract to the smart contract’s escrow account. The smart contract application writes the new escrow balance and the payment record into the blockchain.

3. Assuming that underwriting has been completed successfully (this is performed outside the system), the purchaser’s mortgage company transfers the remaining funds through the smart contract to the smart contract’s escrow account. The smart contract application writes the new escrow balance and the payment record into the blockchain.

At this point, the smart contract can see both the terms of the transaction and that payment has been made by the seller. Assuming that the payment meets the terms of the transaction, the smart contract can begin to process the remaining transaction items:

4. The smart contract application transfers funds to each lien holder, marks each lien record as closed, reduces the escrow balance appropriately, and records all actions as a transaction on the blockchain.

5. The smart contract application transfers the title to the purchaser, establishes a new lien for the mortgage company, transfers remaining funds to the seller, and records all actions as a transaction on the blockchain.

This hypothetical workflow illustrates the potential disintermediation of the closing attorney in a real estate transaction, but it should be noted that significant development of a property records system (most likely by a government agency) would be required to even contemplate such a workflow.

This example highlights the difference between potential and technical feasibility in a near-term scenario for blockchain technology in law… where implementing a smart contract, in terms of layering on the actual technology, is not the most complicated part.

The true challenge lies in all of the other aspects of the process — and the buy-in from existing governing bodies and institutions — that would have to fall into place to make this executable.

The potential, however, does raise many interesting questions: who would write such a smart contract application? How would that provider develop trust with the market? What would happen when things go wrong (e.g., if the seller knowingly failed to disclose a material defect in the property)?

These and other topics are currently under examination within our industry. Several groups are already making significant inroads and investment in exploring blockchain technology’s role in the practice of law.

More on that next month.[1] This of course is a simplistic view of the steps required in transfer of title, and is meant to serve as a high-level example to illustrate the potential role of a smart contract.

[1] U.S. Census figures, December 2017

May Goren Photography

Dean Sonderegger is Vice President & General Manager, Legal Markets and Innovation at Wolters Kluwer Legal & Regulatory U.S., a leading provider of information, business intelligence, regulatory and legal workflow solutions.

Dean has more than two decades of experience at the cutting edge of technology across industries. He can be reached at [email protected].

Discover more reports like this at Above Law here: https://abovethelaw.com/2018/02/blockchain-can-smart-contracts-replace-lawyers/-

- 2

Francisco Gimeno - BC Analyst When we follow up how Blockchain can change sectors in real life, one of the first ones to be listed is Law. We know some start ups trying to develop smart contracts and Dapps for the Law field. This article is one who really reflects on the difficulties for a new technology to be implemented. Recommended.

-

-

Starbucks is likely to utilize blockchain technology as part of a new payments app, executive chairman Howard Shultz said Tuesday. Speaking with Maria Bartiromo during a Fox Business segment, Schultz discussed the use of a "proprietary digital currency" in conjunction with the payments app.

Starbucks is likely to utilize blockchain technology as part of a new payments app, executive chairman Howard Shultz said Tuesday. Speaking with Maria Bartiromo during a Fox Business segment, Schultz discussed the use of a "proprietary digital currency" in conjunction with the payments app.

When asked whether the coffee retailer would use blockchain in conjunction with the initiative - as opposed to a more centralized system of accounting - Schultz said that the company "probably" would move in that direction."I think blockchain technology is probably the rails in which an integrated app at Starbucks will be sitting on top of," he commented.

His comments come roughly a month after the former chief executive spoke broadly during an earnings call about the chain's plans to utilize the tech, especially on the payments front (although he dismissed the idea that the company would use bitcoin in some way).

At the time, Schultz suggested that the tech may play a role in how Starbucks works to "expand digital customer relationships," though it remains to be seen how blockchain is ultimately used in practice by the company.

"I believe that we are heading into a new age, in which blockchain technology is going to provide a significant level of a digital currency that is going to have a consumer application," he remarked during the earnings call.

Image Credit: sitthiphong / Shutterstock.com

The leader in blockchain news, CoinDesk is an independent media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. Have breaking news or a story tip to send to our journalists? Contact us at [email protected].-

Francisco Gimeno - BC Analyst Starbucks focus on its Millennial customers here, experimenting how Blockchain could be used on the chain. Starbucks Coin? Or a token? and a payment App... nice.

-

-

Blockchain technology, Deep Learning, and Interplanetary File Systems? How can we merge all this cool new technology to create something useful and beautiful? Watch this talk to learn about the underlying technologies that can help create decentralized artificial intelligence.

Blockchain technology, Deep Learning, and Interplanetary File Systems? How can we merge all this cool new technology to create something useful and beautiful? Watch this talk to learn about the underlying technologies that can help create decentralized artificial intelligence.

EVENT:

EngineersSG 2018

SPEAKER:

Siraj Raval

PERMISSIONS:

The original video was published with the Creative Commons Attribution license (reuse allowed).

CREDITS:

Original video source: https://www.youtube.com/watch?v=zYKzs...-

Francisco Gimeno - BC Analyst A half an hour interesting talk about Decentralised Artificial Intelligence. Futuristic technology being debated now by those who are working on it.

-

-

By Akash Kasibhatla

Now, there are many practical applications of Blockchain, and it comes in more forms than just a currency. Blockchain can be used to secure healthcare records, secure data, prevent fraud, provide a secure social network, and of course provide education to the world.

In fact, there is a project that launched very recently that securely stores medical records through Blockchain technology. Hospitals, health insurers, and various other healthcare professionals can request permission to access the patients’ records and record transactions on the distributed ledger. The startup behind this, Medicalchain, has the fundamental goal to progress healthcare using Blockchain technology, and not to simply create a currency.The Issue of Inequality

It’s true that a global, decentralised currency could do wonders in the economic sphere. The potential economic effects of Blockchain are very interesting, but first, it is worth considering what the centralised system is doing. The top eight richest people hold as much wealth as the bottom 50% of people in the world. This is because of centralisation.

Corporations are politically centralised, architecturally centralised, and logically centralised. This results in a pyramid where the wealthy and powerful feed off of the masses.But, Blockchain can change that. It can raise the standard of living for people across the globe. Instead of redistributing wealth, could one instead change the way it is created in the first place?

Some of the possible ways are the Sharing Economy, Data-driven Blockchain applications, and the Remittance crisis.The Sharing Economy is a term used to transfer assets peer-to-peer through an online marketplace. Instead of going through centralised companies like Lyft or Uber, one can place an order for a ride on a distributed application on a Blockchain network and someone will pick it up without any intermediaries necessary.

The contract will be controlled through smart contracts, so the need for trust has been taken care of. The app automatically contacts the two parties involved and handles all the payments. This completely takes out the centralised party such as Uber that is raking in all the capital from the hard-working people.A Commodity Named Data

Data-driven Blockchain applications are a big thing now too. Data is being sold, stored, and stolen all over the world. Data about people, their jobs, where they’ve been, what they’ve done; pretty much everything. Their data is stored by centralised companies like Google, Apple, Microsoft, and Intel.

On top of that, there are centralised governments using cryptography to spy and collect data on everyone in the world, whether good or bad. In fact, one would know less about themselves than what is stored in those databases right now. People have a limited memory while the database has the capacity to remember for a lifetime.

So, data has value these days and one can even monetise it. The problem here is that their data, which is stored on central databases, inherently belongs to these people but is not owned by them. There are new Blockchain companies coming out now that are attempting to create a digital version of everyone in a bubble. Just for each person.

This bubble collects their data but only gives out the bare necessities when it is required to do something, such as showing their ID when buying liquor. By doing this, one is doing two things: they’re able to monetize their own data and they’re also able to keep their privacy. This benefits both the developed and the developing societies in the sense that data is a universal asset.Blockchain in the Developing World

Finally, an issue that the world has been facing for over a decade: The Global Remittance Problem. This is the crisis of the absurd fee on transferring money from one person to another through a third party. For example, a family member leaves their home for a more economically prosperous lifestyle in a different country to put their kids through a good school but still sends money home every month to sustain the rest of the family.

This person would have to go through third parties such as Moneygram and other means to send money to their family. And these third parties take a big chunk (up to 40%) out of this person’s hard-earned earnings that they were going to send. With Blockchain, one can completely bypass third parties and go straight to the receiving person.

So, Person A in the UK can send Person B in Zimbabwe money through a cryptocurrency platform for a total fee of 2% for the transaction. The transaction happens in seconds and the money is at one’s door within minutes. All completely secure. But, this isn’t just about Blockchain being a breakthrough in security and technology as one can see – whole countries are dependent on it for sustenance.

For example, The Zimbabwean Dollar (ZWL) was rendered obsolete in 2009 due to hyperinflation, and they have no national currency. They were paying a premium of 15% in late 2017 to trade their wealth in for Bitcoin. Blockchain technology is completely changing the game. People turn to cryptocurrency for support in keeping their wealth intact.

This is a necessity for those people, not a comfort.One needs to take this fact into serious consideration when thinking about banning cryptocurrencies or Bitcoin as a whole because there are millions of people out there that already depend on it.

But, even if Bitcoin disappears, which is unlikely, Blockchain technology will be going nowhere and will be around for decades to come. As they say, the technology genie is out of the bottle once again.-

Francisco Gimeno - BC Analyst More comments on Blockchain based use cases in health, developing world, remittance, crypto economy.... this year is the year to reflect on the best use cases and the year where the actual development on real world of these cases will commence.

-

-

What would the landscape look like today if Marriott had discovered AirBnB? It’s always striking to see disruptions being made in industries where the most well-established brand “should have” been at the forefront of innovation, but wasn’t. AT&T could have created Skype and Discover could have created Paypal, but they didn’t. And where major brands are failing, blockchain is quickly stepping into the landscapes of industries ripe for disruption.

What would the landscape look like today if Marriott had discovered AirBnB? It’s always striking to see disruptions being made in industries where the most well-established brand “should have” been at the forefront of innovation, but wasn’t. AT&T could have created Skype and Discover could have created Paypal, but they didn’t. And where major brands are failing, blockchain is quickly stepping into the landscapes of industries ripe for disruption.

Banking, advertising, exchanges, law, insurance, healthcare, energy, supply chain management, and government are all experiencing the introduction of innovative new technologies based on blockchain technology.Blockchain has been a particularly disruptive force in the financial world, and especially in handling online transactions.

The history of finance has generally been inefficient, centralized, and exclusionary, which makes it both very resistant to change and very vulnerable to bad actor parties. Blockchain might present a solution for this logjam.

Some companies are at the forefront of exploring how blockchain could revolutionize the financial world. Ontology is a blockchain for building and managing decentralized identity applications, creating a system that bridges the gap between real world and distributed digital data systems.

Their network is compatible with existing blockchains, but also with traditional information systems–providing decentralized entity management, secure data storage, key management, and encrypted data analysis on any technological system.How can blockchain be leveraged to change the world of business transactions? By disrupting two major elements of this ecosystem: trust systems and identity verification. Let’s take a look at each component.Building better trust systems

Blockchain is a disruptive technology because of its ability to digitize, decentralize, secure and incentivize the validation of transactions. A wide swath of industries are evaluating blockchain to determine what strategic differentiators could exist for their businesses if they leverage blockchain and the secure amount of trust it brings with every financial transaction.

When looking to the future to examine how blockchain could change digital transactions, it’s important to remember what made online sales feasible in the first place. Retailers and transaction processors created a series of safeguards to ensure that buyers and sellers were both protected.

You don’t worry too much about getting your credit card number stolen when you buy something online today, or about failing to receive the item you paid for. The reason buyers are more confident in their online purchases today versus ten years ago is because of trust.But trust systems currently in place often don’t talk to each other, and the gaps between them create unsecured areas for scammers, hackers, or simple human error to exploit.

Blockchain pioneers are working to create a transaction network without weak spaces between or inside trust networks. Because blockchain is immutable, universally accessible, and decentralized, it provides an ideal space for trust-based transactions. Buying, selling, and communicating will no longer be dependent on a series of loosely connected trust networks where the weakest link in the chain can sink the whole system.Secure identity verification

Jerry Cuomo, IBM Fellow and VP of blockchain technologies, sees blockchain already coming more and more into play as people demand control of their identities. We are constantly being asked to share personal information in return for accessing places, information, or opportunities to buy or sell goods and services. Each of these actions puts us at risk for identity theft. He argues the solution to this problem could lie on the blockchain.

Steve Wilson, analyst at Constellation Research, has a more reserved take on the idea that blockchain truly provides secure identity verification: “We need to remember that the classic blockchain is an elaborate system that allows total strangers to nevertheless exchange real value reliably. It works without identity and without trust. So it’s simply illogical to think such a mechanism could have anything to offer identity.

”But in light of blockchain’s constant evolution and rising profile, is it crazy to believe this technology could become a foundational element of our financial system? A large portion of the average bank’s legal requirements under state and federal law revolve around “know your customer” (or, KYC).

KYC obligations mandate that banks conduct research into how money is moved throughout their system, and require that banks verify the identity of all individuals involved in opening new accounts.

But the current KYC process is full of redundancies, as each trust system must talk to the other over and over whenever a new account or withdrawal is made. Instead of each bank having to conduct their own KYC checks, a third-party could simply conduct these verify on behalf of all banks. This is possible thanks to blockchain. Banks could simply verify customers against a global system.With blockchain platforms, your identity is authenticated by multiple sources to give a more secure and trustworthy certification.

Ontology is particularly ahead of the curve because it also offers a comprehensive personal and data tracking profile where all authentications are performed using signatures that cannot be forged or repudiated.Of course, the blockchain world is already a full and dynamic one. New platforms introduced need to provide smooth compatibility with existing prominent protocols like NEO, Ethereum, and other cryptocurrencies.

Not only is Ontology compatible with these existing blockchains, but also with traditional information systems as well.Blockchain has already disrupted multiple industries, and it’s only going to keep going. Cryptocurrency enthusiast will always be on the lookout for versatile platforms utilizing multi-source identity systems, distributed data exchanges, and collaborative systems.

Ontology offers a way for both cryptocurrency enthusiasts and mainstream consumers alike to access the security and innovation offeredThis post is part of our contributor series.

The views expressed are the author's own and not necessarily shared by TNW.

Discover even more from TNW here a leader in technology publishing, reports and events.

Read next: Atari has decentralized gaming for 45 years. Now it's creating altcoins.-

Francisco Gimeno - BC Analyst Very interesting approach on how Blockchain helps business operations, and in fact, the development of society and digital economy. Trust, collaboration, disruption of old schemes, is important to understand that in the incoming future Blockchain will be the technology which opened the race for the new social and economic paradigm

-

-

Marc Hochstein

Marc Hochstein is the managing editor of CoinDesk. The following article originally appeared in CoinDesk Weekly, a custom-curated newsletter delivered every Sunday exclusively to our subscribers.

A nocoiner, according to Urban Dictionary, is someone who has no bitcoin. But not everyone who has no bitcoin is necessarily a nocoiner.Rather, what makes a nocoiner a nocoiner is not simply the absence of cryptocurrency from his investment portfolio, but his sanctimonious attitude about it.

Urban Dictionary's definition, which was posted in December - about the time the word entered wide usage in the bitcoin community - goes on to describe nocoiners as:"....people who missed their opportunity to buy Bitcoin at a low price ... and who [are] now bitter at having missed out. The nocoiner takes out his or her bitterness on Bitcoin Hodlers, by constantly claiming that Bitcoin will crash, is a scam, is a bubble, or other types of easily refuted FUD."

In other words, a nocoiner is full of what philosophers call ressentiment, defined by La Wik as "a reassignment of the pain that accompanies a sense of one's own inferiority/failure onto an external scapegoat." The Twitter user known as @crackbagged picked up on this psychological insight in a Medium post in June of last year, warning fellow bitcoiners not to gloat when the price reaches $1 million:"The people you told about Bitcoin may turn on you and assault you. You might be accused of witchcraft and thrown down a well, or worse. The mind of a nocoiner (a person who has no Bitcoin) is a dangerous place."

Marco Santori, a lawyer who's represented bitcoin startups since the early days and now the president and chief legal officer of wallet provider Blockchain, recently tweeted his distaste for the word "nocoiner," writing that "it has a bitter us-vs-them flavor to it" and "smacks of partisan tribalism.

"But nocoiners engage in tribal signalling at least as much as bitcoiners. The nocoiner isn't just skeptical or even bearish about bitcoin. He feigns epistemic certainty that it will fail. A nocoiner doesn't simply express doubt about the use cases for cryptocurrency - he declares, unequivocally, that there are no use cases at all, in the face of evidence to the contrary.

(A subset of nocoiners will assert that the only uses are criminal, implicitly committing the logical fallacy of appeal to the law.) The nocoiner mocks the bitcoiner's evangelical fervor, but he is every bit as religious in his convictions - and nowhere near as endearing.

The first use of "nocoiner" on Twitter is believed to have been in February 2017, though the term's apparently been used in 4chan forums for several years. But nocoiners have arguably been around since long before Satoshi's white paper. As long as humans have walked the Earth, perhaps.In the late 19th century, Nietzsche compared the nocoiners of the day to tarantulas: "In all their lamentations soundeth vengeance ... and being judge seemeth to them bliss."Mea culpa

Cards on the table: I myself was a proto-nocoiner in the late 1990s, a good 10 years before bitcoin's Genesis block. Working at a daily banking newspaper (a phrase that will be indecipherable to our grandchildren), I sneered at the dot-com boom and regularly gawked at F**ked Company, a website that printed unvetted rumors of layoffs and bankruptcies at the era's highflying startups (what an edgy name, I thought then).

Incredulous about market valuations for companies with no profits or even revenues, I rolled my eyes and looked forward to the day when the the internet bubble would burst. Once this nonsense is over, I thought, we can concentrate on writing about serious companies. Like Countrywide, ha ha.In my defense, a lot of those tech companies I scoffed at were indeed frivolous, and most went belly-up or got acquired.

But the internet still transformed the economy (though the financial services industry less so) and the subsequent mortgage boom and bust were far more destructive, all things considered. Even Fast Company is still around, while the tawdry gossip site that spoofed the magazine's name is long forgotten. Its rapier-like subtlety lives on at the r/buttcoin subreddit.To be clear: The lesson from that era was not that we should revere entrepreneurs or accept all technologists' claims unchallenged.

Rather, keep an open mind, think beyond the quarterly metricsWall Street obsesses over, question your assumptions about how the world will always work - and don't confuse a beautiful horse (the world wide web, bitcoin) with the flies buzzing around its rear end (Pets.com, Mt. Gox).

In other words, you don't have to hold or even like bitcoin. Just don't be a nocoiner.

The leader in blockchain news, CoinDesk strives to offer an open platform for dialogue and discussion on all things blockchain by encouraging contributed articles. As such, the opinions expressed in this article are the author's own and do not necessarily reflect the view of CoinDesk.

For more details on how you can submit an opinion or analysis article, view our Editorial Collaboration Guide or email [email protected].-

Francisco Gimeno - BC Analyst Good reflection on non coiners.... we all know them... the ones who.... well I don't want to say it, better if you, my fellow reader, read it in the article and chuckle....

-