Important

-

Bitcoin and cryptocurrencies have attracted strong criticism from the world's central bankers this year–sparked, perhaps, by Facebook's plans for its own bitcoin rival.

Bitcoin and cryptocurrencies have attracted strong criticism from the world's central bankers this year–sparked, perhaps, by Facebook's plans for its own bitcoin rival.

The bitcoin price soared in the first six-months of this year only to stall amid concerns lawmakers and regulators could be poised to crackdown on the nascent bitcoin and crypto industry.

Now, former European Central Bank (ECB) president Jean-Claude Trichet has slammed bitcoin and Facebook's libra project, warning bitcoin is "not real" and not the future of money.

Jean-Claude Trichet, president of the European Central Bank from 2003 to 2011, was speaking at a ... [+]GETTY IMAGES"I am strongly against bitcoin, and I think we are a little complacent," said Trichet, speaking during a panel discussion at Beijing-based media group Caixin’s annual conference last weekend.

His comments were first reported by the South China Morning Post newspaper."[Bitcoin] itself is not real, with the characteristics that a currency must have."

Trichet also slammed bitcoin and cryptocurrency speculation, which he branded "not healthy.""Even if [the cryptocurrency] is supposed to be based on underlying assets, I am observing a lot of speculation. It is not healthy," Trichet said, adding buying a cryptocurrency is "in many respects pure speculation."

Bitcoin and cryptocurrency adoption has failed to live up to sky-high expectations since bitcoin exploded into the public consciousness in 2017.

Bitcoin soared in 2017 from under $1,000 per bitcoin to almost $20,000, sparking a digital gold rush and making many early adopters overnight millionaires.

Trichet's remarks come amid excitement in the bitcoin and cryptocurrency industry that China could be about to relax its strict crypto restrictions following a ban on bitcoin exchanges in 2017.

Last month, some bitcoin and cryptocurrency market analysts pointed to comments made by China's president President Xi Jinping that the country should "seize the opportunity" of bitcoin's blockchain technology as the reason behind bitcoin's sudden rally.

The bitcoin price rallied hard earlier this year after a disastrous 2018 but that rally has stalled. ... [+]COINDESK"We are already in a domain which has much less physical currency,” he said.

"Whether we are in a domain where that will be replaced with crypto? I have doubts there.

"Trichet's comments echo remarks made by new ECB president Christine Lagarde earlier this year when she warned cryptocurrencies are "shaking the system"—something that could signal a change in the ECB's approach to bitcoin and crypto and potentially spur adoption.

Elsewhere, the last ECB president, Mario Draghi, has said that bitcoin and crypto "are not designed in ways that make them suitable substitutes for money.

"Forbes CryptoAsset & Blockchain Advisor cuts through the hype and identifies real investor opportunities in the emerging world of blockchain and cryptocurrencies. Click to learn more.

Follow me on Twitter.

Billy Bambrough

I am a journalist with significant experience covering technology, finance, economics, and business around the world. As the founding editor of Verdict.co.uk I reported ... Read More-

- 1

Francisco Gimeno - BC Analyst Even strong believers in crypto should stop and read what strongly critics say. There is always a seed of truth everywhere. Cryptos, as they are now, in its infant stage, are rife with volatility and are not able to be yet the alternative to the monetary system, There is a process to this, and only when the blockchain is massively adopted, and the 4th IR techs start to be global when crypto will be also first an alternative to fiat and, when possible, the tool for global tokenisation of society.

-

-

The EOS blockchain is congested by the EIDOS token airdrop, cryptocurrency exchange Coinbase reports on Nov. 9.

The EOS blockchain is congested by the EIDOS token airdrop, cryptocurrency exchange Coinbase reports on Nov. 9.

In a post on its blog, Coinbase claims that it had trouble in processing its clients’ transactions due to EOS network congestion caused by the EIDOS token airdrop.

The exchange has since solved the issue by increasing the amount of staked CPU, securing a sufficient portion of the CPU time remaining on the network to process its transactions.Interestingly, the incident also caused the price of CPU time on the network to increase by over 100,000% over the course of 4 hours. The CPU time price reached nearly 7.69 EOS/millisecond.The cause of the EOS congestion

According to Coinbase, a token called EIDOS was released on EOS on Oct. 31 and its airdrop involves sending transactions on the network from the token’s smart contract.

Exchanges have listed EIDOS/USDT pairs on Nov. 1 to allow people that received the tokens to sell them for the stablecoin.In order to sell the tokens, users have leased the network’s CPU time to increase the number of transfers processed by the blockchain.

This, in turn, caused the EOS network to enter congestion mode and limit the number of transactions users can broadcast to their pro-rata share of total staked CPU resources on the blockchain.The activity related to the token is responsible for a remarkable portion of total activity on the network:“Currently, we’re observing around 95% of all EOS transfer actions are related to the EIDOS contract.”

EOS network behaving as expected

Average users, who hold a relatively low amount of staked CPU resources, are currently unable to send transactions. That being said, the exchange also notes that this situation is only temporary. Coinbase expects the network to return to its normal state as soon as it is no longer profitable to collect the tokens or the CPU leases expire after 30 days and the lenders do not renew the lease. Coinbase also points out:“It is important to note that the EOS protocol is behaving as expected, but congestion mode prevents users from having transactions processed that exceed their CPU stake.”

As Cointelegraph reported at the end of October, EOS holds the top spot in China’s state-backed crypto rankings, while Bitcoin (BTC) is ranked 11th.-

Francisco Gimeno - BC Analyst EOS network, as other successful blockchain networks, are very new, and issues such as network congestion and other tech issues will be happening as more and more token and crypto enterprises start to be widely used. Growing problems which, we hope, show optimism in the blockchain and crypto sphere.

-

-

China’s recent blockchain development bonanza shows no sign of abatement. Business leaders and investors seized on President Xi Jinping’s first-ever endorsement of blockchain as an underpinning technology, and new initiatives sprung up almost overnight.

China’s recent blockchain development bonanza shows no sign of abatement. Business leaders and investors seized on President Xi Jinping’s first-ever endorsement of blockchain as an underpinning technology, and new initiatives sprung up almost overnight.

But Chinese firms, investors and universities have been working quietly on blockchain projects since 2014. From pledging loyalty to the Communist Party and identifying smart city citizens to verifying pigs and tracking liquor shipments, here’s how China’s gone all-in on blockchain.1. An identification system for cities

China’s wasting no time with this one. Since Sunday, city authorities across China have been eligible to apply for a city identification code to link them into a blockchain network developed by three institutes in Shijiazhuang city. The network aims to enable data sharing and interconnectivity between provinces. But Chinese smart city goals don’t end there. China’s aim is to have 100 operational smart cities by 2020, including its future capital Xiongan, and blockchain will feature prominently.2. An authentication method for everything from liquor to pig meat

Prized by international dignitaries (one bottle is a staggering $450,) Moutai liquor is blended from up to 200 spirits and is manufactured by only one company, Kweichow Moutai Co., a partially state-owned Chinese enterprise. The company has been working with Ant Financial (an affiliate of China's internet behemoth Alibaba) since March 2018, to develop a blockchain-based anti-counterfeiting system for its premium hooch.

The country that’s famous for its copies of everything from Louis Vuitton bags to WAL-MART (China’s version is WU-MART), has embraced blockchain’s authentication talents like no other. It’s using them for everything from verifying pigs to “information asymmetry" in trade finance.3. A national digital currency

Many of China’s applications are a far cry from the vision of the technology’s creator Satoshi Nakamoto. One example is China’s plan for a national digital currency. It won’t be decentralized—one of the main factors ensuring that a blockchain is tamper-proof. That’s why some are calling the technology’s renaissance in China, “blockchain with Chinese characteristics.”Decentralized or not, China’s national digital currency is still likely to get off the starting blocks before Facebook’s Libra—the project that’s rumored to have precipitated its speedy rollout.4. A highway to innovation for Big Tech and banks

China’s Big Tech players, such as Jack Ma’s Ant Financial, have long been experimenting with blockchain for financial applications, such as cross-border micro-transaction payments, as well as medical reimbursement and leasing contracts. Things are going well. The People’s Bank of China, Shenzhen branch, reported, in October, that its blockchain-based trade finance platform has processed $10.7 billion in transactions in the past year.5. A hallowed technology worthy of government investment

Local government officials have begun to provide funding for "outstanding blockchain projects.”—a step up from more stealthy governmental funding of the technology through its “key pillar” projects, such tech giant, Tencent. The city of Guangzhou, a blockchain innovation hub since at least 2017, last week introduced a $150 million initiative to support two public or private-based blockchain projects per year.

There’s no reason to think that other regions won’t follow suit. And standardized regulations for the industry are also in the works.For good measure—irony of ironies, considering its prohibitive stance on cryptocurrencies—China has begun cracking down on any articles daring to tarnish blockchain.6. A breeding ground for tech unicorns

The prospect of billions of dollars in cheap government financing and subsidies, has led to Chinese investors snapping up shares in blockchain-related businesses. More than 85 stocks surged by 10 percent—the daily limit on trading in Shanghai and Shenzhen— the Financial Times reported last week.

But China is also home to three of the world’s top Bitcoin mining companies. Last week Chinese Bitcoin miner Bitmain bested all other crypto startups on this year’s “Global Unicorn List,” published by the Shanghai-based Hurun Report. And, on Wednesday, China finally put an end to speculation that bitcoin mining would be phased out, ensuring a more certain future for Canaan and Ebang, and Bitmain too, if it can sort its civil war.7. A tool for party loyalty

The study of blockchain has become a national movement in China—from civil servants, to stay-at-home moms, the public has been encouraged to study Introduction to Blockchain, on “Xuexi Qiangguo,” an app designed to teach President Xi’s thoughts. A national “Blockchain Day” is even under consideration.

And to provide indisputable evidence of loyalty to the Communist Party, a news publication operated by the People’s Daily newspaper has asked Party members to stamp their declarations of fealty directly onto a blockchain.-

Francisco Gimeno - BC Analyst Interesting analysis on how China approaches the blockchain tech and industry. It should be a very good approach, with the exception that, as with almost everything in the country, is enmeshed with the particular politics and social control systems they have there. Everyone in the industry should be very aware of what is going there, as China (or Chinese Whales) dominate a lot of the crypto market, and also the State's support for the development and use of the technology will make its spread easier in that part of the world.

-

-

Cryptocurrency analysts have warned that early adopting Bitcoin $BTC▲0.14% whales still have “plenty of clout” when it comes to dictating market prices.

Cryptocurrency analysts have warned that early adopting Bitcoin $BTC▲0.14% whales still have “plenty of clout” when it comes to dictating market prices.

Those behind Twitter-based transaction monitor @whale_alert have noted that an apparently dormant Bitcoin address houses almost 80,000 BTC ($750 million), and if the owner decides to sell them all, it could spell utter devastation for the industry.

“That address alone — if that is actually a whale who’s been holding their coins for so long without doing anything with them — if they decide, ‘Okay, let’s go sell them,’ it would crush the market completely,” Whale Alert told crypto prime dealer SFOX in a recent interview.

“But it’s really hard to say anything about the status of that address: Are those keys lost? Is that person even still alive? […] It’s just waiting to see if anything happens with those addresses,” they added.A list of top dormant Bitcoin whale addresses (in which no outflowing Bitcoin has been detected in at least five years) can be found here.The ‘Bitcoin whale effect’ has been demonstrated before

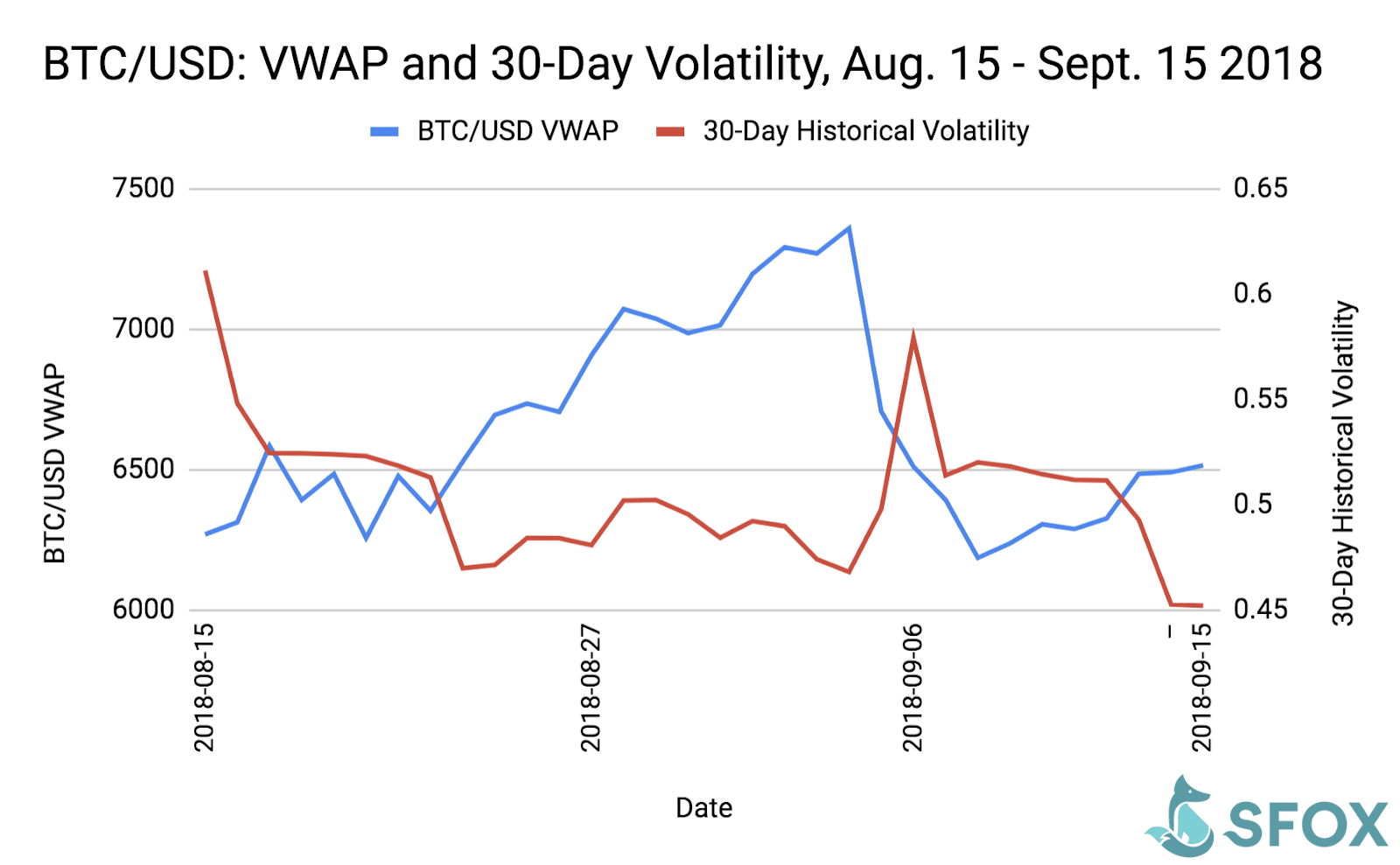

It’s plausible that the power of Bitcoin whales has been demonstrated recently. Whale Alert told SFOX that between August 29 and September 6 2018, a cryptocurrency whale unloaded around $1 billion worth of Bitcoin after they moved the funds from a single wallet to exchanges.When most of the Bitcoin from the wallet was sold, the price of Bitcoin dramatically dropped by almost 15 percent, and the 30-day rolling volatility increased by almost 25 percent.

Price goes down, volatility goes upAnother example is the recent closure of a darknet child abuse imagery ring in South Korea. Police confiscated a massive amount of Bitcoin from the perpetrators, which were eventually auctioned.

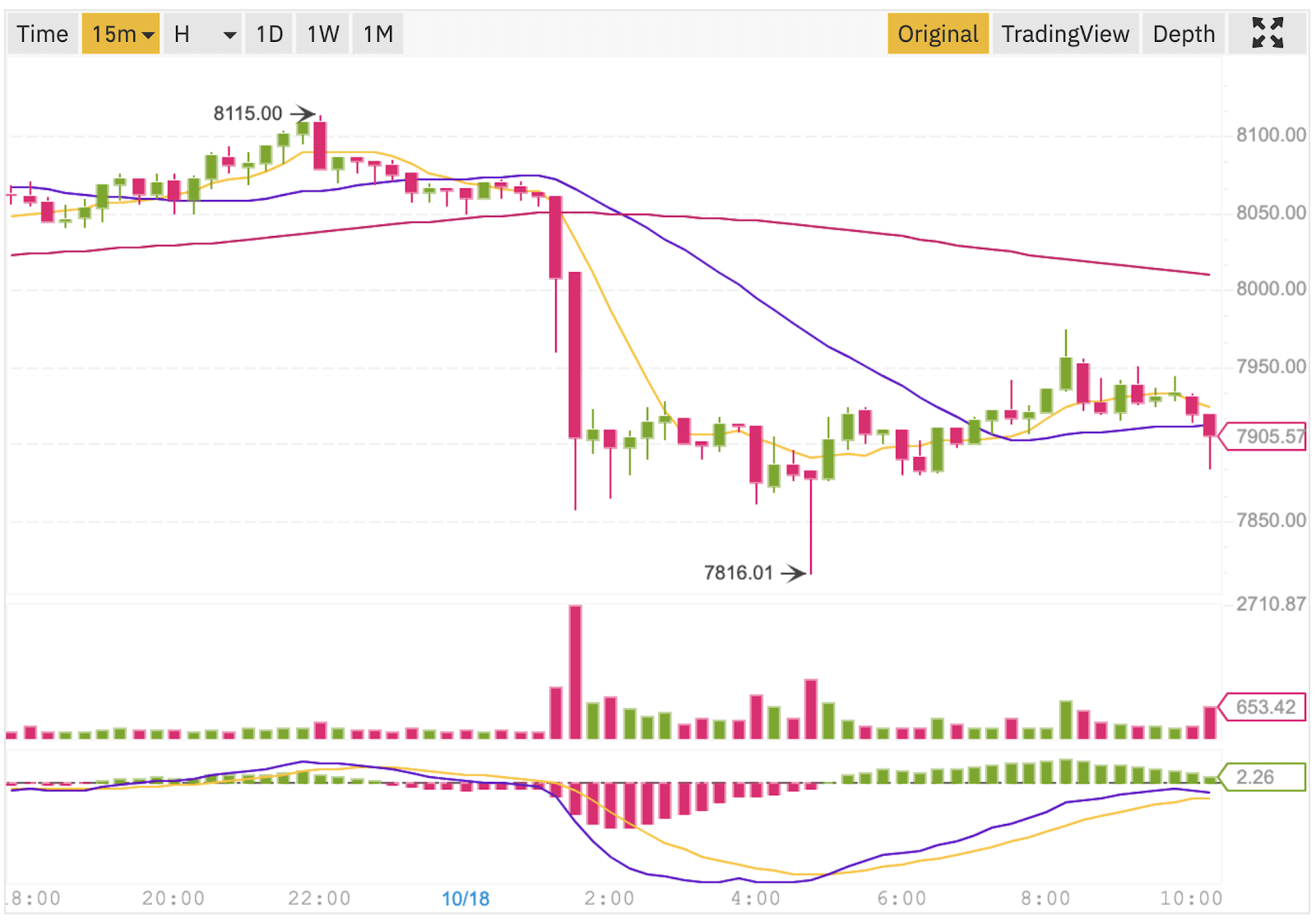

Whale Alert managed to track 10,000 BTC ($94 million) during the auction, which were likely sent to cryptocurrency exchange Binance for selling.“Almost directly after that big transaction, the price of BTC dropped,” said Whale Alert. This seems to be corroborated by Binance‘s order book, which shows a rise in volume just a few hours after the auction.An eventual BTC selloff drove the price of Bitcoin on Binance from $8062.56 to $7856.89.

Those are some big-daddy red candles.It’s worth noting, however, that these kinds of movements are often localized to one particular exchange – in this case, Binance.However, when such large, inactive Bitcoin addresses exist, one can’t help but wonder what the markets would look like if dormant whales one day awoke with a sudden urge to capitulate.

You can read the rest of the Whale Alert interview here.-

Francisco Gimeno - BC Analyst We all hope BTC's so called Whales do not intervene to play with its price. It could happen, however, and this would affect also to every ALtCoin. We can't do anything anyway as BTC is totally unregulated. Just always take care on the always volatile market.

-

-

NEW YORK, Nov 6 (Reuters) - Nervos Network, an open source public blockchain project, said on Wednesday it had raised $72 million in a public sale of its tokens last month, one of the more significant fund raises this year in the cryptocurrency space.

NEW YORK, Nov 6 (Reuters) - Nervos Network, an open source public blockchain project, said on Wednesday it had raised $72 million in a public sale of its tokens last month, one of the more significant fund raises this year in the cryptocurrency space.

The project aims to solve the biggest challenges currently facing blockchains like bitcoin and ethereum. Blockchain, which first emerged as the system powering bitcoin, is a shared database maintained by a network of computers.

After the collapse of cryptocurrency prices in 2018, the focus shifted to blockchain companies developing projects for financial services and the corporate world overall.

Nervos Network sold its tokens to the public through Coinlist, a licensed and compliant token offering platform.

Several institutions participated in the sale, Nervos said, including China Merchants Bank International (CMBI), Polychain Capital, Blockchain Capital, Hashkey Capital, MultiCoin Capital, and Distributed Global.

The public token sale ran from Oct 16-Oct 24.China Merchants Bank’s participation in the token sale comes amid Chinese President Xi Jinping’s message a few weeks ago to embrace blockchain technology, saying the country needed to take advantage of the opportunities the technology provides.

Nervos also announced on Wednesday the launch to the public of its open-sourced network, or mainnet called “Lina.” It added that miners and developers are able to participate and utilize the network starting Nov. 16.

“The launch means that the promised blockchain is ready,” Kevin Wang, co-founder of Nervos, told Reuters in a phone interview, in a project that started two years ago.

Nervos said its blockchain allows developers and enterprises to launch products and services on it without trading off security and decentralization for speed and scalability.

Proceeds from the token offering will go towards engineering and research and development needed to maintain, upgrade, and grow the Nervos project.

“First-generation blockchains like bitcoin and ethereum paved the way by showing us what’s possible,” Wang said.

“Nervos was built on their learnings but it’s now up to us and our community to solve the problems of tomorrow as blockchain adoption is brought to the masses.

”The tokens will be made available when Nervos’ public blockchain is launched.

Nervos last year raised $28 million in a private sale of its token to institutional investors. (Reporting by Gertrude Chavez-Dreyfuss; Editing by Bernadette Baum)-

Francisco Gimeno - BC Analyst Tokens sales like this show blockchain and crypto's fundraising is not dead at all. Nervos is promising unlimited scalability through their Layer 2 protocol, and economic incentives for token holders. Selling themselves as the new generation we will see what happens when they open their network mid-November.

-

-

The FT's Brendan Greeley seeks answers at the annual International Monetary Fund meeting in Washington.

The FT's Brendan Greeley seeks answers at the annual International Monetary Fund meeting in Washington.

Take our survey and tell us what you like about our YouTube channel and would like to see more of: https://bit.ly/33SJ8AI-

Francisco Gimeno - BC Analyst Digital currencies are yet at their infancy. Even the most fanatic believers in them understand that a world where digital currencies substitute fiat is a very long time from us now. Yes, crypto will be more and more massively used. Yes, a digital economy will bring tokenisation. But only real deep civilisation change would bring wide changes including the total replacement of traditional fiat. This has happened in History and will happen again.

-