List MW

-

Fervent blockchain supporters claim the technology has the potential to transform the world we live in – and venture capital investors (VCs) are paying attention.

Fervent blockchain supporters claim the technology has the potential to transform the world we live in – and venture capital investors (VCs) are paying attention.

With hefty funds to deploy, and returns to make for their limited partners, it’s common knowledge that VCs are always looking for the next big thing.

A huge part of their job entails evaluating nascent technologies to separate innovative companies doing revolutionary work from more derivative projects – and blockchain is no exception.

In fact, research released last year showed that the number of VC blockchain deals doubled in the 12 months up to October 2018, by which time investors had already poured $3.9 billion into companies across the globe.

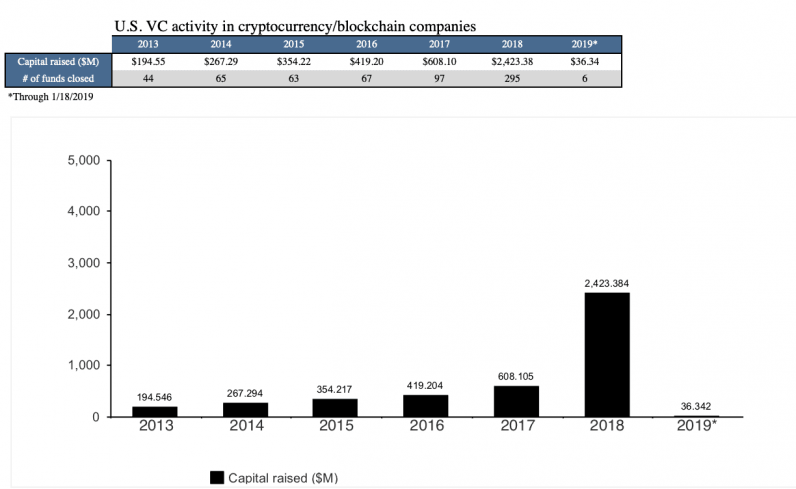

According to Pitchbook data shared with Hard Fork, venture capital investment in the US cryptocurrency and blockchain space has been steadily increasing year on year – going from a mere €14.43 million in 2013 to €723.13 million last year. The number of funds closed has increased, too (17 in 2013 and 106 in 2018).

Courtesy of Pitchbook

Back in 2017, a TNW contributor argued that Initial Coin Offerings (ICOs) would render traditional VCs a thing of the past, but a different story has played out all-together.

At Hard Fork, we want to know what piques investors‘ interest, what drives them to back certain companies, what they’re uninspired by, and why.With this in mind, we reached out to notable figures to find out what’s driving investment in the space.Viable solutions

Octopus Ventures Zihao Xu’s first encounter with Bitcoin took place when a friend emailed him the cryptocurrency‘s whitepaper in 2012. At that time, a coin’s price oscillated between $5 and $13 throughout the year.

“I found it really intriguing as I’d been interested in the idea of denationalized money since my university days,” Xu told Hard Fork.

Xu believes those interested in Bitcoin‘s underlying blockchain technology before the asset price took off fall into three categories. First, the tech enthusiasts who were interested in the code element.

Then, those in finance who figured out they could trade Bitcoin and potentially make money. Finally, the libertarians who saw the potential of censorship-resistance, decentralization, and a free market for money.Initially, Xu fell into the latter camp, but fast forward seven years and his vision for blockchain technology has altered significantly.I no longer think blockchains are the most elegant or suited type of database. In fact, the idea of using a blockchain to distribute a database is probably the most crude one conceptually – giving every node a full copy of the entire database is old-fashioned.

Xu wants to find viable blockchain solutions which could help the technology achieve mainstream adoption. He’s trying to avoid companies that use blockchain for the sake of it, or because it’s a buzzword that’s likely to entice investors.

“We look for companies or projects building something with the core value that comes from a set of functions native to [decentralized ledger technology] (DLT), and cannot be attained in the absence of DLT.”“Right now, only a small handful of projects fits this criterion, but cryptocurrency functionality is improving and expanding all the time,” he added.Tech convergence

Jamie Burke came across Bitcoin entirely by chance.He became so enamored with the technology that he set up Outlier Ventures – credited with being Europe’s first dedicated blockchain VC and venture platform – in 2014.

At the time, Bitcoin hovered around the $300-$400 mark and there seemed to be little, or no, interest outside of the academic and developer community.But things changed quickly. A year later, in the Summer of 2015, Ethereum – the brainchild of Vitalik Buterin, Gavin Wood, and Joseph Lubin – burst on the scene.

“When Ethereum came along and introduced their vision for a virtual machine as well as the way they financed the project through what was only the second ICO at the time, it became clear this promised to be as transformational as The Web was in the 1990s and [it] was something we had to be part of,” Burke told Hard Fork over email.

It was then that academics’ and developers’ interest in the technology started to transcend into the commercial arena, with Microsoft sponsoring Ethereum’s DevCon One conference that same year.

Burke says he’s been bullish about the underlying potential of decentralized ledgers from the very beginning.What’s been surprising to me is how quickly startups in this space have rushed to codify assumptions into their design decisions before testing and validating them. Equally, I have started to realize just how much cultural baggage ‘crypto’ owes to the field of cybernetics, the new communalism of the 60s, and its merging with the libertarian right of the 90s.

Burke thinks the current cryptocurrency winter, which has resulted in some companies making significant layoffs, will be hugely positive for the space in the long-run.

The perceived scarcity of funds in the blockchain and cryptocurrency space, Burke believes, will force founders to concentrate on what really matters: building usable products to solve real-world problems, and in turn, achieve adoption. It’s basically the survival of the fittest.

“We speak to over 100 inbound projects a month and have met over 1500 blockchain startups since our founding. Many don’t go beyond the first round of due diligence because they have no experience or understanding of the industries they want to touch or are too dogmatic,” Burke noted.

He believes the real value will be found where, and when, blockchain helps enable other technologies such as artificial intelligence, internet-of-things, as well as augmented and virtual realities.

It will be then that blockchain will serve as a viable solution to store the increasing abundance of data required to power advancements in these fields.“We definitely don’t look at blockchain and cryptocurrency in isolation,” he explained.Staying close to the problem

Burke is not the only investor to think that blockchain technology’s success – and therefore its potential viability as an investment – will rely on its convergence with other technologies.Sherman Lee, a partner at early stage accelerator program Zeroth AI, agrees.Lee discovered Bitcoin in 2014.

Three years later he began to look at blockchain technology as a solution to a problem he’d encountered with AI training.“During the great bull run of 2017, the euphoria was incredible. Hundreds of teams kept popping up with whitepapers with amazing visions. As an engineer, I was quite skeptical on the ability of all these teams to deliver on their promises of 1 million transactions per second. As an investor, well, it didn’t matter because we started seeing parabolic gains on our investments.”

A year later, everything changed. The bear market of 2018 brought everyone back to reality. Token prices crashed, leading to projects and companies running out of cash, with many ceasing operations completely.“Many thought cryptocurrency was dead, but not me. As an engineer, I saw real technology being built by incredibly talented people.

All the scammers and speculators have mostly disappeared. All the noise is gone. We now have left only the strongest teams. These are the ones that will survive,” he said.Lee wants founders who are “super close” to the problem they’re solving and understand that to be a sustainable blockchain company, you have to have a path to revenue.

“The ability to self reflect is also valuable. Many companies got caught up in the ICO hype and now they have to clean up the mess,” Lee added.Data, data, data

Will Orde, a technology investor at Oxford Capital, discovered cryptocurrencies in 2015, when Bitcoin‘s value moved between $200 and $500. Two years later, in 2017, Oxford Capital began to seriously explore applied uses of blockchain technology.

“When I started looking at cryptocurrencies in 2015, the core premise was focused on digital currencies – Bitcoin being the most famous. But over time I think the more interesting applications (in the immediate future) are using distributed ledger technology in more practical situations, particularly around data.

”As a fund, Oxford Capital wants to back companies at the point where products first hit the market – and blockchain is no different.“Recently I’ve been focusing on use-cases revolving around the creation, sharing and management of data in multi-party situations.

You can find situations like this in many sectors, from insurance to personal identity.”Importantly, though, Orde is quick to point out that, like many others in the market, he’s not interested in blockchain companies looking for a problem to solve.He wants “someone with a clear vision for what they’re building, a balanced skill set, and an ability to get stuff done”.Real innovation

Alicia Garabedian also discovered Bitcoin in 2015 when she was working at Morgan Stanley.Real exposure to the blockchain ecosystem, though, came in 2017 when she joined Samsung Next, where she’s an investor.

When she first came into the space, Garabedian thought cryptocurrencies were about speculation, and admits she didn’t really understand the underlying blockchain technology.

“As I learned more, I became captivated by the speed of industry, the growth of the ecosystem and intrigued by the influx of ambitious entrepreneurs,” she shared with Hard Fork.Today, Garabedian is looking for real applications, actual enterprise implementation, and consumer adoption.“We are interested in the deep, enabling technology that capitalizes on the potential of blockchain. We look at companies that are doing something new and innovative with blockchain, as opposed to leveraging it as, say, a data store. In this sense, we are less interested in companies that are trying to put something on the blockchain, or creating a token, without clear justification or end game.”

In her experience, blockchain technology proves to be useful when there’s an issue that lacks distribution, not only geographically, but organizationally.

But, will investment in cryptocurrency and blockchain startups continue to rise or stagnate?

Well, it’s highly likely the number companies that raise considerable amounts via ICOs will stagnate, and those building a solution without a problem will struggle (or even cease to) exist.It seems that, somewhat predictably, the future looks bright for blockchain businesses which fundraise reasonably with a clear path to monetization.

A clear value proposition and a solid market strategy are also a must. This is what’s really attracting investors and that’s unlikely to change.

-

- 1

Francisco Gimeno - BC Analyst This is one of the most clear articles we have read related to the status of the ICOs in 2019. Different opinions but all understand that the blockchain Wild West is not needed anymore, and only serious projects with serious value proposition, strategy and team will get funds from investors. This is the beginning of a new stage for all things blockchain.

-

-

The Synaptic Health Alliance: A Look at how Blockchain Technology Could Improve Provider Data Quality

Blog Healthcare Law Blog

Sheppard Mullin Richter & Hampton LLP

MEMBER FIRM OF

In 2018, five major healthcare companies – Humana, MultiPlan, Optum, Quest Diagnostics, and UnitedHealthcare – formed the Synaptic Health Alliance (the “Alliance”) to explore how blockchain technology could resolve current healthcare issues.

The Alliance launched its first pilot program in April 2018 to focus on specific ways that “blockchain technology can help ensure the most current information about healthcare providers is available in the provider directories maintained by health insurers.

”[1] Aetna and Ascension joined the Alliance in December 2018, thus adding additional resources and unique perspectives to the effort of streamlining provider data management.

[2]What is Blockchain?

As described in a March 1, 2018 article, “How Blockchain Can Impact Healthcare” authored by James Gatto, Esq. and posted on the Law of the Ledger: Legal Issues with Blockchain and Cryptocurrency Blog, a blockchain is, at its core, a distributed ledger for recording transaction data. In short, a blockchain can aptly be described as a simple list of transactions.

Traditional paper-based ledgers include consecutive pages in which each line records a transaction. When a ledger page is full, the process repeats on the next ledger page. In the case of a blockchain, each block is like a page. Transactions get verified and written into a block and when the block is full, a new block is created.

Unlike traditional paper-based ledgers, when a block is full, the system creates a hash value, which is just a random number generated by an algorithm based on the contents of the block. This hash value is then written as the first entry in the new block, thereby “chaining” together the blocks, hence the term “blockchain.

” If someone ever attempts to change an entry in a prior block, the hash value would no longer match what was written into the new block and that attempt would be deemed invalid.

In part, this is how blockchain creates unalterable records.Current Challenges Surrounding Provider Data ManagementHealth plans are required to actively maintain and update their provider directories to meet both federal and state regulatory requirements.

Provider directories include vital information for determining coverage for patients, including contact information for providers, information about plan participation for individual providers, and information regarding whether an individual provider is accepting new patients.

Approximately $2.1 billion is spent annually by insurers, doctors, and hospitals to maintain this provider data.[3]In addition to astronomical costs, current provider directories often contain inaccurate or outdated information.

The Centers for Medicare and Medicaid Services reviewed a pool of Medicare Advantage Organizations and found that “52.20% of the provider directory locations listed had at least one inaccuracy.

”[4] The inaccuracies included incorrect address information, errant phone numbers, and misidentification of a provider as presently accepting new patients, when the provider was not.[5]Inaccuracies in provider directories routinely result in issues with coverage for patients.

A survey conducted by the American Medical Association and LexisNexis® Risk Solutions found that 52% of physicians in the United States “say they encounter patients every month with health insurance coverage issues due to inaccurate directories of in-network physicians.

”[6]Blockchain as a Potential SolutionThe Alliance has assessed this current system as inefficient due to the duplicative efforts of health plans that “typically maintain their own provider data sets and rarely collaborate on the daunting task of provider data management.

”[7] The end result being redundant administrative expenses and silos of disconnected data.

[8]The Alliance considers blockchain to be a technology that could streamline the current process for maintaining accurate provider data. The Alliance “plans to build a permissioned blockchain that would let members view, input, validate, update and audit non-proprietary provider data within the network.

”[9] Specifically this blockchain solution could:- Improve interoperability among stakeholders by creating “a synchronized, shared source of high-quality provider data” that would be stored via blockchain and begin to connect the currently separated data silos;

- Improve data integrity by creating a tamper-resistant, chronological record of each transaction which will “remain visible and unchanged, providing a real-time audit trail;” and

- Allow “participants to share some of the administrative burden and cost of data maintenance and reconciliation” thus reducing administrative costs for each member.

- [10]

Sheppard Mullin Richter & Hampton LLP - Samuel Gilkeson and John M. Tilton-

Francisco Gimeno - BC Analyst Another well thought pilot use case for the health sector where data handling is crucial both for everybody involved, from providers to customers. Saving money and time is the easiest consequence, but also who controls what, who handles what data and why is tremendously important. A new era in this sector is arriving.

-

Cryptopia In Crisis: Joe Lubin’s Ethereum Experiment Is A Mess. How Long Will He Prop It Up?

Jeff Kauflin

Forbes StaffFintechI cover fintech, cryptocurrencies, blockchain and investing.

Sarah Hansen

ContributorFintech

Ayear ago, Joe Lubin seemed like one of the most prescient people on the planet. Cryptocurrencies like ether were in the midst of a hockey-stick ascent, and Lubin, a cofounder of the Ethereum blockchain and one of its most articulate pitchmen, was scheduled to speak at events from Davos to SXSW. At his firm’s “Ethereal Summits,” it was standing room only, with crowds hanging onto his every utterance, no matter how bizarre.

At one event in San Francisco in October 2017, he scolded attendees for hitting their television sets and for being rude to Siri, Apple’s digital assistant. “We designed Ethereum to enable machines and bots to be first-class citizens,” Lubin said with straight-faced sincerity as he espoused visions of decentralization, self-sovereignty and a democratized global society.

“So be nice to the machines of this generation, lest some future artificial general intelligence who feels that you have been disrespectful to her ancestors decides to turn your carbon into something more useful to the future machine economy.”

On the hunt for new blockchain projects from ConsenSys’ San Francisco office, CEO Joe Lubin is certain the sun will come out tomorrow for crypto, despite its current dark days.

TIMOTHY ARCHIBALD

Lubin’s quip drew laughter, but in the autumn of 2017 the idea that blockchain—the distributed database technology underlying virtually all cryptocurrencies—would usher in a new world order didn’t seem far-fetched at all.

The price of a single ether token, a digital representation of money that’s similar to bitcoin, had just pierced $300, up from about $10 at the beginning of 2017. It was on its way to a peak of $1,389 within the next three months.

Forbes would soon name Lubin the second-richest person in crypto, worth as much as $5 billion, based largely on reports that he owned between 5% and 10% of all the ether in circulation, which by the beginning of 2018 had a market value exceeding $100 billion.

“The potential of this technology is just enormous,” Lubin, 54, tells Forbes in a recent interview. “It’s many orders of magnitude more valuable than [where the tokens] are sitting right now, because it’s going to permeate all aspects of society. We’re going to build everything on this technology.

”Back in late 2014, a few months after ether launched via crowdsale at 30 cents per token, Lubin created ConsenSys, a holding company he grandiosely describes as a global “organism” to build the applications and infrastructure for a decentralized world. In actuality, it is the first crypto conglomerate, comprising a network of for-profit companies supporting bitcoin’s biggest blockchain rival, Ethereum.

More than 50 businesses were quickly spawned out of its Brooklyn headquarters, ranging from a poker site and a supply-chain company to a prediction market, a healthcare-records firm and a cybersecurity consultancy.

But there were no fundraising rounds or debt offerings. In Lubin’s version of the decentralized future, he is the architect, CEO and central banker, funding all of ConsenSys’ “spokes” from his personal cryptocurrency stash. Lubin has yet to veer significantly from this master plan, despite serious cracks in its foundation.

For one thing, the Ethereum blockchain faces strong headwinds. Thanks to its perceived technical superiority—largely because it allows apps to be “embedded” in the blockchain—Ethereum became the launching pad for hundreds of initial coin offerings (ICOs), many of which in aggregate resulted in billions in losses for their supporters.

The crypto landscape is littered with the carcasses of ill-fated Ethereum-based ICOs, and now the SEC and other regulators are targeting some of them for enforcement action. In November, the SEC settled actions against two Ethereum-based startups, Airfox and Paragon, which had effectively sold $27 million in unregistered securities when they issued their ICOs in 2017. Both tokens are now basically worthless.

Meanwhile, rival app-supporting blockchains like EOS, which processes nearly ten times as many transactions a day, and Dfinity, which recently raised $102 million from investors such as VC firm Andreessen Horowitz, are challenging Ethereum.

But almost all blockchain technologies remain glacially slow. Ethereum can process only about 20 transactions per second. By contrast, Visa can handle 24,000. Yet Lubin’s organism keeps growing. ConsenSys has 1,200 employees, and some 200 job openings are posted on consensys.net.

Though ConsenSys declined to comment, Forbes estimates that almost all of its businesses are in the red, some with little hope of profitability. Lubin’s global organism appears to be burning cash at a rate of more than $100 million a year.

When worried staffers have questioned Lubin about ConsenSys’ sustainability, Lubin has always had a pat reply: “Joe would say, ‘This is definitely not something you need to worry about. We can go on at this pace for a very, very long time,’ ” recalls Carolyn Reckhow, a former director of global operations who left ConsenSys in May.

With the price of ether in free fall, down from $1,389 to barely more than $100 today, Lubin’s fortune may have dwindled to less than $1 billion, calling into question how long he can continue to fund his dream. It all depends on how much ether he sold—and when.

Like Ethereum’s other cofounders, Vitalik Buterin and Anthony Di Iorio, Lubin grew up in Canada.

A self-described computer nerd whose father was a dentist and whose mother was a realtor, he attended Princeton in the mid-1980s, where he played squash and was roommates with future billionaire hedge fund star Mike Novogratz, who, like Lubin, would ultimately pivot toward blockchain and crypto.

After graduating in 1987 with a degree in electrical engineering and computer science, Lubin started in tech at Princeton’s robotics lab, but he eventually made his way to finance, building software for Goldman Sachs and later running a successful quant hedge fund.

Lubin’s office was not far from Ground Zero during the September 11 attacks, and the harrowing experience threw him into an existential crisis. Over the ensuing decade he became deeply depressed about the state of the world.

“It was folly to trust all those structures that we implicitly felt had our best interests at heart. … I felt we were living in a global society and economy that was figuratively, literally and morally bankrupt,” he said at ConsenSys’ Ethereal Summit in May 2017.

“I was confident that our economy and society were in a slow, cascading collapse.” Lubin foresaw two equally catastrophic outcomes: Central bankers would eventually debase currencies to pay off mounting debts, stifling growth for decades, or some unexpected “nonlinear” event would create great hardships and send the world into the worst economic depression it had ever seen.

So distraught was Lubin that he traveled to Peru and Ecuador looking for land he could escape to.Then in early 2011, Lubin read the bitcoin white paper and had an epiphany: “Decentralization was a game-changer.” Lubin’s global “organism” appears to be burning more than $100 million a year, yet ConsenSys is still expanding.

Lubin’s global “organism” appears to be burning more than $100 million a year, yet ConsenSys is still expanding.

Reading all he could on bitcoin, Lubin was eventually introduced by Di Iorio to Vitalik Buterin, Ethereum’s then 19-year-old creator and boy genius of crypto.

Having read Buterin’s November 2013 Ethereum white paper, Lubin got in on the ground floor of the Ethereum project and attended the group’s foundational meeting in Miami in January 2014.

He continued as part of the core group through Ethereum’s $18 million initial coin offering in July 2014 and was rumored to be one of the biggest buyers during the token’s initial crowdfunding, at prices estimated to be well below a dollar. Ultimately, Ethereum’s founding team bickered and parted ways. Buterin continued to focus on the technology, while Lubin hatched his plan to create a business ecosystem around Ethereum.

For ConsenSys’ headquarters, Lubin chose the hipster-heavy Bushwick neighborhood of Brooklyn. From the outside, 49 Bogart Street looks dingy: The door is covered with the kinds of stickers you’d see in a bar bathroom and is surrounded by graffiti.

The interior isn’t all that different. ConsenSys occupies multiple lofts alongside residential apartments.When it came to organizational structure, Lubin wasn’t having any of the typical corporate hierarchy. His ConsenSys would be a so-called holocracy—no managers or reporting structures. Decision-making would be decentralized, and employees could choose their own titles.

Few had permanent desks. “Every day, it was so lax that I’d walk in and didn’t know if I had a seat. Literally, it was like Game of Thrones,” says Jeff Scott Ward, who joined ConsenSys in June 2015 and left the company in early 2018. There was one toilet for 30 people on the floor, Ward says.

The company didn’t hire a human resources person for almost a year and a half. ConsenSys’ first projects, or spokes, included accounting software for cryptocurrency transactions and a blockchain-based digital-rights platform for musicians.

Most of the ideas for spokes came from ConsenSys employees, and once a project was approved, Lubin would give the startup between $250,000 and $500,000 to get it off the ground.

The goal was for the spokes to become self-sustaining businesses, and in an effort to foster this, they would occasionally be spun out into their own legal entities. Lubin’s broader goal is to turn his Ethereum ecosystem into a what he calls a mesh, whose strength is derived from the spokes’ inter-connectivity.

Only a handful of the spokes ConsenSys has launched have gained traction. Balanc3, the accounting software project, says it has more than 25 business customers (though it won’t specify any), each paying at least $25,000 a year. Another, Kaleido, helps companies implement blockchain technology.

It has 1,900 users and says it just began charging for its services. Amazon Web Services recently announced that its ubiquitous hosting platform is compatible with Kaleido’s blockchain offerings. ConsenSys has built technical tools for Ethereum that programmers have downloaded millions of times, but the company doesn’t charge for them.

Lubin has been less rigorous than traditional venture capitalists in approving projects. “Joe is the kind of person who tends to want to keep his options open and say ‘Yes, why not?,’ ” says Reckhow, who’s now head of client services and operations at Casa, a crypto-wallet company.

“He’s lucky to be in a position where that works well, but he’s not as good at prioritizing. He’d rather say yes to everything. ”Being the Daddy Warbucks of the Ethereum blockchain is fine when digital money is trading at stratospheric levels, but as cryptocurrency enters another bear market, Lubin, who admits to periodically selling crypto to fund operations, may need to start pulling some plugs.

In 2017, Mark Beylin, a student at the University of Waterloo in Canada, came to Lubin with the idea for Bounties Network, a marketplace for freelance jobs that’s similar to the popular website Upwork but uses Ethereum’s smart-contract technology, which helps with billing.

After one year in operation, Bounties Network has seven people working on it and just $400,000 in total “bounties,” or offers for jobs, which range from $171 for an 800-word blog post on the future of work to $67.30 in exchange for translating a white paper into Portuguese.

Bounties Network has generated revenues of less than $50,000 so far.In October 2016, Jared Pereira, an 18-year-old high school graduate living in Dubai, pitched Lubin on Fathom, which aims to somehow disrupt the higher-education business by crowdsourcing academic evaluations and grading.

Lubin gave the go-ahead, but two years later the project has six people working on it and no launchable prototype.

Its website is nothing more than a few pages stating high-minded ideals: “If individuals were free to build their experiences tailored to their unique aims, and were able to communicate those experiences reliably to any entity in the world, there would be an order of magnitude shift in the efficacy of social organization at every scale.

”Other projects that have been staked by Lubin seem even flakier. Cellarius, a spoke that Lubin often promotes by wearing an eponymous T-shirt, is a “transmedia cyberpunk franchise” aimed at collaborative storytelling on the blockchain. What exactly is collaborative storytelling, and why will the blockchain make it better or more profitable? Its website’s explanation is far from clear.

Lubin insists ConsenSys is getting more selective in picking projects. But old habits die hard. In October it bought a nine-year-old asteroid-mining company called Planetary Resources.

“We see it as a group of amazingly capable people who are interested in exploring how blockchain could ramify on space operations,” Lubin says abstrusely.

Civil, a spoke that aims to put journalism on the blockchain and is supposed to somehow increase the level of trust in news, recently had to cancel its ICO because it failed to raise its minimum target of $8 million.

Some of the journalists in Civil’s 18 newsrooms say they have yet to receive compensation in the form of tokens they were promised. (Disclosure: Forbes recently announced a partnership with Civil.)

Vitalik Buterin’s 2013 Ethereum white paper gave Lubin a new lease on life. GORDON WELTERS/LIAF/REDUX

ConsenSys also offers consulting services, essentially assisting companies in becoming blockchain-literate. To date, this is the best business ConsenSys has. In the short run, these services will succeed—until companies wake up and realize that blockchain isn’t necessarily better for most things and is sometimes worse than other technologies.

ConsenSys consultants helped create Komgo, for example, a consortium of 15 big banks that includes Citi, BNP Paribas and ABN AMRO. Komgo wants to use the blockchain to bring efficiency to the financing of goods shipped around the world, like oil. ConsenSys consultants are also working with UnionBank in the Philippines to speed up money transfers.

In the past year, ConsenSys’ consulting arm has grown from 30 employees to more than 250 and, according to Lubin, is bringing in “tens of millions of dollars” in the form of cash and equity stakes. As for ConsenSys’ spokes, which are mostly applications and developer tools, Forbes estimates the whole lot of them won’t generate more than $10 million in revenues in 2018.

So far, ConsenSys’ biggest non-consulting successes are its tools for Ethereum programmers. Its MetaMask product, which lets users log in to Ethereum from a Web browser, has more than one million downloads (all of them gratis). Truffle, which helps developers manage and test parts of their code for building Ethereum applications, has also cleared one million free downloads.

It can be difficult to charge real money for these tools because of the communal, quasi-anarchist nature of the blockchain developer community. ConsenSys claims it will soon start charging for Infura, another tool that facilitates access to Ethereum.

“ConsenSys has done more for the Ethereum ecosystem in its first five years of development than any other firm,” says Meltem Demirors, chief strategy officer at CoinShares, a crypto-asset-management company.ConsenSys will end up in the Harvard Business Review as a case study on changing corporate structure or as a disaster.

None of this seems to phase Lubin, who is clearly not launching projects to make profits. “The intention isn’t to create companies and send them out and make money,” he says. “The intention is to create an ecosystem. It really is very family-like.

” However, Lubin also acknowledges that changes are in order and recently sent a memo to his staff about becoming leaner and more focused.

“In ConsenSys 2.0,” Lubin says, “we’ll pay more attention” to the market-based hurdles that traditional startups have to clear. And he’s not ruling out layoffs—even in its consulting business.

The biggest problems at ConsenSys may have less to do with plunging crypto prices and Lubin’s dwindling fortune than with his conglomerate’s weird operating structure.

ConsenSys would like to believe that it’s reinventing the future of work and business. As you enter ConsenSys’ hacker-chic Brooklyn digs, there are lots of antiestablishment touches, including a large banner on the wall that reads, “Welcome to the decentralized future.” In fact, CEO Lubin tries not to tell people what to do.

“He wants to be like the anti-CEO or the anti-founder,” says Jeff Scott Ward, a former employee who thinks this is partly because Lubin is a nice guy who wants to be democratic.

But there are some not-so-nice consequences of having Mr. Nice Guy in charge. At ConsenSys, there’s less incentive to meet deadlines and make fast progress. “In a lot of ways, there still isn’t pressure to generate revenue or hit targets that normally Silicon Valley VCs and businesses would be looking for,” says Griffin Anderson, who leads the Balanc3 spoke.

One Glassdoor commenter describes ConsenSys as a place with “unlimited funding and no pressure to actually deliver anything.” The lack of traditional structure has also spawned ugly politics. “It feels a little like Survivor,” says Lucas Cullen, a former employee. ConsenSys staffers who are close to Lubin get faster access to resources, says a former employee, and accountability varies widely from team to team.

ConsenSys does have Resource Allocation Committees, which are charged with deciding whether spokes will continue to receive additional engineers or funding. But the committees are in a constant state of flux.

“There’s always one person from finance, but they’re generally made up of people who have an interest in your area,” says Thomas Hill, a cofounder of Truset, a ConsenSys spoke that’s building a crowdsourced business data platform.

“Anyone can sign up for an RAC.” According to Ward, who spent three years at ConsenSys, “There were too many cooks in the kitchen. It was like, Whose ego is the strongest? It was exhausting,” he says.

UPort, a tool aimed at letting users log in to Ethereum applications, had three project managers, who couldn’t align on a single vision. Today there are just 15 applications using UPort, and the project is splitting in two.

Many describe ConsenSys’ culture as chaotic, and the company seems to have trouble keeping track of its projects. ConsenSys’ homepage says it has “50+ spoke companies,” but during the reporting of this story, the number ranged from “more than 30” to, most recently, 42. It’s a “fluid number,” says a company spokesperson.

Lubin acknowledges some of these difficulties. “[Accountability] has been an issue at ConsenSys,” he says. “We’ve been working to put in place various mechanisms to make it clearer who’s responsible for what and to ensure crisp accountability.

” But he also cites real benefits to his mesh architecture. Projects are collaborative, and silos are easily breached. Employees report that there is little stigma attached to questioning others’ assumptions. And some insiders report feeling empowered by the autonomy—especially the opportunity to move laterally among projects.

Crypto matchmaker and fellow Canadian Anthony Di Iorio was Lubin’s entre into Ethereum’s inner circle.COLE BURSTON/BLOOMBERG

According to Hill, the Truset cofounder, “ConsenSys will end up in the Harvard Business Review as a case study, either as a lesson on how you change corporate organizational structure or as a disaster.

” If there is a paradox in Lubin’s quest to reinvent business for the coming age of decentralization, it’s that ConsenSys is actually much more centralized than Lubin would like to admit.

When ConsenSys spokes have spun out and become separate businesses, for example, Lubin has retained ownership of 50% or more. Thus, like John Pierpont Morgan and Andrew Carnegie during America’s Gilded Age and tech magnates Jeff Bezos and Mark Zuckerberg of the internet age, Lubin is setting himself up to become one of the controlling titans of the blockchain era.

“This is where the whole mesh-and-decentralization thing falls apart,” Ward says. “It was never clear who had what stake.” In the case of Grid+, one of the projects ConsenSys spun out through an ICO, Forbesestimates that Lubin walked away with no less than 20% of its tokens, in addition to half of its equity.

“I don’t think they even have the slightest idea what decentralization is,” says Demirors of CoinShares. And the issue of sharing ConsenSys’ equity among its 1,200 employees has become a running joke. Former employees report that for a long time Lubin was evasive and the plan was always “six weeks away,” if you asked him.

In fact, the first set of 100 employees or so received their equity in early 2017, and nearly two years later, ConsenSys says, it’s still working on a plan to give its larger workforce a stake in the company.Lubin doesn’t think ConsenSys’ structure presents contradictions.

“If you can build a system that serves many people and they’re all delighted with the system, then the originating structure doesn’t necessarily have to be equally owned by lots of people,” he says, in a response that could have just as easily been uttered by Zuckerberg on the eve of Facebook’s lopsided public offering.

In 2017 ConsenSys was able to use ICOs as an easy and lucrative way to spin companies out and reward internal staff. But now that the SEC is cracking down on ICOs, that window is much smaller. “As we look to make more external investments, there are specific deals where we need to map to a traditional VC model,” says Ron Garrett, head of ConsenSys Labs, the division responsible for deciding which projects become spokes.

“In those deals, we’ll take less equity.” He adds that other startup incubators like Betaworks are known to take -majority stakes in the companies they incubate. So much for democratization and decentralization.

For now, Joe Lubin’s grand experiment in the future of business is racing against a clock: Will blockchain applications achieve mainstream success before Lubin’s largesse is exhausted? Even the most successful applications on Ethereum have tiny user bases. The most widely used application is a decentralized exchange for trading crypto called IDEX, which is unaffiliated with ConsenSys.

After more than a year in operation, it has a pitiful 1,000 daily users. “We knew that it was going to be a lot of work and take a long time before you enable massive evolution on a planetary scale,” Lubin says. If Lubin is still a billionaire, he may be able to sustain ConsenSys for several years—even at its $100 million-plus annual burn rate. “As it stands, ConsenSys is stable and healthy,” he insists.

At what point will Lubin throw in the towel? “I have no exit plan, and I’ve never had an exit strategy for anything I’ve done,” he says from ConsenSys’ San Francisco offices, where he just hosted a “demo day” for 16 startups eager to join his bankroll.

“I’m all in.”Update, 12/7/18: After publication, Bounties Network informed Forbes that it had incorrectly reported its total bounties offered as $250,000.

We've updated the number to $400,000.Reach Jeff Kauflin at [email protected] and Sarah Hansen at [email protected].

Cover image by Filip Peraić.

This story appears in the December 31, 2018 issue of Forbes.

Jeff Kauflin

Forbes Staff

I cover cryptocurrencies, blockchain, fintech and investing at Forbes. I’ve also written frequently about leadership, corporate diversity and entrepreneurs. Before Forbes, I worked for ten years in marketing consulting, in roles ranging from client consulting to talent ma... Read More

Sarah Hansen

Contributor

I write for Forbes’ Money & Markets team. I’ve previously worked at Investopedia, as a breaking news intern at CNBC, and as a radio reporter in Alaska. I’ve written about the NYSE, the rise and fall of General Electric, and emergency care in the Aleutian Islands. Before ... Read More-

Francisco Gimeno - BC Analyst Those old enough will read this article thinking how similar comments were made about Amazon, or YouTube or any Internet start up twenty five years ago. All big companies which burned a lot of money, were seen as "weird" as is written here too, and somehow were vital for all the internet industry development. It is the time now for Lubin and Consensus to evolve and adapt to the new situation but we think (hope) his company and his work will be with us for a long time.

-

-

To help developers at new blockchain startups, and at companies seeking to start using blockchain, IBM has developed the IBM Blockchain Platform Starter Plan to help them build blockchain proof-of-concepts quickly and affordably.

To help developers at new blockchain startups, and at companies seeking to start using blockchain, IBM has developed the IBM Blockchain Platform Starter Plan to help them build blockchain proof-of-concepts quickly and affordably.

It offers an end-to-end blockchain development experience: a secure test environment, a suite of education tools and modules and one-click network provisioning. It is built on the open source Hyperledger Fabric.

IBM logo. (Photo by Chesnot/Getty Images)

More than 2,000 developers and tens of thousands of transaction blocks used the Starter Plan in a three-month test environment, said Jerry Cuomo, vice president of blockchain technology at IBM.

The Starter Plan is for enterprises -- whether startups, large corporations or government agencies -- that want to understand and use blockchain technology, Cuomo said.

It is designed to make the technology disappear so developers can focus on their ideas rather than how to operate a test network.

“Starter is to provide the developers and test environment with single click deployment to enable an aspiring blockchain developer to get started,” he said. “When we put it out there as a beta in March of this year we saw very quick and significant adoption.

We had over 2000 smart contract contributors, developers building contracts on the platform and deploying smart contracts of every variety imaginable,” he added.

The Starter Plan attracted some companies he describes as “born on the blockchain” including Road Launch for logistics, Mediaocean, which automates and tracks digital ad buys, and Global Debt Registry, which helps institutional investors and warehouse lenders manage risk, improve efficiency and pricing in the credit markets by providing solutions that ensure the integrity of a loan asset.

“The Starter Plan is a great place to start because it offers low cost and high value, with the tools we provide on top of open source,” Cuomo said.

For now the plan runs on the IBM cloud although he suggested it may be available on other clouds in the future. Continue to page 2 on Forbes here: https://www.forbes.com/sites/tomgroenfeldt/2018/06/28/ibm-launches-starter-kit-for-blockchain-develo...

-

Francisco Gimeno - BC Analyst We talked about this in March when it was launched. After some months it looks like very successful as the technological tools offered are low cost and high value for companies and start ups on an open source. We have to yet see how it evolves. IBM is strongly betting for Blockchain.

-

-

The EU Blockchain Observatory and Forum has built a new interactive map to highlight Europe’s crypto ecosystem. The map points startups and events in the sector, helping make blockchain enterprise exploration easier. Companies on other continents can also be mapped on the platform.

The EU Blockchain Observatory and Forum has built a new interactive map to highlight Europe’s crypto ecosystem. The map points startups and events in the sector, helping make blockchain enterprise exploration easier. Companies on other continents can also be mapped on the platform.

By

Viraj Shah

Europe’s premier blockchain organization, the EU Blockchain Observatory and Forum has built a new interactive cryptocurrency map for the continent. The map points out crypto companies and highlights related events in an area.

It could help users find informationabout various startups and what they do. The map is open to users from around the world, who can filter results or mark startups in their respective continents.A Map for Detailed Crypto Exploration

The interactive map marks crypto and blockchain companies and provides relevant details of their objectives, purpose, year of establishment, etc. It also displays the website and other important information about the company.

Blockchain events will also be listed on the map for easy access to enthusiasts. Users can create filters in the search criteria to find companies or events in an area or find blockchain initiatives in a certain sector.

The Observatory designed the map with Europe in mind. However, it welcomes global users to add companies and events from other continents too. Currently, only European entities are available. The agency warns users that the map is crowdsourced, but entries are reviewed before submission.

Therefore, it will be vital for users to do their research before adding any companies.The Observatory Takes a Giant Leap With Multiple Projects

The interactive map project was first announced In March. The agency stated that they are:“Creating a public map of existing blockchain initiatives; regrouping key players, projects, and regional activities driving the ecosystem’s development. The end result will be a dynamic, geographical map, available on the Observatory and Forum website. Such map is highly valuable for both the European Union and other participants in the blockchain ecosystem.”

Every company submission takes 10 to 15 minutes, for which a user needs to fill a form. Event submissions are made through a separate form.The agency has been very active recently in educating citizens about blockchain and cryptocurrencies.

Apart from several workshops, it also announced a 90-minute ‘Ask Me Anything (AMA)’ session on its website to answer questions related to the blockchain, its use cases and its future in the world.

https://blokt.com/news/an-interactive-map-lets-you-explore-eus-cryptocurrency-startups

-

Admin

Admin - 0 comments

- 10 likes

- Like

- Share

-