ICO

-

The cryptocurrency market has been in decline since January, but it appears blockchain startups are still profiting big. Indeed, new data suggests Ethereum-based initial coin offerings (ICOs) are sitting on $830 million in reserves – that is despite having already sold almost as much ETH as they initially raised.

The cryptocurrency market has been in decline since January, but it appears blockchain startups are still profiting big. Indeed, new data suggests Ethereum-based initial coin offerings (ICOs) are sitting on $830 million in reserves – that is despite having already sold almost as much ETH as they initially raised.

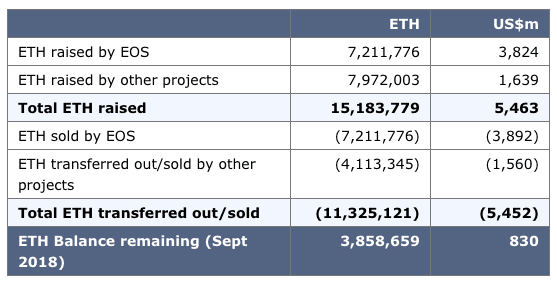

According to data from BitMEX Research, blockchain startups raised a total of $5,463 million worth of Ethereum $ETH▼1.02% (approximately 15 million ETH) in ICOs by September 2018. Interestingly, the sum almost matches the total amount of ETH these companies sold during the same period – $5,452 million (or 11.3 million ETH).

The data essentially shows that most blockchain startups sold their ETH at a value higher than initially raised. This is also what made it possible to secure the funds initially raised (in terms of dollars), but also keep a huge treasure trove of Ether in reserve.

(Source: Ethereum Blockchain, BitMEX Research, TokenAnalyst, Token Data, Price data from Etherscan)Indeed, it would appear that ICOs sold much of their Ethereum before the price dropped 85 percent, from $1,400 last December to $230 in September 2018.

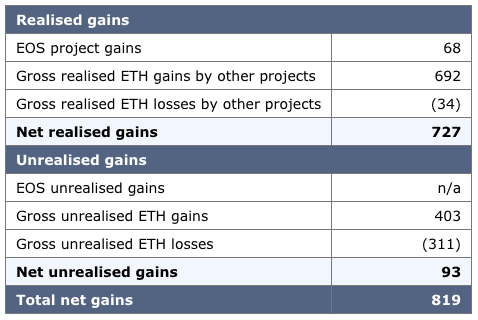

As a result, ICOs have realized profits of $727 million, while still retaining $830 million worth of Ethereum (3.9 million ETH) in reserves. It would seem the ETH being held is pure profit for the ICOs.

(Source: Ethereum Blockchain, BitMEX Research, TokenAnalyst, Token Data, Price data from Etherscan)BitMEX points out the findings are significant in two ways. On the one hand, it shows that most ICOs don’t engage in “panic selling” as a strategy to off-load funds.

On the other, it highlights how easy it is for blockchain startups to run ICOs for quick cash rewards.As the value of Ethereum remains low and panic selling isn’t a strategy ICOs seem to endorse, it is unlikely that we will see any ICOs sell more of their ETH funds for the time being.

However, even if these ICOs did decide to off-load all 3.9 million Ether that they currently hold, it’s unlikely that this amount would be large enough to negatively impact the price of Ethereum – given that there is 102 million ETH currently in circulation.If you’re interested in everything blockchain, chances are you’ll love Hard Fork Decentralized.

Our blockchain and cryptocurrency event is coming up soon – join us to hear from experts about the industry’s future. Ticket sales are now open, check it out!-

- 1

Francisco Gimeno - BC Analyst Companies which have raised ICOs, naturally have to raise some profits to continue working in their products, while reserving most of their tokens based on Ethereum for future. This article is common sense, and also shows how most of the ICOs don't move in crypto speculation but into development of their own projects. Good data here.

-

-

Tim Enneking, Robert Brauer & Andrew Kang

Tim Enneking, Robert Brauer & Andrew Kang

Tim Enneking is managing director at Crypto Asset Management. Robert Brauer and Andrew Kang are members of the Crypto Asset Management ICO Analysis team. The number of initial coin offerings (ICOs) is growing rapidly, having raised an astounding $5.6 billion in 2017 alone.

More outrageous is that, by most estimates, over half of the ICOs launched in 2017 have already failed.In addition to the hundreds of ICOs being launched every month, our management company Crypto Asset Management (CAM), also receives around a dozen emails per day from new companies planning on launching crypto tokens to raise capital.

CAM, through the various funds and share classes it manages, invests in less than one out of every 100 ICOs that comes across its desk.Out of absolute necessity, we have developed an analytical framework for ICOs, which CAM applies to every such opportunity it evaluates.

In this article we explain what we call The Seven Pillars Of ICO Investing™, which we've rigorously crafted over several years of investing in crypto and other assets.Pillar #1: Team

The critical element which we are searching for is an experienced team, ideally with a strong track record in developing and launching blockchain technology. In addition, the team should have experience in the market it is targeting. A team that is not only competent, but capable of developing, completing and/or expanding the project is paramount to its success.A couple of additional issues to consider are:- Does the team have a vesting token schedule that will properly incentivize it?

- Do the advisors have the right experience and are they actively engaged?

- Does the project have any notable financial backers? (VCs, other hedge funds, etc.)

Pillar #2: Idea

Without a compelling, realistic and timely idea for a blockchain-based enterprise, the investment will almost certainly fail.A few of the key things we look for are:- Total addressable market: How large is the opportunity? We want as large of a market as possible (See: ethereum, filecoin).

- Product-market fit: Does the business address an urgent problem? (0x, ChainLink)

- Unique value proposition: What facets of the technology enable it to stand out from the competition? How much competition is there (Wax)? Ideally, the token has proprietary technology, and as little competition as possible (Orchid Protocol).

There is clearly an interrelationship between Pillars 1 and 2. However, if we had to choose between them, we would clearly rather invest in an "A" team working on a "B" idea than a "B" team working on an "A" idea.A talented group of people are the lifeblood of any business, and crypto is no different.Pillar #3: Execution

In the cut-throat business world we live in, the only thing that matters is results. A brilliant idea and great team are nice, but execution is everything. Is there a working prototype or does your idea only exist in a nebulously written white paper?

We prefer to invest in a product that already exists to some degree (Presearch, Basic Attention Token, Superbloom, FunFair), whether in the crypto space or analogously in the fiat space (Wax). Finally, we look for some sort of proof that the company will be able to hit future milestones.Pillar #4: Legal/Regulatory

This pillar is essential given the current and growing regulatory uncertainty in the industry. Almost every week, there is news of a governmental agency in one country or another taking regulatory action or making a new statement around ICO governance. Of course, almost as often, there is news of a different country considering crypto-favorable legislation.

Comprehensive regulation in many marketplaces is on the horizon and it is imperative to ensure that ICOs vigilantly navigate the landscape to the best of their abilities. The threshold issue is jurisdiction: in what country is or will the ICO company be incorporated and the ICO executed?

This determines the rules that will apply to the company's actions and the ICO. Depending on the approach taken, we may apply the somewhat arcane rules of the Howey test (in the US or if US investors are targeted or allowed to invest), KYC/AML principles (which are essentially universal) and applicable securities law.Pillar #5: Tokenization

A significant number of the ICOs we analyze do not actually need the blockchain, tokenization or a public sale of their tokens to be successful. When this is an issue, it is usually the last - public sale - which is not necessary. (NASDAQ's settlement system is an excellent example of where tokenization is a brilliant idea but a public market would be superfluous, or even counterproductive.)

Also, they are sometimes glorified apps that could be built without creating a specific token, despite how much "utility" the founders may claim their token provides. With the enormous amount of value exchanging hands over the blockchain and the prospect of getting "free" money without giving up any equity, it's not hard to imagine why many industrious entrepreneurs try to identify any possible reason to launch an ICO.

That being said, one of the crucial things that every investment we make must have is a legitimate reason for "tokenizing" their business, and for creating a public market for that token (OmiseGo, Icon, Raiden Network, Cosmos).Pillar #6: ICO Structure

Similar to traditional venture capital investing, the financial underpinnings of the deal ultimately determine the decision to invest. The characteristics of an ICO can have important implications on the expected upside of the token.This can be split out into two categories - ICO mechanics and ICO deal structure.- ICO Mechanics - Historically, ICOs with a lower hard cap tend to outperform ICOs with massive hard caps. While it is important that the parent companies be well funded and have sufficient runway to work with, ICOs need to have a convincing plan for use of proceeds as the potential upside decreases in proportion to the amount raised. The precise metric here is valuation of the token economy - a derivation of the hard cap. Both the valuation in light of circulating tokens at launch and the valuation upon release of all tokens are factors that we consider.

- ICO Deal Structure - The deal should be structured in a way so that investors are not at a disadvantageous position to the market.These are a few of our considerations:

- Distribution: The team should have a compelling structure for the distribution of tokens, fair allocation among team/advisors and investors, programs for market uptake, etc.

- Distribution Schedule: Given the fast-moving pace of the crypto market, the distribution schedule should not massively favor specific parties. While long distribution periods can be considered acceptable for high-potential ICOs, individual liquidity preferences should be considered.

- Discounts: Discounts are ubiquitous in the ICO environment, so examining the discount levels given to different tranches allows investors to understand where they stand in relation to other stakeholders.

- Equity Stakes: At Crypto Asset Management, we like to be part of the growth of the company and investing directly into the equity of a company allows us to play a greater role in that development. In the world of token sales and short-term liquidity, people often forget that the value proposition of a company can be just as great or even greater than the token ecosystem it is developing.

Pillar #7: Price Drivers

Even if we believe a team is able to create a great product that incorporates a token with an imperative use case, this does not necessarily mean that we will want to hold the token or invest in the ICO. A token must additionally have a mechanism to drive price appreciation.

A token with constant supply without any incentive to hold, will not be subject to buying pressure which significantly outweighs selling pressure over the long run (Votes).

This is underpinned by the concept of price risk, in which individuals will lean towards reducing their exposure to price volatility in favor of fiat or a form of stable currency. (Kyle Samani has written an in-depth piece on this velocity problem here.)A few of the price drivers we look for include:- Network Volume: In almost every instance the value of a token increases as the number of transactions on the blockchain increases (bitcoin, ethereum). This is one of the most basic, yet influential, indicators of demand, and is also the reason we invest primarily in protocols rather than dapps.

- Market Leadership: We look to invest only in tokens that are clear market leaders, or have the potential to be in the near future. Usually, these tokens have a distinct and growing unique advantage over their competition (Practical VR).

- Incentives to Hold: There is a clear reason why a user would rather hold than spend the token, which can be related specifically to speculated price increases or other non-monetary rewards (Presearch, PROPS). We won't invest in a token that's only purpose is a medium of exchange.

- Supply Changes: This can include limiting inflation, meaning the token supply does not dilute the value of all tokens over time, or token burning, where the supply of tokens in the system decreases over time (Binance Coin, Iconomi).

- Profit Sharing: Part of the value that is extracted from the system is given back to the token holders (Augur, NEO, Neon Exchange, Ethorse).

- Staking: Having users of a network to lock up their tokens either for network consensus or as a requirement in certain processes. (Bee Network, Open Platform, NuCypher, Video Coin).

- Sufficient Liquidity: If the project isn't proactive about getting listed on multiple exchanges, preferably top-tier exchanges, we will likely not make an investment.

Please note that, as a general rule, we are not in favor of asset-backed tokens as an investment vehicle at this time. There are no real drivers of price formation after an initial, relatively small boost for convenience (Sandcoin, OneGram) and the opportunity cost is consequently too high (there are far greater returns elsewhere).Importantly, the effect of implementing strong incentives to hold is multiplicative.

Not only will the price increase be driven by the inherent tokenomics design, but also by speculation directly related to the implementation of these drivers. Despite the incredible number of fly-by-night operations in the world of ICOs, it is certain that token generation events are here to stay.

Such events are completely transforming the traditional venture capital industry and, for savvy investors, are creating fortunes literally overnight. For unsophisticated or undisciplined investors, ICOs are a minefield that should probably be avoided.

However, for those who perform proper due diligence, the odds increase for realizing breathtaking returns on your investments.This article is an abbreviated summary of our process for investing in ICOs.

Here at Crypto Asset Management, we've also developed more in-depth tools, such as our innovative 64-point ICO Scorecard and a more traditional Private Equity Due Diligence Checklist.

Stack of coins via Shutterstock

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.

Discover more insights from Coindesk here: https://www.coindesk.com/seven-pillars-ico-investing/-

Admin

Admin - 0 comments

- 2 likes

- Like

- Share

-

Brady Dale

Brady Dale

Apr 11, 2018 at 12:45 UTC | Updated Apr 12, 2018 at 04:08 UTCThe average crypto enthusiast isn't likely to get their hands on grams - Telegram's crypto token - anytime soon.While half of the ambitious $1.2 billion the messaging giant hoped to raise was supposed to come from an ICO open to public investors, recent SEC filings confirm Telegram has already raised $1.7 billion from two private sales.

Now, sources with knowledge of the deal believe the company is likely to scrap its public sale altogether.The reason? Raising money from the public could be way more trouble than it's worth.For one, Telegram's blockchain, called the Telegram Open Network (TON), hasn't been built yet. (To be clear, no one has received any grams.) As such, Telegram is selling what basically amounts to IOUs for future grams under the Simple Agreement for Future Tokens (SAFT) framework.

That means - as displayed by the company's SEC filings - the company is selling a security, which cannot be sold to non-accredited investors (except under some exemptions)."The regulatory environment is in a weird place with most teams having more questions than answers," said Anthony Pompliano, a general partner at Morgan Creek Capital Blockchain.

"If teams can raise their capital goals in private sales, they'll continue to do so until there is less ambiguity in regulations."This appears to be what Telegram is doing, although it's been tough to tell exactly what the founders are thinking since they've said nothing about the ICO or TON, both of which the white paper details will help facilitate a network of faster payments, file-sharing, decentralized privacy, domain registration and more.Telegram did not respond to a request for comment.Pompliano told CoinDesk:"The goal of fundraising is to gain access to capital to allow a team to build a product and company. It appears Telegram has already achieved their goal so there would be no reason to conduct a public sale."

Tech first

This is especially cogent as it relates to the amount of work a legal public sale would entail.For one, Telegram would have to go through a know-your-customer and anti-money laundering verification process to be able to sell to everyday investors.

For private, known investors that have been identified plenty of times for investment purposes, the verification work is less cumbersome, but for a store cashier who is investing for the first time, it's more challenging to prove they are who they say they are.

And it just has to do it so many more times. This would be no small lift and may not be attractive to a company that already has plenty of money.

Plus, there's already a secondary market for grams whereby small investors are buying the crypto tokens from whales that got into the private sales, according to Alexander Borodich, an alum of the Mail.ru Group, one of Russia's largest tech companies, and an angel investor passed on the opportunity to invest in Telegram's ICO.As such, he said it's unclear whether a legit public sale will happen.

The TON technical white paper describes an ongoing token sale that will continue intermittently well into the future. That phase may be a sort of public sale, but one that won't begin until the protocol launches.And according to Sid Kalla of the Turing Advisory Group, building the product before selling to the public would be that smart thing for Telegram to do.He told CoinDesk:"The private sales were raised at around the top of the market euphoria. For a public valuation to reach back to those levels, the crypto community would need to see something concrete."

Public opinion

Which is another reason Telegram may discard it's public sale for some time - so it doesn't have to deal with thousands of people's unsolicited opinions.

When a company decides to do a public sale, it introduces complexity into its public relations.That's why large, publicly traded companies devote whole departments to investor relations, said Stephen Palley of the law firm Anderson Kill.

And that's something young startups may not have bandwidth to manage, he said."In this twilight world of ICO crowdfunding, you have a company that's brand new, it's a startup ... You suddenly have thousands -- tens of thousands -- of people who feel like they are stakeholders," Palley continued, adding:"Do you really want to manage all those people?"

While Telegram is five years old, it's still a relatively small company that's so far bootstrapped development of its messaging platform from the founders' own pockets, which suggests it doesn't have experience in investor relations.

Kalla agreed, telling CoinDesk, "Since Telegram is trying to solve several hard technological problems (like sharding, say) there may be inevitable delays and setbacks. The private investors are likely more used to such things than the public at large."As much as possible

That said, not everyone agrees that Telegram will scrap its public sale so soon."I see no motivation for Telegram to call off their public sale," Joe DiPasquale, CEO of the crypto fund-of-funds BitBull Capital, wrote CoinDesk via a spokesperson. "They seem dead set on raising as much capital as possible ... Considering they're targeting the mass adoption of their user base, I can't imagine them estranging the masses by canceling the public sale.

"Although, it would help if Telegram offered some insight into when and where this sale would be launched, since crypto enthusiasts keep getting bilked out of money by Telegram-focused phishing attacks.DiPasquale's sentiment isn't the prevailing one, though.

Even if Telegram needs more money to build, it doesn't seem like it's having trouble soliciting from experienced investors through private sales.Borodich for one predicts that Telegram will raise more money - to boost the total to $2.5 billion - through another private sale before the end of the year.

Another source concurred.Having said that, because there's been a pullback in the cryptocurrency hype, Kalla said, investors would likely want a lower price point for allocations of grams.And as such, he said:"The only reason I see a public token sale making sense if there is investor demand or pressure or any contractual obligation for liquidity."

Telegram image via Shutterstock

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.-

Francisco Gimeno - BC Analyst Whoever has been following the issue is expecting that Telegram probably won't do a public ICO. First because it has already earned a lot of money through private sales under SAFT agreements, and second because it wants to avoid problems with SEC in USA. This may happen also with future ICOs for other companies which may invite a private sale before going to public. It is a very interesting movement.

-

-

Many cryptocurrency speculators are banking on the theory that someone dumber than them will buy their tokens for more than they paid. That’s a pretty good bet…until it isn’t.

Many cryptocurrency speculators are banking on the theory that someone dumber than them will buy their tokens for more than they paid. That’s a pretty good bet…until it isn’t.

AUTHOR: JOI ITOBY JOI ITO

EVER SINCE MY friends and I set up a Digicash server to sell music and artwork with a digital currency called eCash representing real gold, back in the 90s, I’ve been waiting for the day when cryptocurrencies—digital currencies that operate independently of central banks by using encryption to generate units and verify transfers of funds—would transform the world. Cryptocurrencies are finally here, but not exactly in the way that I envisioned.

And so since last year, I’ve found myself issuing warnings instead of accolades about the latest trend in the frothy world of cryptocurrencies: ICOs, or initial coin offerings. The initial idea was a pretty good one—blockchain technology could be used to issue new cryptographically secure “tokens” or “coins” that are easy to transmit peer-to-peer.

The coins could be sold to fund open-source software projects and other services that people find useful but are hard to finance with traditional structures. They could even function as shares and thus allow startups to finance themselves far more efficiently, from a broader range of people, and without the intermediaries that take fees and require a drawn-out process. Or the “coins” could represent some unit of utility, such as a gigabyte of storage or access to a network.

Joi Ito (@joi) is an Ideas contributor for WIRED. Ito has been recognized for his work as an activist, entrepreneur, venture capitalist, and advocate of emergent democracy, privacy, and internet freedom.

As director of the MIT Media Lab and a professor of the practice of media arts and sciences, he is currently exploring how radical new approaches to science and technology can transform society in substantial and positive ways. Ito’s honors include being named as one of TIME magazine’s Cyber-Elite and selection as one of the Global Leaders for Tomorrow by the World Economic Forum.

He is a coauthor with Jeff Howe of Whiplash: How to Survive Our Faster Future.My concern with today’s ICOs is that they’re being fueled by the gold-rush mentality around cryptocurrencies, and so are deployed in irresponsible ways that are causing harm to individuals and damaging the ecosystem of developers and organizations.

We haven’t set up the legal, technical, or normative controls yet, and many people are taking advantage of this.Thus, ICOs are to cryptocurrencies what Trump is to American democracy: not what the founders of the institution envisioned.

It doesn’t have to be that way.

THINK OF AN ICO as a means of creating digital certificates that have signatures, rules, programs, and other attributes controlled cryptographically. You could create a digital version of a check, a stock certificate, an IOU, or a gift card for a hamburger or a barrel of oil. That makes these certificates equivalent to a security, a commodity, or even just a simple financial transaction.

In their traditional forms, each of these elements have different risks and different regulatory bodies governing them. The Securities and Exchange Commission, the Treasury Department, and so on play a role in reducing financial risks and preventing financial crimes. In other words, some of the rules and regulations—the friction—in the existing system is there to protect investors, customers, and society.

But those regulators haven’t caught up with ICOs quite yet. Issuers are getting rich and unwitting investors are buying tokens of questionable value.On July 25, 2017, the SEC announced that if a token looks like a security, it will regulate and treat the token as a security. It subsequently set up a task force to go after ICOs that are scamming investors and exploiting gray areas in securities laws.

But many of the tokens issued through ICOs today are not shares in a company. Rather, they are “tokenized” versions of some sort of product, service, or asset, or a promise to invest funds in research or infrastructure. Issuers are calling the sale of such tokens a “crowd sale” instead of a “funding” to make it clear that people are buying a product rather than a security—and, intentionally or not, avoiding regulatory scrutiny.

A Swiss platform for posting jobs, for instance, used a crowd sale to sell what it calls Global Jobcoin, which buyers can use to pay for employment services. Meanwhile, someone—it is almost impossible to figure out who—is using a crowd sale to peddle Jesus Coins, which promise to forgive sins and fight corruption in “the church,” among other things.

I’m not saying all ICOs are sketchy. Some have legitimate uses, such as Filecoin, which aims to allow a token holder access to storage online and rewards people for hosting files.

The problem is that many of these tokens are traded on exchanges, and are thus viewed by investors as commodities or currencies to trade in and out of.

Most tokens aren’t “pegged” to anything in the real world, and their exchange rates fluctuate. Most tokens are currently going up in value, which has attracted a large number of speculators who aren’t looking for workers or forgiveness of sin.

They don't really care about the underlying asset linked to tokens, and are investing on the Greater Fools Theory—the idea that someone dumber than them will buy their tokens for more than they paid.

This is a pretty good bet … until it isn’t.Requiring companies to sell tokens only to accredited investors won’t solve the problem, because those investors will later sell them to speculators or, worse, to people who have seen the ads online promising to provide the secret of making a bundle on cryptocurrencies. And Wall Street has never been willing to end a rip-roaring party once the keg is tapped.

The regulatory intervention that has just begun will need to be much more sophisticated and technically informed, and in the meantime there’s a long line of people who’ve read about the skyrocketing price of Bitcoin (or Jesus Coin) and are waiting for a chance to buy into one of the myriad ICOs coming down the pipeline.

And volatility adds to the burdens of young companies issuing tokens, which will need functions similar to a central bank and corporate-style investor relations in addition to just trying to run their core businesses. If these companies fail, investors will get some benefit in a fire sale or liquidation, but token holders will end up with something akin to the Zimbabwean dollar in my scrapbook.

But a coin without volatility would be of little interest to such speculators, and it would be quite easy to design. We could start by simply pegging the value of tokens to something, say $1 or the price of one hamburger. A pegged token would fluctuate in “value” only to the extent that the underlying asset fluctuated. If the subscription price is fixed or you only eat hamburgers, there would be much less fluctuation or volatility.

For people hoping to make a fast buck, that linkage would remove potential upside value, narrowing the market of the coins to mostly just those people who would use the service. Having said that, even with a value pegged to some underlying asset, it’s possible that the current irrational market would still make prices go crazy.

If the issuer didn’t own or have the ability to produce the underlying asset, the owners of its coins might be in peril of holding a valueless proxy.

For example, concerns have escalated recently that Tether, a cryptocurrency pegged to the dollar, may or may not have actual dollars to back its tokens. If it doesn’t, then it’s sort of like an uninsured bank printing its own version of dollar bills without anything in its vaults.

People have been buying Tether as a proxy for dollars on cryptocurrency exchanges, and so its failure might cause the price of Bitcoin to plummet and, more broadly, do substantial damage to the market.

A lot of otherwise productive developers are devoting their expertise and attention to working on shallow, quick money ICOs rather than working to sort out the underlying infrastructure and protocols in academic and more open deliberative settings not fueled by warped financial interest.It reminds me of the late-’90s dot-com bubble, when the now-defunct Pets.com was spending investor money buying Super Bowl ads to sell products at 30 percent of what they cost the company itself to buy.

I understand the desire of venture capital to use blockchain and other technologies underpinning ICOs, and for new companies to take this nearly “free money” to build their businesses. But there is, I feel, an ethical issue in such knowing exploitation. I’ve pleaded my case with entrepreneurs, investors, and developers, but it’s like trying to stand in front of a buffalo stampede.

ICO mania will no doubt run its course, as all such financial manias do. But in the meantime, people will be hurt and there will be a painful correction. The one upside is this: As in the wake of the dot-com implosion, serious developers and investors will continue to work to build what will be a more robust network and foundation for the future of the blockchain and cryptocurrencies.

My friend Bill Schoenfeld, along with a small number of investors, made a lot of money when the real estate bubble in Japan popped. At some point, the Japanese real estate bubble got going so fast that almost no one was assessing the underlying value, but Bill insisted on pricing real estate doing just that. When the bubble popped and the prices went into free-fall, he bought a lot of property at a rational price.

Bubbles make pricing irrational going up as well as going down. Maybe the clever thing to do right now is for people to assess the real underlying value of these tokens and be prepared to buy the ones that are actually valuable when the bubble pops.

Amara’s law famously states that “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.

” The largest and most successful companies on the internet were built after the first bubble, when the protocols and the technologies became mature. I’m holding my nose, squinting my eyes, and imagining—and running for the mountains beyond the dust storm around the ICO stampede.

Note on conflict of interests:

When I helped found the MIT Media Lab Digital Currency Initiative, I sold my shares in all blockchain and bitcoin related companies and have not invested in any companies engaging in cryptocurrencies as their primary activity. I do not hold any material amount of any cryptocurrency.

I believe that in the current phase of our work, it is important for me to be clear of any conflicts of interest. You can see a more complete conflict of interest disclosure on my website.

The Blockchain BoomPivoting to blockchain has become the new lifeline for struggling startups.Everipedia wants to use the blockchain to create a more powerful, accountable encyclopedia.Careful what you use your cryptocurrency for: Researchers have found that it's all too easy to dredge up evidence of years-old bitcoin drug deals.

Help friends or someone you care about discover blockchain and

cryptocurrencies, by simply sharing this page. Don't keep it to

yourself.....share Blockchain Company (BC).

Did You Know About This?

You can curate a Personal Blockchain Page right here on Blockchain Company ( BC ) like these 2 great user examples here:

http://www.blockchaincompany.info/Paula

http://www.blockchaincompany.info/Francisco

Show

your blockchain page off to your employer, colleagues and friends. It

demonstrates your professional awareness and competency of this

revolutionary paradigm changing the world. It's free if you are a

consumer user. Just Create your Account here in less than 3 mins!

Or

Click Create Account above in the upper right corner. Instructions how

to curate your blockchain page from information you discover on BC, is

sent in your email after you sign up.

You might be able to capture your ' first name " unique url for your blockchain page too! Like : http://www.blockchaincompany.info/robert

You

may be entitled to cryptocurrency tokens, offers and discounts at any

time in the future once you are a user on our platform.

-

Samuel Santos Sales & Growth Marketing at BC Awesome...

-

-

By:

By:

Brady Dale

FEATURE

To describe Telegram's planned initial coin offering (ICO) as ambitious would be an understatement.And it's not only because the provider of a popular messaging app is seeking to raise $1.2 billion, according to three people familiar with the offering, which would represent the largest crypto token sale to date.Nor is it just because Telegram, with 200 million users, seems to be intent on bringing cryptocurrency payments to the masses.

Rather, the proposed Telegram Open Network (TON) would seek nothing short of decentralizing online communication, with a suite of services, from file sharing to anonymous browsing, purchasable with the new crypto tokens, known as grams.

"This is like Elon Musk-level ambition," Kyle Samani of Multicoin Capital, who looked at the offering, told CoinDesk. In fact, Samani said he declined to invest in the ICO precisely because of its broad scope.

"My concern as an investor is focus and diluted effort," he said, since the TON aims to disrupt the same areas as several other blockchain startups that have also recently raised funds via token sales.

Outlined in a 23-page primer on the offering obtained by CoinDesk, the TON is a blockchain protocol for the peer-to-peer movement of funds between users and to make purchases. This would interact directly with Telegram's messenger app, which was created in 2013 at VK, the Russian equivalent of Facebook.

Sources told CoinDesk that $500 million to $600 million was Telegram's goal in a presale, with the other $600 million to $700 million to be offered publicly.The company is using the Simple Agreement for Futures Tokens (SAFT) structure, in which money is raised from accredited investors before a functioning network is built, in order to avoid running afoul of securities laws. The grams, eventually delivered to the SAFT investors, could then be resold to consumers.Talk of the town

Telegram, which has not responded to CoinDesk's requests for comment, would, no doubt, be the most mainstream company to issue a crypto token to date, although the social messaging app Kik raised $98 million in an ICO in September.

"Many hedge fund managers are talking about the TON ICO," said BitBull Capital's Joe DiPasquale. "Telegram has owned the chat space for those in crypto, and our usage of the app is increasing due to its security and ease. It's become the platform of choice for crypto discussion, and they will have a lot of attention leading into their ICO."

Calling the presale's minimum investment of $1 million and cap on proceeds high and its one-year lockup long compared to other token sales before it, DiPasquale still continued optimistically, saying:"They are likely to be successful with a raise given their success as a platform to date."

Other investors CoinDesk spoke with were reluctant to discuss the sale, with one citing a non-disclosure agreement required to view the primer and a technical white paper.

Rumors of the ICO plan started last week, and on Sunday a Russian-language slide deck marked "Ton_Draft" was posted on a Russian-language Telegram channel run by Fedor Skuratov, CEO of Combot, an analytics platform for the messaging app.

TechCrunch was the first English language outlet to report the plan.While the document CoinDesk received, and other investors have confirmed receiving, does not seem to be the most detailed account of the TON system (its footnotes refer to the technical white paper), the primer does provide a basic outline of what Telegram hopes to achieve with its crypto token.Lofty goals

In the document, the company declares:"The current state of blockchain technology resembles automobile design in 1870: it is promising and praised by enthusiasts, but inefficient and too complicated to appeal to the mass consumer."

As such, no cryptocurrency has gained truly mainstream success, yet Telegram believes, according to the paper, that a decentralized counterpart to everyday money is needed. The primer states that the company is hoping to enable the easy exchange of micropayments among users and bots, something that's been of general interest throughout the blockchain space.

In an effort to do that, the primer explains that 5 billion grams will be generated, with 4 percent reserved for the Telegram team (with a four-year vesting period) and 44 percent to be sold during the ICO. The remaining 52 percent will be "retained by the TON Reserve to protect the nascent cryptocurrency from speculative trading and to maintain flexibility at the early stages of the evolution of the system," the primer states.

According to a source with knowledge of the presale terms, the one-year lockup comes with a 60 percent discount. The ICO is likely all or a part of the "three big announcements" Telegram co-founder Pavel Durov told his followers about on his public Telegram channel on New Year's Eve.

According to the primer, the sale will take place in the first quarter of 2018, with the SAFTs converting to grams in the fourth quarter.The roadmap goes on to state that the first related product, "External Secure ID," will launch in the first quarter of 2018, with all other products to be rolled out by the first half of 2019. And the Telegram founders' control of the project will shift to a non-profit foundation by 2021.'Tons' of competitors

While the TON's main priority is consumer payments, the primer goes into a number of services Telegram would like to build out that seem to encroach on territories, such as file sharing and privacy, already staked out by well-known and well-funded ICO issuers.For instance, the primer outlines:- TON Storage – "A distributed file-storage technology, accessible through the TON P2P Network and available for storing arbitrary files, with torrent-like access technology and smart contracts used to enforce availability." Throwing in torrent-like access makes this product similar to the Filecoin platform, which raised $257 million in a token sale in September, as well as projects like Storj and Sia.

- TON Proxy – "This layer can be used to create decentralized VPN services and blockchain-based TOR alternatives to achieve anonymity and protect online privacy." This sounds similar to the vision articulated by the team behind Orchid.

- TON Services – "A platform for third-party services of any kind that enables smartphone-like friendly interfaces for decentralized apps and smart contracts, as well as a World Wide Web-like decentralized browsing experience." A number of blockchain-based startups are building decentralized app marketplaces, including Coinbase, which continues to build out its Toshi marketplace; and the recently completed token sale for Sirin, which seeks to integrate decentralized applications into its blockchain-based mobile device.

- TON DNS – "A service for assigning human-readable names to accounts, smart contracts, services and network nodes." Both MaidSafe and Blockstack, which raised $50 million on an ICO in December, fall into the same category.

The company's ICO plans must have come together quickly, according to the former chief technical officer at VK, Anton Rozenberg."While I was working at Telegram, cryptocurrencies, ICO, blockchain, etc were never discussed," Rozenberg, who left the company in April of last year, told CoinDesk.

Still, many remain, if nothing else, wow-ed by the expanse of the project.Eduard Gurinovich, a Russian entrepreneur and founder of MyTime, which plans on launching an ICO in March, told CoinDesk:"Gram ... is declared, essentially, as a new dawn for P2P. This is something that could compete with bitcoin. Gram has the chance to realize its full potential. This is the winning bid for Gram as a new accounting currency, not an investing one."

Telegram Messenger image via Shutterstock

The leader in blockchain news, CoinDesk is an independent media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies.

Interested in offering your expertise or insights to our reporting? Contact us at [email protected].

Disclaimer: This article should not be taken as, and is not intended to provide, investment advice. Please conduct your own thorough research before investing in any cryptocurrency.

Did You Know About This?

You can curate a Personal Blockchain Page right here on Blockchain Company ( BC ) like these 2 great user examples here:

http://www.blockchaincompany.info/Paula

http://www.blockchaincompany.info/Francisco

Share your blockchain page with your employer, colleagues and friends. It demonstrates your professional awareness and competency of this revolutionary paradigm called the blockchain changing our world. It's free if you are a consumer user to curate on BC. Just Create your Account here in less than 3 mins!

Or Click " Create Account " above in the upper right corner. Instructions how to curate your blockchain page from information you discover on BC, is sent in your email after you sign up, so read it. It takes only a few minutes to curate your blockchain page. You can then track and share all the content you love or care about to enhance your knowledge of the blockchain and cryptocurrencies in general.

You can send message over our network, invite friends, your employer and colleagues to follow your Blockchain Page too! You might still be able to capture your ' first name " as a unique url for your blockchain page too! Like : http://www.blockchaincompany.info/robert We recommend you do this sooner as easy memorable BC urls will get snapped up quickly.

Going forward, you may also be entitled to free cryptocurrency tokens through airdrops with our partners and our own utility tokens. You may also get unique offers and discounts at any time in the future, once you are a user on our BC platform.

Blockchain is the Internet of Value...

you need to start participating today and be part of it!

-

Admin

- 0 comments

- 1 like

- Like

- Share