Research

-

The bestselling author and historian offers his predictions on how technology will alter the evolution of humans and change society. Anderson Cooper reports.

The bestselling author and historian offers his predictions on how technology will alter the evolution of humans and change society. Anderson Cooper reports.

"60 Minutes" is the most successful television broadcast in history. Offering hard-hitting investigative reports, interviews, feature segments and profiles of people in the news, the broadcast began in 1968 and is still a hit, over 50 seasons later, regularly making Nielsen's Top 10.

Subscribe to the “60 Minutes” YouTube channel: http://bit.ly/1S7CLRu

Watch full episodes: http://cbsn.ws/1Qkjo1F

Get more “60 Minutes” from “60 Minutes: Overtime”: http://cbsn.ws/1KG3sdr

Follow “60 Minutes” on Instagram: http://bit.ly/23Xv8Ry

Like “60 Minutes” on Facebook: http://on.fb.me/1Xb1Dao

Follow “60 Minutes” on Twitter: http://bit.ly/1KxUsqX

Subscribe to our newsletter: http://cbsn.ws/1RqHw7T

Download the CBS News app: http://cbsn.ws/1Xb1WC8

Try Paramount+ free: https://bit.ly/2OiW1kZ

For video licensing inquiries, contact: [email protected]-

Admin

Admin - 0 comments

- 1 like

- Like

- Share

-

-

A perennial question surrounding blockchain technology is: When will it make a mainstream impact?

A perennial question surrounding blockchain technology is: When will it make a mainstream impact?

Understandably, enthusiasts in the industry are anxious to see this technology live up to its promise of empowering consumers, accelerating cross-border payments and bridging the financial inclusion gap for the under- and unbanked.

The reality is that today, its scope is limited. From what little data we have available about cryptocurrency adoption, we see that the pool of active users is relatively small in size and scope — largely millennial and largely male.

Related: Crypto could save millennials from the economy that failed them

Some countries have proven to be trendsetters; for example, one survey showed that 32% of respondents in Nigeria, Africa’s largest economy, said they’ve used or owned cryptocurrency.

To put that into perspective, only 7% said the same in the United States and 8% in China.In part, this limited adoption can be attributed to the fact that today’s products are designed for users who know what they’re doing.

It’s designed for people who know or are willing to learn the hoops they need to jump through to take their financial assets from fiat into crypto and back again and the benefits of doing so.

Crypto utility — that allows people to use it in their daily routine — will come from putting in the time to develop the right foundational infrastructure.

This infrastructure will enable some of the most powerful crypto use cases, such as hedging inflation in volatile economies, enabling remittance and cross-border solutions, paying bills, and charging for goods and services as a merchant.

Stablecoins — tokens backed by fiat currencies — are essential to that infrastructure; they create a bridge between the digital and physical worlds, between virtual and physical value.

They make digital currency useful so that they can be quickly and efficiently traded, exchanged, saved and spent — no matter where you are in the world. They represent the promise of blockchain technology.But stablecoins won’t be useful on their own.

They need a simple platform that makes it easy for consumers to use digital assets. Many of today’s platforms are designed for traders, sophisticated investors and experienced crypto adopters, not your average retail users.

Driving greater blockchain adoption will rely on creating platforms that are accessible and familiar to consumers so they can trust in connecting their digital and physical assets.

With mainstream consumers in mind, platforms that obfuscate the blockchain back-end should be designed in a way that is intuitive and integrates customers’ current digital habits.Blockchain for business

That last component is essential for building the right infrastructure for greater blockchain adoption. However, it nevertheless requires a business-to-customer focus, as well as business-to-business.

Blockchain infrastructure should be readily available and easy to integrate for businesses.

In its most recent analysis of the blockchain landscape, Big Four audit firm Deloitte argues that the appeal and sustainability of this technology hinge on “its use of digital assets and the roles those assets will play in the future of commerce.” To get there, it requires making crypto and crypto wallets business-friendly.

With digital payments on the rise, both e-commerce and brick-and-mortar — or, more generally, online and offline — businesses already have to adapt quickly to new payment methods.

To incentivize them to see blockchain and innovations like stablecoins as a compelling addition (or alternative), there needs to be the right infrastructure, such as one-stop API endpoints so shops and businesses can offer crypto payment methods without bearing a significant operational burden.

Building infrastructure with B2B in mind and creating the ecosystem to support it ultimately drive greater consumer adoption because it means blockchain technology is available where consumers use it, delivering portable, universal money that can be used across business platforms.

The momentum is here to move blockchain technology into the mainstream. In the same Deloitte survey, 89% of respondents said that they believe digital assets will be very or somewhat important to their industries in the next three years.

Now it’s up to us to build this technology to get the infrastructure right and prove that blockchain can live up to its promise.

This article was co-authored by Lisa Nestor and Mary Saracco.The views, thoughts and opinions expressed here are the authors’ alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.-

Francisco Gimeno - BC Analyst The blockchain is coming into business because shows is useful for solving problems with more agility, saving money and time. However, crypto and tokens, theoretically aiming for the same, have a long way yet to be globally accepted, not just for its volatility, but also because is not user friendly or seen as useful yet except for some investors and few people doing transactions in emerging economies who prefer crypto to their useless national money. China can be the first to try to make it streamlined and easy to use for its citizens.

-

-

The University of Cambridge and the school’s Centre for Alternative Finance has published the third “Global Cryptocurrency Benchmarking Study.” The 71-page in-depth study examines the current growth of the crypto industry, mining, offchain activity, crypto asset user profiling, regulation, and security.

The University of Cambridge and the school’s Centre for Alternative Finance has published the third “Global Cryptocurrency Benchmarking Study.” The 71-page in-depth study examines the current growth of the crypto industry, mining, offchain activity, crypto asset user profiling, regulation, and security.

The September 2020 third edition of the Global Cryptoasset Benchmarking Study concentrates on four market segments which include mining, payments, custody, and exchange.

A great number of participants from the cryptocurrency industry took part in the University of Cambridge (UC) study including wallet providers, exchanges, miners, cloud mining providers, crypto custodians, and more.

The 71-page UC report says it leveraged two surveys from March and May 2020 to get a number of report’s metrics.Employment Figures and Growth of the Crypto Industry

The UC report first delves into the crypto asset ecosystem’s employment figures and notes that even though the industry provides opportunity, there’s been a decline since 2017.

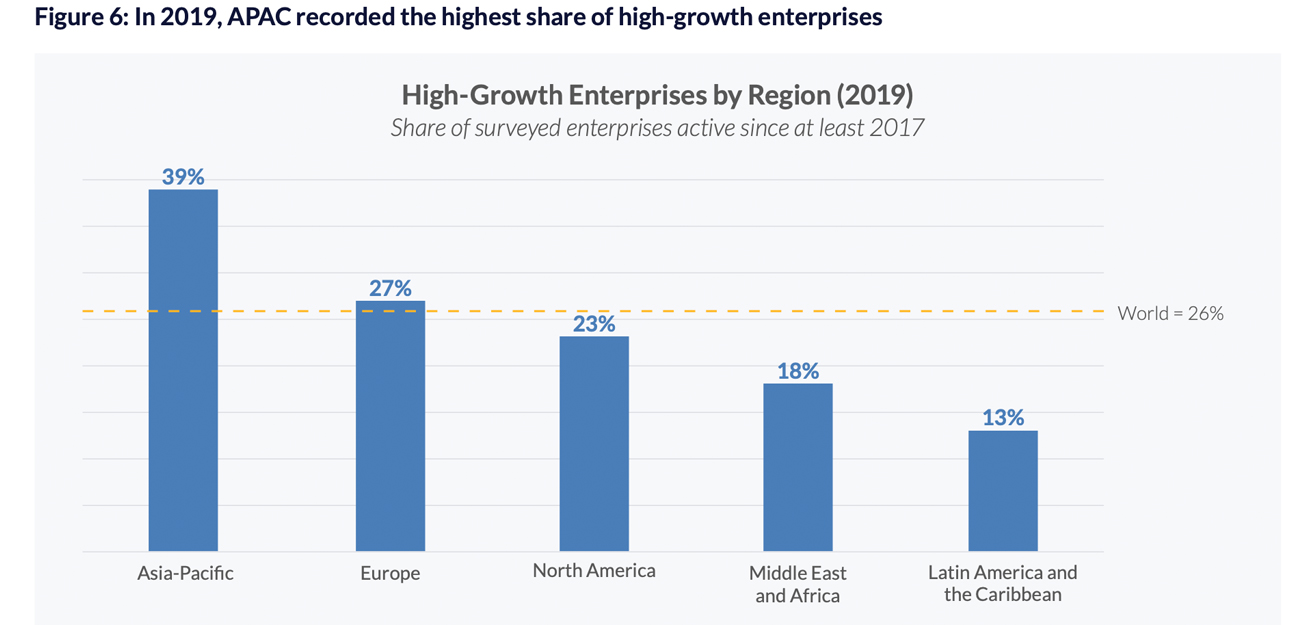

“Respondents across all market segments, reported year-on-year growth of 21% in 2019, down from 57% in 2018,” the UC authors detail.Furthermore, the mining sector was hit the hardest as it’s aggregated employment level saw a 37 point decline. Asia-Pacific (APAC) respondents recorded the highest share of high-growth enterprises in 2019 according to the data.

High growth is primarily younger firms that are 3-4 years old, and this represents 49% of the share of respondents. A few service providers polled detailed they saw an increase in profits in 2019 compared to years prior.

“Industry-wide, the growth in FTE employment declined by 36 percentage points between 2017 and 2019, whereas the median firm reported a 75-percentage point downward change in employment growth,” the UC benchmarking study notes.Hashers and Global Mining Operations

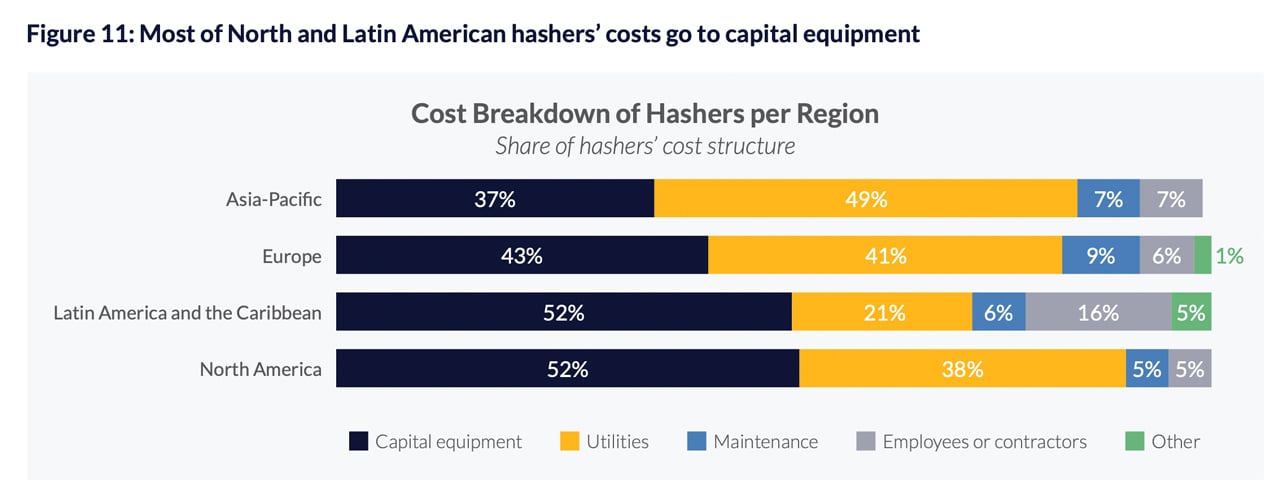

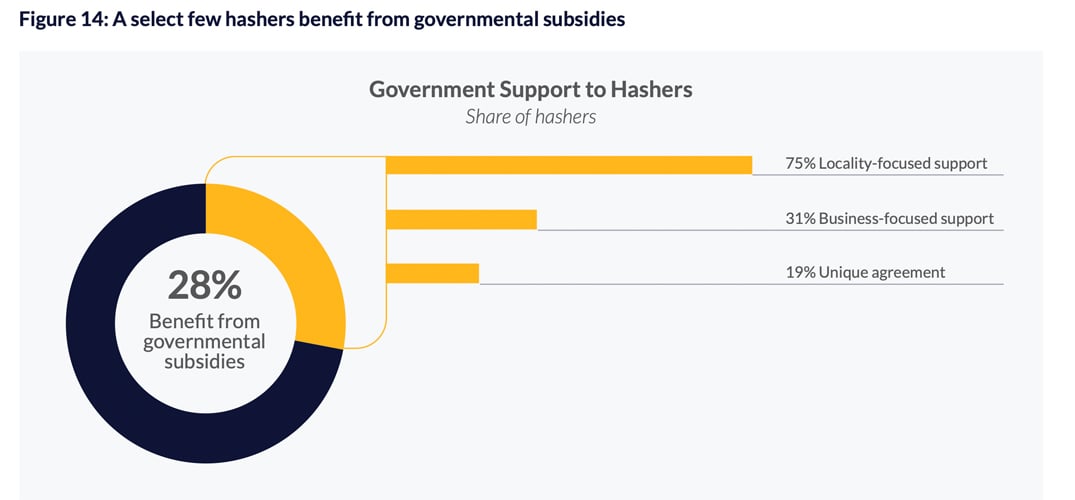

The UC study then discusses the cryptocurrency mining ecosystem and the report highlights that mining is steadily reaching an “industrial scale.” The findings detail the criteria miners (hashers) leverage in order to choose which coin the operation should mine is entirely based on profit scaling.

The utility cost for the average miner is roughly 79% of the aggregate operational expenditures.

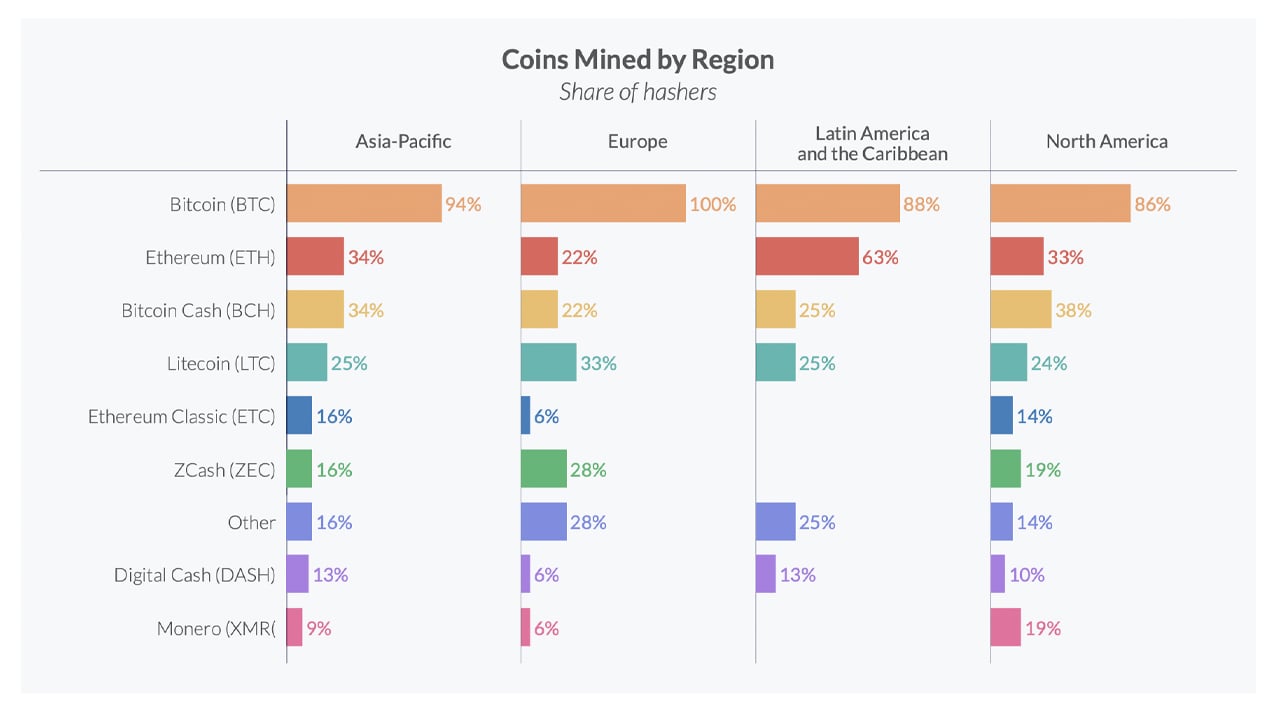

The benchmark report notes that bitcoin (BTC) is the most popular coin with 89% of respondents mining the crypto asset. BTC is followed by ethereum (ETH – 35%) and bitcoin cash (BCH – 30%) respectively. Certain regions have different miner popularity ratings depending on the region and demographic.

“For instance, ethereum mining appears to be particularly popular among Latin American hashers, whereas bitcoin cash is more popular in APAC and North America,” the authors detail.

“The mining of privacy coins in Western regions also differs from the global average: 28% and 19% of European and North American hashers report mining zcash, and as many North American hashers also engaged in monero mining.”

Crypto Mining Operational Expenditures and Renewable Energy

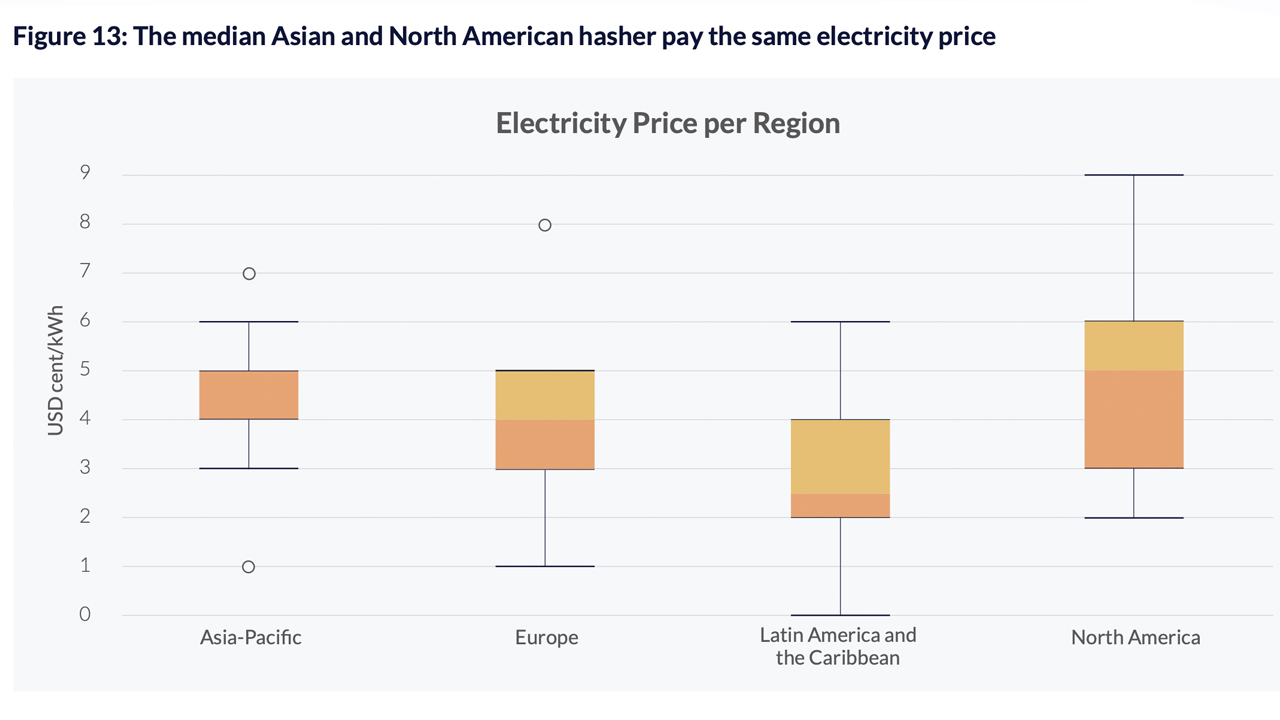

Moreover, the UC findings show that the utility cost for the average miner is roughly 79% of the aggregate operational expenditures. But there are differences that arise at the regional level, the study’s authors note.

“For instance, since the introduction of new tariffs on Chinese imports, US hashers have to pay 28% tariffs on ASICs shipped to the USA,” the report says.

While discussing electricity costs one takeaway from the study suggests the median Asian and North American miner pays roughly the same amount for electricity.

The mining section also examines Proof-of-Work’s (PoW) energy consumption, in general, and the subsidies or tax exemptions stemming from governments. Government benefits have entered the fray, but only “28% of the surveyed hashers report receiving support from governments.”

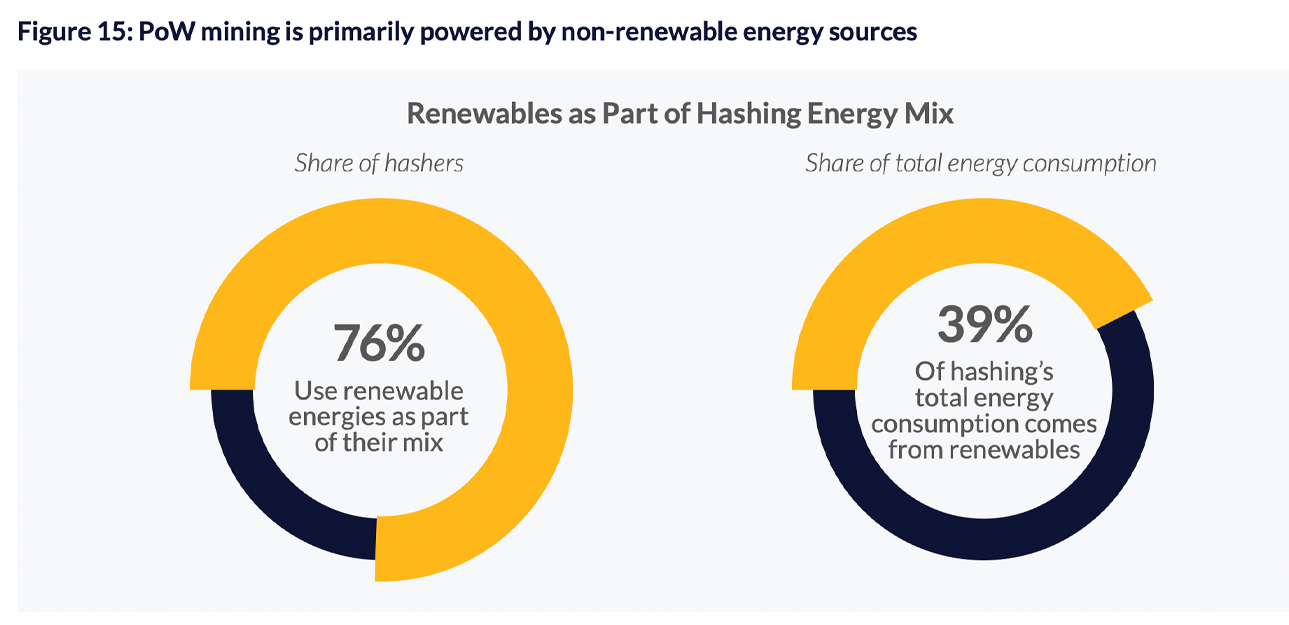

Additionally, the renewable energy estimate is much lower than prior reports concerning renewable energy and bitcoin mining. “39% of miners’ total energy consumption comes from renewables,” the UC study highlights. However, 76% of the survey respondents leverage a “mix” of traditional fuels like coal and renewables like hydropower.

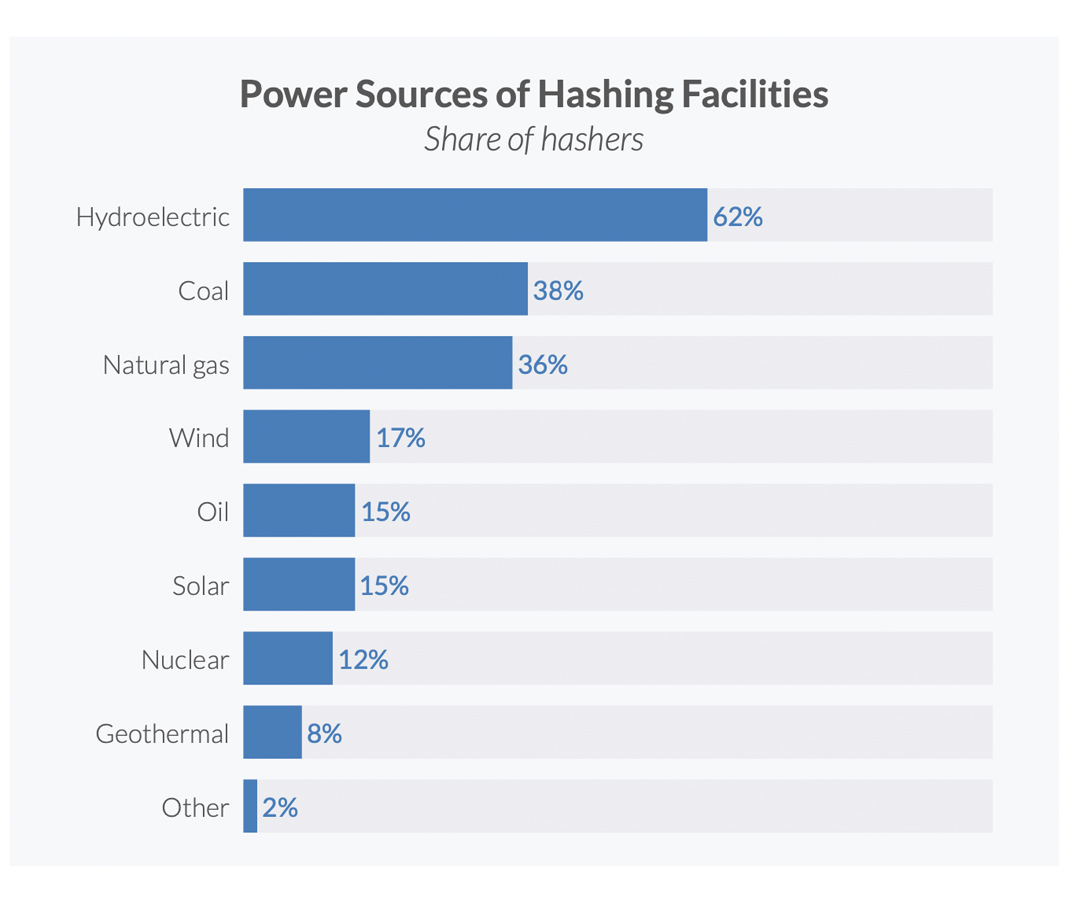

“Hydropower is listed as the number one source of energy, with 62% of surveyed hashers indicating that their mining operations are powered by hydroelectric energy,” the UC study details.

“Other types of clean energies (e.g. wind and solar) rank further down, behind coal and natural gas, which respectively account for 38% and 36% of respondents’ power sources.”

The Digital Asset Landscape and Crypto User Profiling

As far as the growing crypto asset landscape is concerned, bitcoin (BTC) is still the most popular cryptocurrency by representation on custodial services, payment processors, exchanges, and wallet providers. “Support has declined slightly over time from 98% of service providers in 2017 to 90% in 2020,” the UC authors mention.

Ethereum (ETH) is the second most commonly leveraged coin and the crypto asset is widely supported, while LTC, BCH, and XRP are available on at least 50% of 2020’s crypto service providers.Moreover, despite the negative news and delistings, “zcash and monero are still becoming increasingly more available, and are supported at 24% and 17% of service providers respectively

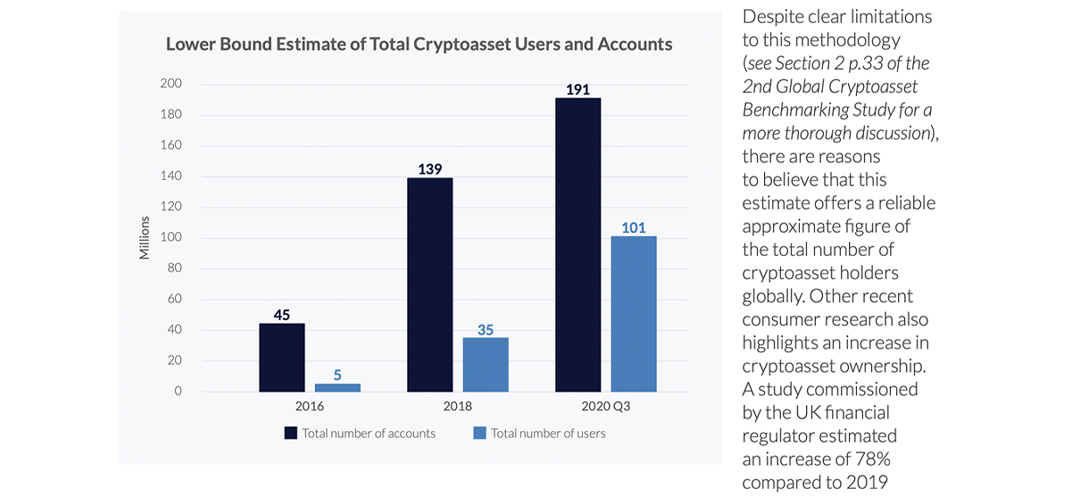

” Since the second UC benchmark report, identity-verified crypto asset users have increased significantly.The UC crypto study states:In 2018, the 2nd Global Cryptoasset Benchmarking Study estimated the number of identity-verified crypto asset users at about 35 million globally. Applying the same methodology, an update of this estimate indicates a total of up to 101 million unique crypto asset users across 191 million accounts opened at service providers in Q3 2020. This 189% increase in users may be explained by both a rise in the number of accounts (which increased by 37%), as well as a greater share of accounts being systematically linked to an individual’s identity, allowing us to increase our estimate of minimum user numbers associated with accounts on each service provider.

A Variety of Other Key Crypto Factoids

The vast amount of findings within UC’s study discusses a number of other subjects like stablecoins, IT security, and government regulations. Stablecoins like tether (USDT) have become very prominent and “increasingly available” the report highlights.

“Tether support [grew] from 4% to 32% of service providers and all non-Tether stablecoins [grew] from 11% to 55%. This increase is not simply from service providers holding stablecoins diversifying their holdings, but rather more service providers offering stablecoins,” the study insists.

The report also says, at the same time crypto asset companies are complying with new regulations, the “decoupling of duties, such as between custody, clearing and settlement responsibilities, appears to be underway” as well.

UC’s authors say the number of crypto companies that didn’t adopt know-your-customer rules (KYC), dropped from 48% to 13% during the last two years. This metric highlights that regulatory guidelines and compliance is on the rise. The UC study insists that the standards enforced by the Financial Action Task Force (FATF) invoked this significant change

Despite the increase of KYC/AML procedures, UC’s third benchmark study underscores the recent emergence of decentralized finance (defi) platforms.

UC’s authors Apolline Blandin, Gina Pieters, Yue Wu, Thomas Eisermann, Anton Dek, Sean Taylor, and Damaris Njoki emphasize defi has introduced “more risky and experimental innovations.” In the near future, it is possible that crypto service providers will be impacted considerably by the defi space, the study notes.

Defi will likely impact large crypto service providers in particular and their business models “in the next 12 months.

”The third “Global Cryptocurrency Benchmarking Study” in its entirety can be viewed here.-

Admin

- 0 comments

- 1 like

- Like

- Share

-

-

Way back in 2014, I debated the merits of bitcoin with cryptocurrency evangelist Andreas Antonopoulos. It was a wonderful, civil and not too disobedient dialogue. I was sceptical, not cynical.

Way back in 2014, I debated the merits of bitcoin with cryptocurrency evangelist Andreas Antonopoulos. It was a wonderful, civil and not too disobedient dialogue. I was sceptical, not cynical.

Six years later, I remain sceptical but now have a cynical bias.Let me explain what I see as the good, the bad and the ugly across the cryptocurrency landscape. I won’t cover the blockchain (for that, I have only optimism).

Cryptocurrency: the good- A democratised currency can only be described as good.

- A decentralised currency that cannot be controlled by any — misanthropic, missing or maddening — government leader must be described as good.

- A digital currency that does not recognise sovereign borders and so requires no conversion taxation or limitations is good.

- A currency for places that do not have a stable or developed one is very beneficial.

- Hooray for a currency that is ready, maybe too willing, and able for our global, digital world without all range of account establishment hurdles, capital movement restrictions and other challenges.

If you believe the rule of three, then those five points ought to be more than enough to wipe out the scepticism and initiate our living the crypto dream.Cryptocurrency: the bad

What if the world fully embraced a cryptocurrency? No more paper money. The social contract that we fear is fraying today would be torn to shreds.Without delving into what led to our social contract challenges, how would ‘universal sovereign individuals’, based upon their money, be taxed to enable and support a social contract with their schools, police, fire stations and safety nets?

Answer: they could not, I cannot imagine, without creating a violation — breaking the sovereignty — that would tear down the crypto kingdom as it stands. Moreover, governments with social contracts know this and will do whatever it takes to stop any real breakaway from their currencies.

Now, re-visiting the five ‘goods’, because hope and hype is not a strategy, we can lose the first one because a democratised cryptocurrency is kind of fictional.

Why? Because today, big controlling hands exert an influence on the cryptocurrencies that exist through mining or any other process.

Cryptocurrencies have not been distributed like some type of universal basic income (UBI). To be sure, introducing a form of cryptocurrency could make for a brilliant UBI, but it would be guaranteed to be controlled by a central, sovereign state actor – so much for that idea.

And, for all those who think crypto is fabulously anonymous, it is not. Hello blockchain – the real dream tech!

There is a reason that governments have threatened or begun to remove from circulation larger denominations of paper currencies. Hint: cash is much more anonymous.Cryptocurrency: the ugly

All paper currencies can be lost or stolen. Ugh! But crypto is not demonstrably more secure. There are big thefts and hacks and people lose their crypto keys all the time (ugh again!).And, don’t forget the infamous American bank robber Willie Sutton.

When asked why he chose banks, Willie allegedly responded “because that’s where the money is”. Well, crypto exchanges are arguably bigger and easier targets than any individual bank today. And exchanges don’t offer complimentary insurance.As if that isn’t ugly enough, try to stomach these:- Cryptocurrencies can be manipulated or schismed – such as the schism in bitcoin’s most notable spin-off, bitcoin cash, in 2018.

- How would you feel about paying the equivalent of several thousand dollars for a pizza? If a cryptocurrency cannot remain stable, why would buyers/sellers be motivated to use it? Aside from potential illicit applications and maybe for collectibles, there is no use, no purpose. Unless…

- You view your cryptocurrency as an investment. Maybe just don’t. Investments offer dividends or a yield. Cryptocurrencies have neither. They are… speculations, collectibles? Does the world really need any more private ornaments? And digital gold? Really? That’s nice marketing. But why not just buy gold?

Be careful if you’re crypto dreaming

The sceptical me remains sceptical and not crypto dreaming. You may wish to be careful, too.Furthermore, the idea of sovereign digital currencies – the stuff of efficiency/effectiveness dreams – could be dangerous, too. Take a moment and think of the temptation to tax, repress, fine or devalue with the proverbial press of a button if there’s any form of centralised control.

Fiat currencies – that is, government issued money – are no panacea, but for me still, today, I’ll take paper or plastic/credit, please, at least until decentralised digital is a reality.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.For more research and analysis, visit CFA Institute.

By Michael S. Falk, CFA, partner at the Focus Consulting Group.All posts are the opinion of the author.

As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.-

Francisco Gimeno - BC Analyst Interesting approach to crypto currency. Not everything that glitters is gold, even in crypto. There are many reasons why, even trusting that a new digital economy fuelled by 4th IR techs is coming, we can say crypto is yet in an infant stage, and many things have to change, develop or being solved before we can accept and use crypto currency all around. Time will say.

-

The proliferation of digital currencies over the last few years has led to a rapidly growing list of use cases for tokenised assets.

The proliferation of digital currencies over the last few years has led to a rapidly growing list of use cases for tokenised assets.

Thanks in no small part to the development of blockchain technology, as well as the recognition and anticipation of what cryptocurrencies such as bitcoin and ethereum (ether) could achieve in the future, tokenised assets are hotly anticipated to deliver a variety of benefits to the world—from boosting specific industries such as banking and real estate to helping to solve global challenges such as supply-chain issues and financial inclusion.

Indeed, we are already seeing hundreds of projects issuing digital tokens with the intention of growing both user adoption and utilisation of the tokens as well as promoting the use of particular blockchain platforms.

But given that these tokens now represent an increasing array of useful assets and functions, each one is exposed to numerous economic forces, including supply and demand, changes in the prices of competitor currencies, and inflation.

And because each has an economic value that can change in response to such factors, it becomes crucially important to understand each token’s inherent utility.

This ensures that both token users and investors are confident that they are buying an asset that is valued accurately.

And it is also important for them to ensure that a token will be employed more extensively going forward, which in turn will mean that more people will demand to use the token, and thus its value should appreciate.

So, what is a token’s utility? This question has led to the early development of new economic models that aim to account for the forces that determine the value of digital tokens. As such, token economics seeks to analyse the various economic factors and mechanisms that are involved in the value-creation process of a tokenised ecosystem.

It refers to how economic forces lead to the creation of sustained user adoption of both the token and the ecosystem as a whole, and it is thus ultimately used to determine whether tokenised assets can be useful in the real world over the long term, beyond merely functioning as a digital currency.

The methods through which cryptocurrencies are created and issued into circulation play a significant role. Whilst some are issued in a one-off manner, others are circulated more gradually. This has significant implications for the relative scarcity of the token at any point in time, which in turn influences how much each token is worth.

Similar in manner to how real-world commodities such as gold derive much of their value from their relative scarcity and utility, the scarcity and utility of digital tokens such as ether also go a long way towards determining their value.

Token economics also deals with how robust blockchain systems can be designed to produce desirable outcomes for all network stakeholders, including token users and those responsible for validating transactions. With that in mind, one of the most important forces for which to account when designing such models is incentivisation.

With blockchains invariably involving a decentralised architecture, there is no need for relevant parties within the ecosystem to trust or rely on an intermediary entity to maintain the integrity of the ledger of transactions (as is generally the case with centralised applications such as Facebook or Google).

Instead, blockchain enables all validating nodes to maintain their own copies of the same ledger, which in turn greatly enhances the security of the data. But to ensure long-term sustainability, relevant stakeholders must be adequately incentivised to act in the best interests of the system as a whole.

If this is achieved, it should instil confidence in the integrity of the system and thus facilitate greater user adoption of the system’s token.

Bitcoin, for instance, involves senders and recipients of the cryptocurrency, as well as miners who are responsible for validating transactions and adding the next block of transactions to the blockchain.

This is done using cryptography, which provides irrefutable proof of all previous transactions within the system. Incentives are thus designed to ensure that the system continues to produce desirable outcomes.

The miner receives bitcoins as a reward for validating transactions in accordance with the network rules. If, however, miners break the rules in one way or another, they can be penalised, typically through a loss of their tokens.

This system incentivises miners not to behave nefariously and, as such, ensures individuals are acting to benefit the security of the system rather than for self-interest.

The world’s second-most valuable cryptocurrency project, ethereum, meanwhile, is designed principally to execute smart contracts that are employed for a variety of use cases, such as creating decentralised autonomous organisations (DAOs) and decentralised applications (DApps).

The smart contract code is stored on ethereum’s blockchain. And while it is similar to bitcoin, in that miners validate new blocks and are rewarded with ether, the ethereum ecosystem also requires users to pay ethers if they want to execute smart contracts on the platform.

Similarly, the actual users of each ecosystem (such as the senders and recipients of coins in the case of bitcoin) must be suitably incentivised to ensure that their behaviour promotes the continued sustainability of the ecosystem.

This means that issues such as the sustained growth in both the overall numbers of users adopting the token and the number of users actually using the token for its intended purpose are taken into account. As far as the latter is concerned, this is proving to be far from straightforward.

Given the massive price swings that much of the cryptocurrency space experienced until 2018, the myriad of opportunities to benefit from short-term price appreciations has caused most users to date to hold their tokens as an investment that could generate potential substantial returns rather than actually use the tokens.

Even today, many investors continue to hold on to their tokens in the hope of seeing bitcoin scale the heights it managed to achieve in late 2017.

Simply buying and holding is far from ideal from the perspective of the token issuer, especially given that such tokens have been created mainly to be used for a specific purpose within the ecosystem.

Indeed, it is unlikely that violent price swings will even be considered desirable by token issuers, especially if those price swings are not reflective of the endogenous value of the token itself but instead of the trading activities conducted by investors looking to exploit opportunities for profit.

Nor will a static price over the long term incentivise users to hold on to their tokens. As the ecosystem grows and more users begin to adopt the token, one would reasonably assume that the increase in utility associated with this growth will induce a steady rise in the price of each token, which in turn will deliver at least respectable returns for token holders.

The economics associated with designing such an ecosystem, therefore, is likely to prove challenging for token-project designers, especially for those projects for which the inherent value of each digital asset is not easy to calculate.

Some models have been posited to address some of these challenges. For instance, Factom, a system for securing millions of real-time records using blockchain, has tried to implement a “burn-and-mint” process, whereby users burn” their Factom (Factoid) tokens each month in order to use the Factom ecosystem, while the issuers separately mint 73,000 new tokens each month that are distributed to transaction validators.

Should users end up burning less than this figure per month, therefore, Factom’s overall token supply in circulation increases, which should exert downward pressure on the Factoid price. But the total supply will fall if users end up burning more than the 73,000 tokens, which in turn should boost prices.

As the usage of the Factom ecosystem grows over time, therefore, more tokens should hypothetically be burnt, which would help to progressively raise prices in direct proportion to network usage. But the burn mechanism should also incentivise token holders to actually use their tokens rather than simply hold them.

There may also be other issues that will have to be considered when ascertaining the token economics required for designing a suitably robust model, including the governance system, the mechanisms for revenue sharing and the ease of access for users.

Ultimately, with each protocol likely to be different and dependent on the specific utility of the token, the approach to token valuation will also be different for each project.

As such, designing the appropriate mechanisms and incentives to ensure that participant behaviours are always as desired will not be a standard process.

And that makes token economics a challenging field for project designers to navigate during these early years of blockchain’s evolution.-

Francisco Gimeno - BC Analyst Token economics is a new field for designers and those who wish to understand better the concept of tokenisation and its consequences. Make sure you are one of those who get to understand it by reading, debating and participating.

-

-

Research: 80% of US and European Institutional Investors Find Cryptocurrency App... (news.bitcoin.com)A new survey of about 800 institutional investors in the U.S. and Europe shows strong cryptocurrency adoption, particularly bitcoin. About 80% of institutions said they find cryptocurrency appealing, and 60% believe cryptocurrencies have a place in their portfolios.

Research: 80% of US and European Institutional Investors Find Cryptocurrency App... (news.bitcoin.com)A new survey of about 800 institutional investors in the U.S. and Europe shows strong cryptocurrency adoption, particularly bitcoin. About 80% of institutions said they find cryptocurrency appealing, and 60% believe cryptocurrencies have a place in their portfolios.Crypto Appeals to 80% of Institutions Surveyed

Fidelity Digital Assets, the cryptocurrency arm of Fidelity Investments, announced Tuesday the results of a survey to better understand institutional interest and adoption of cryptocurrencies as well as key barriers to investing in them. It was conducted from November 2019 to March 2020.

Fidelity Digital Assets offers a full-service, enterprise-grade platform for securing, trading and supporting cryptocurrencies.A total of 774 institutional investors participated in the survey, 393 of which were in the U.S. while 381 were in Europe.

Respondents include financial advisors, family offices, pensions, crypto and traditional hedge funds, high net worth investors, endowments, and foundations. This is the second consecutive year Fidelity has surveyed U.S. institutions but it is the first time it surveyed European investors. According to the results:Almost 80% of institutional investors find something appealing about digital assets.

Fidelity Digital Assets conducted a survey of 774 U.S. and European institutional investors and found that about 80% of them find cryptocurrency appealing in some way.

Breaking down the number, 74% of U.S. institutional investors find cryptocurrency appealing, while 82% of European investors do.

“A notable contrast is that 25% of European investors find the fact that certain digital assets are free from government intervention to be appealing, whereas only 10% of investors in the U.S. feel this way,” the report further reads.

Moreover, 36% of respondents — 27% in the U.S. and 45% in Europe — revealed that they are currently invested in digital assets. Bitcoin continues to be the cryptocurrency of choice with over a quarter of respondents holding BTC while 11% have exposure to ETH.

“Looking out five years, 91% of respondents who are open to exposure to digital assets in a portfolio expect to have at least 0.5% of their portfolio allocated to digital assets,” the report adds.

Three characteristics of cryptocurrencies are most compelling to both U.S. and European institutional investors. 36% of respondents said “uncorrelated to other asset classes,” 34% are compelled by innovative technology, and 33% by the high upside potential. The report notes:The majority of institutional investors (6 in 10) feel digital assets have a place in their portfolio, though opinions vary on precisely where.

Despite growing interest among institutions, obstacles remain to cryptocurrency adoption. 53% of respondents cited price volatility as the main reason, 47% said market manipulation, and 45% said “lack of fundamentals to gauge appropriate value.

”Fidelity Digital Assets president Tom Jessop commented on the survey findings:

“These results confirm a trend we are seeing in the market towards greater interest in and acceptance of digital assets as a new investable asset class.

This is evident in the evolving composition of our client pipeline, which spans from crypto native funds to pensions.”What do you think about institutional interest in cryptocurrency? Let us know in the comments section below.-

Francisco Gimeno - BC Analyst Very interesting that, even with high volatility and a small market size, the crypto and token ecosystem is becoming with time very much valued by investment institutions, as a new asset class, and this interest is growing every month. Much work is needed yet to make this market also accesible through tokenisation, Apps and other tools to the general world. Meanwhile, another sign that times are changing in the financial and investment industry.

-

-

5G networks are beginning to roll out across the UK as well as around the world. One of the biggest promises of 5G is the ability to connect millions of IoT devices. And Blockchain networks have three services they can perform to drive adoption and add value.

5G networks are beginning to roll out across the UK as well as around the world. One of the biggest promises of 5G is the ability to connect millions of IoT devices. And Blockchain networks have three services they can perform to drive adoption and add value.

IoT stands for the Internet of Things. More simply, IoT is a network of things/devices connected to the Internet. These devices include sensors to collect data, and other functions, allowing them to engage with the world around them.

Some examples of IoT devices would be a temperature sensor with a 5G radio built-in or an automated door lock in a hotel room connected via WiFi.

Together all of these devices make up the Internet of Things or IoTWith potentially millions of IoT devices coming online soon, there will be substantial demand for network bandwidth, hence the importance of 5G networks. But what does blockchain have to do with any of this?

Blockchain networks will play a vital role in three main areas: value Transfer, Identity and Data Collection.

As early as 2012 there have been IoT devices connected to the bitcoin blockchain. Specifically, there was an internet-connected vending machine which accepted bitcoin as payment. The first purchase was for a bag of popcorn.

The system was simple enough. When the right amount of bitcoin arrived in a specified wallet, the vending machine would spring into action. Of course, there were some problems along the way.

The bitcoin network can take up to an hour to process a transaction. With some tweaking, it can be nearly instantaneous. The problem with this is that it removes some of the safety mechanisms to reduce fraud. For substantial transactions on the bitcoin network (like purchasing a house) it is best to wait for up to an hour to ensure that the network accepts the transaction.Today’s IoT systems need immediacy and may rely on blockchain protocols with significantly faster performance than available today.

Today’s IoT systems need immediacy and thus may rely on blockchain protocols and networks with significantly faster performance and assurance against fraud.

Equally, today’s IoT systems will not rely on the transfer of cryptocurrency direction to a device. Instead, payments will be made using traditional fiat currencies across existing payment systems – and then receive blockchain-based notifications.

For any of these systems to function, including peer-to-peer communication, there must be a decentralised identity framework. Every device is registered and identifiable across the network. Blockchain can provide this identity framework.

When implemented at an industry level, it allows for the identification of any IoT device, regardless of manufacturer, geographical location or purpose, to any other device.

An IoT Identity network can verify transactions as originating from authorised devices. Equally, the systems can ensure the sending of access transactions to the correct destination device.An IoT Identity Blockchain is a hugely ambitious project…

An IoT Identity Blockchain is a hugely ambitious project, but one which has sufficient advantages to all stakeholders to put aside competitive objections and get on with the creation of the governance, protocols and systems of such a network.

Last week Vodafone and Energy Web announced a partnership that could provide identities for billions energy generating assets.The last piece in the puzzle is the ability to automate the entire network. Enter smart contracts.

Smart contracts are programs which run on the network and orchestrate the automated communications between devices and the associated transfers of value. Smart contracts do not run only in isolation; they need input from the outside world.

A smart contract needs to created, executed, to check conditions from the outside world and to cause actions in the outside world.Connections between the outside world and smart contracts are known as oracles and oracle services (not to be confused with Oracle Corporation).

Every IoT device or group of IoT devices can act as an oracle. Smart contracts can check with an oracle service to determine the temperature outside or the arrival time of a cross-country train.

An oracle service can unlock the door to a properly rented Airbnb flat – or serve a bag of popcorn from a vending machine.

And all of these transactions, automated or not, can be recorded in a blockchain. By registering every transaction, transfer and transformation, a permanent, immutable record exists for independent verification and audit. And with appropriate access, there will live a vast amount of data.

Blockchain-based data records can prove useful for analysis but also for training machine learning and artificial intelligence models. Of course, these are not without their challenges.

Blockchain is not designed for storing vast amounts of data – whether in the number of transactions or data associated with single transactions. Equally, data stored on a blockchain must be masked in some way so as not to reveal personal, sensitive or competitively sensitive data inadvertently.

Masking or hiding data by maintaining a centralised database with appropriate access controls addresses this issue.Blockchain, IoT and 5G will provide an infrastructure allowing for extensive new business models and process automation opportunities.

It will require thousands of companies to agree to work together, and it will require an evolution of blockchain and other distributed ledger technologies. And it will require a keen focus on managing privacy and access to data that works for everyone.

Get in touch with us [email protected] / Twitter

@igetblockchainTroy Norcross, Co-Founder Blockchain RookiesTwitter: @troy_norcross-

Francisco Gimeno - BC Analyst The time is now for the enmeshing of 4th IR techs, working together, not for speed, but for better integration and results, creating the foundation for the digital economy, All economy will get in the wagon at seeing the opportunities brought by this. IoT and blockchain were the first in the streets. But something was amiss. Now with 5G expansion starting soon, both techs, together with a more powerful and evolving AI, the world is going to change very fast.

-

-

Many enterprise IT teams feel there is no justifiable use case for blockchain. At the other end of the spectrum are those who believe in storing every last bit, byte and nibble of data on the blockchain. Neither of these is overly helpful in supporting the adoption of blockchain networks in industry.

Many enterprise IT teams feel there is no justifiable use case for blockchain. At the other end of the spectrum are those who believe in storing every last bit, byte and nibble of data on the blockchain. Neither of these is overly helpful in supporting the adoption of blockchain networks in industry.

A foundational premise of applying blockchain to solve business problems is Minimum Effective Blockchain (MEB).Perfection is achieved, not when there is nothing more to add, but when there is nothing left to take away.– Antoine de Saint-Exupéry

Tim Ferriss, in his book The 4-Hour Body, refers to the principle of Minimum Effective Dose (MED). The definition is straightforward: The MED is the smallest dose that will produce the desired outcome. Of course, in Tim’s context, it was related to sports nutrition and supplements. This principle can also apply in the context of blockchain.Minimum Effective Blockchain (MEB) is the smallest combination of data and nodes to create value for the broadest range of stakeholders.

Minimum Effective Blockchain (MEB) is the smallest combination of data and nodes to create value for the broadest range of stakeholders. Good data architecture design is critical. Blockchain networks are not designed for storing large amounts of data.

Neither are they intended for storing high volumes of transactions. Blockchain networks do not perform as efficiently as relational databases.

The data stored in the blockchain should be the minimum set of information necessary to ensure trust between counterparties and satisfy the requirements around tracking and tracing assets.And what of the rest of the data?

A blockchain project will often require more data than that which is on the blockchain. The additional data may exist in a distributed database or filesystem. These data stores can be designed to prevent unauthorised access using encryption and other established technologies.

In these cases, the information stored on the blockchain can contain time-stamped records of the original data. Any tampering with the data becomes immediately evident.

The blockchain can also store records of access to data and granting/revoking access to information. Inevitably, the distributed data will have a central point of control. However, so long as the underlying blockchain is decentralised, counterparties can be confident that the data integrity is maintained.What is the minimum number of nodes necessary to ensure the integrity of the network?

With the data architecture planned, what is the minimum network architecture required? Or, to put it another way, what is the minimum number of nodes necessary to ensure the integrity of the network? (A node in a blockchain network is a computer which contains a copy of the blockchain and participates in the process of adding new data to the blockchain) A vital aspect of the Bitcoin network’s security is a large number of nodes.

As a public permissionless blockchain, the Bitcoin network has an estimated 10,000 nodes. To compromise the network, an attacker must take control of more than half (the 51% attack problem).

In enterprise blockchain projects, there are a range of additional factors to consider.The minimum number of nodes necessary for network integrity varies based on how the network achieves consensus related to adding data to the blockchain. The Bitcoin protocol uses something called Proof of Work. A large number of nodes is critical for this protocol.

Other protocols like Hyperledger Fabric, use a different consensus mechanism and can operate with only a few nodes. A further consideration for enterprise or industry blockchains is private versus public. If a blockchain network is private, then all members are known to each other.

The closed nature of the network affords a trust which arises from every member knowing every other. Any node that attempts to behave like a bad actor is caught out and potentially thrown off the network. Operating and maintaining a blockchain node is one of the costs of the network. It is not likely that every member will want to run their node.

Many smaller stakeholders will have neither the competence nor the desire to run their nodes. The decisions of who will run the nodes – and how the cost will be absorbed – is part of the design.In applying the MEB principle to enterprise blockchain projects, determine the minimum number of nodes necessary for the network to be fully trusted and to operate securely.As with many things, the MEB approach – if taken to an extreme – can go too far.

As with many things, the MEB approach – if taken to an extreme – can go too far. In the case of blockchain it is possible to reduce the number of nodes and data to such a small amount that it is no longer blockchain – but only a DLT (Distributed Ledger Technology approach) – or possibly not even DLT.

If stripped back far enough, the solution has value only to one stakeholder. And for that, you can use a database.

Today’s primary objections to the use of blockchain technology focus on issues of scalability, performance and transparency. These objections are genuine and can happen with flawed blockchain design from the start.

When looking at how to solve a multi-enterprise industry problem with blockchain technology, begin by deciding the minimum amount of information which must exist on a blockchain network that is distributed and decentralised where data is immutable.

Then look at what data should reside in a decentralised filesystem or database with traditional technology solutions for scalability, performance and access control. Not everything belongs on the blockchain. Not every stakeholder should run a node.

Blockchain cannot solve every problem. To avoid problems in the future, apply the principle of Minimum Effective Blockchain (MEB) to the design in the beginning.

Get in touch with us [email protected]

/ Twitter @igetblockchain-

Francisco Gimeno - BC Analyst Reality check: the blockchain shouldn't be applied to everything every time and, the blockchain is not a solution but a tool. It must be used when its proven the better solution, and should be used as a support for other solutions when other solutions are better. The principle of Minimum Effective Blockchain (MEB) stated here is interesting.

-

-

GBBC Open Source Ideas:

The Future of Urban Living

Part I:

The Rise of “Smart Cities”

17 March 2020

Washington DC,

United States

IntroductionUrban populations around the world are growing, putting new and unexpected strains on urban environments and governments. The United Nations estimates that 55 percent of the world’s population lives in urban areas; this is projected to increase to 68 percent by 2050, adding about 2.5 billion people to urban areas.

i.

In the face of this growth and pressing issues surrounding transportation, water management, energy, waste management, government service delivery, and much more, some cities are turning to technology with the goal of becoming “smart cities.” According to McKinsey, the smart city industry will be a $400 billion market in 2020.

ii.

If you ask people to define a “smart city,” you will likely receive a range of answers: from “I don’t know” to “cities where streets expand and contract based on traffic patterns,” or “cities where noise and light pollution iseliminated to improve the psychological wellbeing of inhabitants.” While there is no set definition of a “smart city,” this term generally refers to urban environments in which technologies, especially Internet of Things (IoT) and broadband, are used to improve the lives of citizens.

While splashier and more visible smart city innovations, such as applications that identify and alert users to open parking spaces, receive the bulk of media attention, there are many other “background ” innovations that can lead to significant quality of life improvements for citizens; this is where blockchain technology fits in. It should be noted that blockchain and IoT are an effective and popular technology pairing.

A recent Gartner survey found that 75 percent of IoT adopters “in the U.S. have already adopted blockchain or are planning to adopt it by the end of 2020. Among the blockchain adopters, 86 percent are implementing the two technologies together in various projects.”

iii.

Blockchain technology is distributed, transparent, and highly secure, three traits that can prove invaluable for certain smart city innovations. With blockchain’s massive potential in this area in mind, the Global Blockchain Business Council (GBBC) and respective collaborators conducted a survey of individuals in New York City, Los Angeles, Nur-Sultan (formerly Astana), and the United Kingdom regarding opportunities and roadblocks for blockchain implementation.

For this survey, questions were written by the GBBC team with the aim of understanding how individuals in the blockchain space view the implementation of blockchain technology for smart cities.

To disseminate the survey, the GBBC partnered with trusted local groups and institutions focused on blockchain technology in each of the target cities. Partner organizations, including NYC Blockchain Center, Los Angeles Blockchain Lab, Citigate Dewe Rogerson, and Astana International Financial Centre (AIFC), then agreed to share the survey with their respective....

Download the full report here: https://gbbcouncil.org/wp-content/uploads/2020/03/Future-of-Urban-Living_Part-I_Smart-Cities-.pdfhttps://gbbcouncil.org/wp-content/uploads/2020/03/Future-of-Urban-Living_Part-I_Smart-Cities-.pdfth their respective....

Download the full report here:

https://gbbcouncil.org/wp-content/uploads/2020/03/Future-of-Urban-Living_Part-I_Smart-Cities-.pdf

-

Francisco Gimeno - BC Analyst There is a lot of literature on the issue of "smart cities", related with 4th IR techs like the blockchain. The world after this pandemic offers us also new reflections on how we want these smart cities to develop. We need smart cities to help developing new attitudes, new approaches and ways of living in a healthy, smarter urban society. Good reading.

-

-

A few years ago, if you had heard that the U.S. government might mint its own digital currency, you might have dismissed the idea as starry-eyed futurism — or, less charitably, a joke.

A few years ago, if you had heard that the U.S. government might mint its own digital currency, you might have dismissed the idea as starry-eyed futurism — or, less charitably, a joke.

Digital currencies, such as Bitcoin, were the purview of speculators and coders, not stodgy central bankers.

But this winter, the Federal Reserve announced that it’s investigating the possibility of issuing its own digital coin.

Speaking at Stanford, Federal Reserve Governor Lael Brainard noted that the “potential for digitalization to deliver greater value and convenience at lower cost” has piqued the interest of the traditionally risk-averse institution.

For now, the Fed’s interest in digital currency might be most notable as a sign of how the world has changed — and where the winds are blowing.

Because just as Paypal and eBay (or Alipay and Taobao, if you prefer) revolutionized how people shopped online and Amazon changed how people shop, full stop, digital payment services — powered by blockchain technology — could be the next great upheaval in global e-commerce growth.

For that to come to pass, however, four conditions need to align: appropriate technology, consumer demand, corporate champions, and an amenable regulatory environment. The question is how.

For all the hype around blockchain — the open-source digital ledgers that many have argued will do everything from make cash obsolete to remake the global economy — it can sometimes seem like a solution looking for a problem.

While it has found a place in niches such as supply chains and digital IDs, problems like price volatility and the need to comply with the existing regulatory framework have prevented mainstream adoption in currency.

But now, one promising category of cryptocurrencies known as “stablecoins” seems poised to succeed where its predecessors failed.

Uniquely positioned to act as a medium of exchange in e-commerce, stablecoins enhance both the efficiency and reach of e-commerce.Finding the Right Application for Blockchain

As their name suggests, stablecoins distinguish themselves from their more popular but highly volatile cryptocurrecy brethren, such as Bitcoin, in their focus on price stability. In striving for stability from the start, stablecoins hope to avoid situations like the one experienced by Laszlo Hanyecz in 2010.

Hanyecz was a U.S.-based software programmer who agreed to pay someone 10,000 Bitcoin for two Domino’s pizzas (a fair price at a time when Bitcoin was worth only a fraction of a penny).

Today, this transaction would be worth almost $100 million. Hanyecz was proving a point — this was the first instance of a good being purchased with a cryptocurrency — but the now-legendary story has also become an allegory of the pitfalls of using a notoriously volatile tender for day-to-day purchases.

Stablecoins have adopted a variety of approaches to solve this price volatility problem.

The highest profile attempt so far — and the most controversial — has been Facebook’s new, yet-to-be-released cryptocurrency project, Libra, which was supposed to be tied to a basket of short-term government securities and bank deposits in historically stable currencies such as U.S. dollars and Euros.

Pushback from regulators and traditional financial institutions has induced Facebook to pull away from its original vision of a global currency that competed with monetary authorities.

Although there is still a lot of uncertainty surrounding the project, it might look more like Venmo, with people sending dollars through Facebook.Terra (where Nicholas works) is a new stablecoin that has been adopted by several online merchants across Southeast Asia.

It’s less well-known in the U.S., but it’s an example of how stablecoins actually work in the wild — a blockchain currency with reliable value that normal people actually use.

In contrast to Libra, it employs a form of automated monetary policy to keep its price stable, contracting the supply when prices are too low and expanding it when prices are too high.

This is achieved using a second cryptocurrency, Luna, which acts as a monetary policy instrument and earns transaction fees as a form of reward.

And while criticism of Libra has mainly been centered on how its governance mechanism is controlled by a few large corporations — the Switzerland-based Libra Association — Terra’s policy is coded directly on its blockchain and therefore is transparent and impervious to human interference.

The stability and transparency of Terra are important because they harness the potential of blockchain in a form that’s useful for everyday people. That, in turn, sets it up to challenge existing technologies. In the case of Terra, that means taking on credit cards.Better Than a Credit Card

Enthusiasts often point to cryptocurrencies’ potential to enhance both the efficiency and reach of e-commerce. The existing financial system — while certainly functional — has its share of inefficiencies, including its reliance on middle men, which often come in the form of credit card providers that charge up to 3% per transaction.

Blockchain technology allows payments to occur directly between buyers and sellers, circumventing the existing system and reducing costs for both merchants and consumers.

Blockchain also allows for the automation of the transaction verification process, where most banks today still expend significant resources on expensive manual verification. In fact, Santander InnoVentures has estimated that “blockchain technologies could reduce banks’ infrastructural costs by $15-20 billion a year by 2022.

” These advantages will bring faster settlement times and cheaper international transactions.

As shown by the Square’s staggering success in attracting small businesses with lower fees, stablecoins’ higher efficiency is likely to translate into wider reach.

Merchants, who build those fees into their prices, might be more willing to offer their products online because of the lower fees.

Similarly, customers might decide to keep balances in digital currencies and complete more transactions online without ever going back to fiat currency or feel the need for a credit card account.

For the 25% of U.S. households that the FDIC has identified as unbanked or underbanked, lower fees and lack of barriers to entry could be transformative. Finally, the general mistrust in financial intermediaries that leads millennials to flee traditional banks for fintechs and challenger banks suggests they’d be willing crypto adopters.

These features could prove to be the edge that drives stablecoins into the financial mainstream. To understand the effects that they might have on the e-commerce ecosystem, we can use data from Terra, which has experienced explosive growth since launching in June 2019, growing at 35% month-over-month.

It now has over 1 million users, who frequently use it for online purchases ranging from groceries to hotel bookings. Due to easy onboarding and lower fees, merchants have been the first to promote Terra over alternative payment options, e.g. credit cards, thereby facilitating its rapid adoption.

Terra’s growth has been driven by a significant reduction in the adoption of other payment systems, including credit cards. This suggests what E-commerce 2.0 might look like in the western world as well.

If stablecoins are going to become mainstream, however, they need corporate champions as well as innovative outsiders, and they’re starting to win influential insiders over.

Facebook’s debacle in launching Libra has been instrumental in bringing attention to this opportunity and has accelerated similar developments elsewhere.

Financial institutions, including JP Morgan, have recognized the need for a digital currency for payments. Jack Dorsey’s Square has recently won a patent for a network allowing consumers to pay with cryptocurrency and merchants to receive the full value in U.S. dollars, eliminating any concerns about crypto volatility.

Finally, the whole financial ecosystem is evolving —challenger banks such as Revolut accepting cryptocurrencies, for instance — which makes future developments and integration more likely.But Will People Use It?

There are still major barriers for blockchain currencies to overcome, no matter what incentives exist. For most of the world, the use of cryptocurrency to pay for goods and services is limited to certain niches.

There are some major retailers — including Starbucks and Overstock.com — that accept crypto, but they’re outliers.

A blockchain research company, Chainalysis, found that a mere 1.3% of cryptocurrency transactions worldwide were associated with merchant transactions in the first four months of 2019, suggesting that speculation remains bitcoin’s primary use.

Regulation could change that. Banks have been reluctant to get involved in cryptocurrency projects because of potential scrutiny from skeptical regulators, which in turn has made most businesses suspicious of the technology and slowed adoption.

Policymakers worry about transferring control of monetary policy from sovereigns to commercial enterprises. The ability of central banks to expand and contract the money supply is an important part of their policy toolkit, allowing them to stabilize growth and inflation in times of need.

Data privacy is also a major concern. This is a particularly poignant issue after Facebook’s well-documented controversies on the data security and privacy front; it will be a key focus of any future stablecoin.

Right now, three of the four pieces necessary for an ecommerce transformation at the hands of stablecoins are in place — the appropriate technology, consumer demand, and corporate champions.

If an amenable regulatory environment materializes in the next few years, the adoption of stablecoins as a means of payment might boost adoption of blockchain technologies above and beyond the current niche uses, and has the potential to breach the barriers to entry in the e-commerce market.

If key financial institutions like the Fed give their stamp of approval, we might really see a lower reliance on fiat currency and actual paper money in our day-to-day lives. If more and more of our purchases are made online and cashless shops become more popular, why the need to exchange digital currency into paper money?

Large retailers like Amazon might launch their own digital coins. Soon, we may not be wondering whether crypto will ever catch on, but whether we’re going to miss seeing George Washington’s face.-

Francisco Gimeno - BC Analyst Today is Bitcoin Pizza Day! With China launching its own national crypto, French experimenting with a digital Euro, Libra trying again, we hear now about a possible digital coin from the US Federal Reserve. A good early step, fully understood when all conditions are suitable for their acceptance around the financial sector.

-

-

Blockchain started as a way to move bitcoin from point A to point B, but it is now being used by a host of big companies to monitor and move any number of assets around the world as easily as sending an email.

Blockchain started as a way to move bitcoin from point A to point B, but it is now being used by a host of big companies to monitor and move any number of assets around the world as easily as sending an email.

Our second annual Blockchain 50 represents enterprises embracing the technology underlying cryptocurrencies like bitcoin and using it to speed up business processes, increase transparency and potentially save billions of dollars.

To qualify, Blockchain 50 members must be generating no less than $1 billion in revenue annually or be valued at $1 billion or more.

From the instantaneous settlement of German government bonds to verifying the provenance of diamonds mined in Africa and bringing liquidity to a small supplier of sliding shower doors in Zhongshan, China, this year’s members have largely moved beyond the theoretical benefits of blockchain, to generating very real revenues and cost savings.

While many companies on our new list are household names like Vanguard, Square and Microsoft, a few cryptocurrency native startups like Bitfury have already met our criteria and are on their way to becoming the blue chips of the digital age.Future of Blockchain: Fintech 50 2020

Amazon

Seattle, Washington

As an extension of Amazon Web Services, the e-commerce behemoth offers blockchain tools for companies that don’t want to build their own. In Australia, Nestlé used Amazon’s blockchain product to help launch a new coffee brand, “Chain of Origin,” where consumers can look inside the coffee’s supply chain: They can scan a QR code to see at which small farm the beans were planted and where they were roasted. Other Amazon blockchain clients include Sony Music Japan, BMW, Accenture and South Korean craft brewery Jinju Beer.Blockchain: Hyperledger Fabric

Key Executive: Rahul Pathak, general manager for databases, analytics and blockchain at AWS

—Ant Financial

Hangzhou, China

Its finance platform called Duo-Chain has facilitated $1.5 billion in quick loans and other transactions for cash constrained suppliers like Sichuan’s GuanYong Computer and others. Ant uses its own proprietary blockchain to verify the receivables and make payments.Blockchain: Ant Blockchain Technology, Hyperledger Fabric and Enterprise Ethereum (Quorum)

Key Executive: Geoff Jiang, vice president of Ant Financial

—Anthem

Indianapolis, Indiana

At the end of 2019 the health insurance company started rolling out a blockchain-powered feature that allows patients to securely access and share their medical data. In the next two to three years, all 40 million members will gain access to it.Blockchain: Hyperledger Fabric

Key Executives: Mariya Filipova, VP Innovation, Plamen Petrov, VP Exponential Technologies, Rajeev Ronanki, Chief Digital Officer

—Aon

London, England

Besides brokering a $255 million policy protecting Coinbase against losses from hacking, Aon is building a blockchain platform to speed up insurance operations. Creating a new reinsurance contract—where insurers buy their own insurance to hedge their risk—is clunky, with insurers using different systems to send and receive quotes. Aon is building a shared platform, where big reinsurers can work off of the same system. So far Everest Re and RenaissanceRe have signed on to test and help design the project.Blockchain: R3 Corda

Key Executive: Robert Olson, chief information officer of Aon Reinsurance Solutions

—Baidu

Beijing, China

Search giant Baidu has been bullish on blockchain for years. One of its affiliates Duxiaoman Financial, built a canine version of Cryptokitties in early 2018, which allows millions of Chinese to adopt and trade cute digital puppies, each distinct, that “live” on the blockchain. Another Duxiaoman service offers student loans, but funds are disbursed only after the technology is used to verify grades. At Baidu itself there are also numerous projects including XuperChain, which uses artificial intelligence to analyze copyright infringement allegations and reduce the time to a judgement from three months to one week.Blockchain: Hyperledger Fabric

Key Executive: Li Feng, head of blockchain

—Bitfury

Amsterdam, Netherlands

The mining—cryptocurrency, not minerals—equipment maker has also customized the bitcoin blockchain so that clients can build their own apps. Graduates of Dubai’s Synergy University, for example, can use a Bitfury’s Exonum blockchain to verify their credentials for potential employers.Blockchain: Bitcoin, Exonum

Key Executive: Chris Dickson, head of blockchain solutions

—BMW

Munich, Germany

The luxury automaker currently has a pilot program with suppliers with plants in Europe, Mexico and the U.S. and is using blockchain to track materials, components and parts across its supply chain. BMW is also a member of the Mobile Open Blockchain Initiative (MOBI), which is made up of a consortium of auto manufacturers including Honda and Ford. In July 2019, Mobi launched the auto industry’s first blockchain vehicle identity standard, which gives new cars a digital identity. The technology could eventually track events throughout a car’s life and be used to connect vehicles to share information, track speed, location, direction of travel, braking and even driver intention (like changing lanes).Blockchain: Hyperledger Fabric, Ethereum, Quorum, Corda and Tezos

Key Executive: Andre Luckow, head of distributed ledger and emerging

technologies

—Broadridge

New York City, New York

Last summer, ADP spinoff Broadridge acquired blockchain software built by financial services firm Northern Trust designed to help manage the entire life cycle of private equity investments. The tool automates the manual middle office functions of PE transactions, like managing legal agreements, and streamlines the process of gathering data and communicating with investors. It’s currently available for funds based in Guernsey and the state of Delaware. In the second half of 2020, Broadridge has plans to go live executing bilateral repurchase agreements (repos) on the blockchain.Blockchain: Hyperledger Fabric, Quorum, Corda, DAML (Digital Asset Modeling Language)

Key Executive: Mike Tae, Head of Broadridge’s Corporate Strategy

—Cargill

Wayzata, Minnesota

America’s largest private company launched an open-sourced privacy-focused platform called Splinter in 2019, which enables members of its vast supply chain to use distributed applications to communicate and transact. Cargill is mum on details but says the applications are vast and touch all aspects of the company’s business transactions. Cargill began testing Intel’s Hyperledger Sawtooth before Thanksgiving 2017 to track turkeys from farm to supermarket and also previously helped build a customized blockchain called Hyperledger Grid.Blockchain: Hyperledger Sawtooth, Hyperledger Grid

Key Executive: David Cecchi, senior director, engineering

—China Construction Bank

Shanghai, China

The world’s second-largest bank has nine blockchain projects in operation, including one that helps trace pharmaceuticals to their origin, another that tracks carbon credits, and one that shows how government grants are spent. BCTrade is farthest along connecting 60 financial institutions including Postal Savings Bank of China, the Bank of Shanghai and the Bank of Communications, to 3,000 manufacturers and import & export trading companies involved in commerce. Today, a cash-strapped exporter waiting for a shipment to be confirmed can take out a loan in a matter of minutes by sharing a record of the future receivables on the blockchain.Blockchain: Hyperchain, Hyperledger Fabric

Key Executive: Lei Xing, blockchain as a service platform lead

—Citigroup

New York City, New York

Citi recently digitally issued its first letter of credit using its trade-finance-focused blockchain Komgo. Citi is also working with Goldman Sachs and 13 other trading firms to automate the matching and reconciliation of equity-swaps derivative contracts using Axoni’s Axcore blockchain. By moving the entire workflow to blockchain, Citi hopes to reduce errors and operational costs and minimize disputes over the valuation of assets. Click here to read more.Blockchain: Axcore, Symbiont Assembly, Quorum

Key Executive: Puneet Singhvi, markets and securities services lead for Blockchain

—Coinbase

San Francisco, California

Eight years after its start, Coinbase has opened 35 million accounts, presides over $21 billion of assets and is on target, we estimate, to top $800 million in revenue this year. Think of Coinbase as the blue chip among dozens of cryptocurrency exchanges, abiding by regulations and serving institutional investors, pension funds, endowments and retail investors alike. In February 2020, Coinbase announced that it had received authority from Visa to issue its own credit cards. Click here to read more.Blockchain: Bitcoin, ethereum, XRP and 24 others

Key Executive: Brian Armstrong, cofounder and CEO

—Credit Suisse

Zurich, Switzerland

This Swiss banking giant has been investing in blockchain since 2015, when it became a founding member of blockchain consortium R3. It is now working with the parent company of bitcoin exchange itBit, to settle U.S.-listed equity securities using a blockchain. Another blockchain partnership with Deutsche Börse has reduced settlement times for government and corporate bonds to the same day.Blockchain: Corda, Paxos

Key Executive: Emmanuel Aidoo, head of digital assets markets

—Daimler

Stuttgart, Germany

The German auto giant has overseen a number of blockchain pilots, ranging from letting Daimler truck owners make payments for fuel using e-euros to issuing a one-year €100 German debt instrument known as a Schuldschein. It is also using blockchain technology to track contracts along the supply chain through subsidiary Mercedes-Benz.Blockchain: Hyperledger, Corda, Ethereum

Key Executive: Jonas von Malottki, Open Source Priority Lead

—De Beers

London, England

The end of blood diamonds? De Beers’ new software, Tracr, follows diamonds, which have undergone 3-D scans, as the gems are mined, cut, polished and sold. Already more than 30 participants, including Signet Jewelers—owner of Kay, Zales and Jared—have signed on. Tens of thousands of stones are being registered per month.Blockchain: Ethereum

Key Executive: Jim Duffy, CEO of Tracr

—Depository Trust & Clearing Corporation (DTCC)

New York City, New York

Global securities warehouse DTCC will soon move its $10 trillion credit derivatives business to a blockchain. These derivatives represent some 50,000 accounts held by some of the largest financial institutions in the world. Previously each institution would keep its own record requiring continuous reconciliations and redundant efforts. DTCC’s new shared ledger will eliminate waste and paperwork.Blockchain: Axcore

Key Executive: Rob Palatnick, global head of technology research and innovation; Jennifer Peve, managing director, business innovation

—Dole Foods

Charlotte, North Carolina

After several high-profile recalls last decade, Dole has adopted blockchain across all vegetable processing, for millions of pounds of lettuce, spinach and coleslaw. Customers at Walmart can now check where their fruit comes from by scanning a code used by farmers. Dole’s fruit business is next. Dole’s new level of traceability starts on the farm and ends at the grocery aisle. Current transaction volumes through partner IBM Food Trust are about 11,300 transactions a day, or 2.3 million a year.Blockchain: IBM Blockchain, Hyperledger Fabric

Key Executive: Natalie Dyenson, Vice President, Food Safety & Quality

—Facebook

Menlo Park, California

Last June Facebook boldly announced its plans for libra, a cryptocurrency backed by a basket of stable assets including the U.S. dollar and government bonds. The announcement brought Facebook haters out of the woodwork who were loath to cede monetary control to the same company whose laissez-faire approach to its technology may have contributed to the unexpected outcome of 2016’s presidential election. Already many original libra backers, including Visa and Mastercard, have dropped out of Facebook’s consortium. Stay tuned, however: The Libra Association that administers the blockchain code says it will launch the cryptocurrency in 2020—if it can get regulatory approval.Blockchain: Hotstuff

Key Executive: David Marcus, head of Calibra, Facebook’s cryptocurrency wallet; Morgan Beller, co-creator of Libra, Head of Strategy at Calibra

—Figure

San Francisco, California

This unicorn has facilitated more than $800 million in home equity loans, mortgage and student loan refinancings for lenders including Caliber Home Loans. Franklin Templeton is among the financial service firms that manage nodes to validate transactions on its Provenance blockchain platform. All documents are stored and algorithmically verified on the blockchain.Blockchain: Hyperledger Fabric

Key Executive: Mike Cagney, cofounder and CEO; Jennifer Mitrenga, head of Americas, Provenance

—Foxconn

Taipei, Taiwan

The iPhone maker’s trade-finance venture, Chained Finance, pays more than 20 electronics suppliers using digital coins minted on the Ethereum blockchain. The result: Financing costs have plummeted from annual percentage rates as high as 24% to 10%, and the time needed to get funding has been cut from seven days to same day. Foxconn uses Ethereum’s blockchain, famous for innovating so-called smart contracts, which automate financial transactions.Blockchain: Ethereum

Key Executive: Jack Lee, acting CEO, Chained Finance

—General Electric

Boston, Massachusetts

GE is actively exploring blockchain through its $30 billion (revs) Aviation subsidiary, which has built what it calls a “back-to-birth” record of an airplane engine that records important details of the manufacturing process and specifics about maintenance performed. In an industry where complete, easily accessible records are critical to productivity (airline parts without proper documentation are not easily bought and sold), GE’s blockchain team has created a digitized paper trail in order to prevent engines with incomplete paperwork from sitting unused.Blockchain: Microsoft Azure, Corda, Quorum, Hyperledger

Key Executive: David Havera, Blockchain Lead

—Google

Mountain View, California

In June, the search giant announced that it was integrating its BigQuery data analytics platform with Chainlink, allowing data from outside sources to be used in applications built directly on the blockchain. The partnership could help process futures contracts, settle speculative bets and make transactions more private. Earlier in 2019, Google launched a suite of tools on BigQuery that made blockchain data for bitcoin and seven other major cryptocurrencies fully searchable.Blockchain: Chainlink, Bitcoin, Ethereum, Bitcoin Cash, Ethereum Classic, Litecoin, Zcash, Dogecoin, Dash

Key Executive: Allen Day, developer advocate, Google Cloud

—Honeywell

Charlotte, North Carolina