Opinions

-

Traditionally one of the greatest obstacles to rapid technological progress in society has been the inability for worthy projects to find the funding required for an entrepreneur to turn a vision into a reality. In response to this problem, there has been a lot of innovation surrounding alternative funding mechanisms over the past few decades.

Traditionally one of the greatest obstacles to rapid technological progress in society has been the inability for worthy projects to find the funding required for an entrepreneur to turn a vision into a reality. In response to this problem, there has been a lot of innovation surrounding alternative funding mechanisms over the past few decades.

These innovations have occurred most notably in the Venture Capital and Angel Investor circles, as well as in crowdfunding platforms such as Kickstarter. Now, though, there is another funding mechanism on the scene which is claiming to revolutionise the funding of tech projects… token sales.

A token sale is simply the creation and the sale of a cryptographically backed token (cryptocurrency) on a blockchain platform. Within this umbrella term, there are three main types of token sales: Initial Coin Offerings (ICOs), Security Token Offerings (STOs) and Utility Token Offerings (UTOs).

Historically speaking, out of the various types of token sales ICOs have grabbed the most headlines and media attention. For example, early in 2018, during the ICO hysteria, EOS raised over $4 Billion in its ICO, whilst on aggregate 2018 brought in over $21.5 billion from ICO and UTO sales.

However, since then the ICO/UTO bubble has burst and many have lost faith in the entire token sale enterprise. In their minds, this was a bubble like every other and since it has burst, it is time to move on. Although that may be true for many people, there are still quite a few who see ‘The Tokenization of Everything’ as an inevitability – to them, it is a matter of when not if.

The Tokenization of Everything (TOE) refers to a world where anything from patents to houses, to concept cars, can be represented by a blockchain-based token and then sold/traded with anyone, anywhere. So then, out of these two camps, who is right?

Short-term outlook (-12 months)

The token sale model receiving the most hype at the moment is the STO, to the extent that a quick Google search of the term will show many proclaiming 2019 to be ‘the year of the STO’. STOs are tokens representing securities, created on top of an existing blockchain platform.

The main benefit of using an STO as opposed to any other type of token offering is that it operates in a space with clear regulatory frameworks which guide issuers and investors alike. The claims being made are that this token sale model will revolutionise all types of project funding, specifically where VCs, Angel Investors or IPOs are involved.

The perceived benefits are summarised in a Nasdaq issued report (Security Tokens Set To Take Center Stage in 2019) which states that“Security tokens digitally represent ownership in any asset, such as a piece of a tech startup or a venture capital fund and can provide investors with various rights to that company or fund.

Furthermore, Security tokens provide liquidity to investors, access to compliance features to issuers, and a framework for oversight to regulators. ”Under close inspection of the current state of the market, however, these claims fall apart. The infrastructure that is necessary for a fully optimised STO market to operate has barely begun construction, who knows how long it will take to build?

Furthermore, the claim that STOs will provide token owners access to a liquid secondary market also seems to be a wild exaggeration. Quite simply, the Securities and Exchange Commission (SEC) in the US has very strict requirements and protocols for self-proclaimed ‘Securities Exchanges’ and will take action against any exchange not complying with these requirements.

Consequently, there are no sizeable exchanges accepting STOs for secondary sale at this moment. Essentially this means the token becomes “a zombie coin” in the words of Trevor Koverko CEO of PolyMath (an STO platform). Taking this into consideration along with other points not mentioned here, the short-term prospects for STOs as well as the Tokenization of Everything is pretty bleak.

But is this the case for the medium to long-term?

Medium to long-term outlook (1-10 years)

Due to the factors stated above, it seems that the TOE hypothesis and all the promise that holds for tech startups/companies will not be coming true in the short term.

However, I believe the medium to long-term prospects to be much more promising.Let me explain: ICOs will always be the go-to funding mechanism for new blockchain platforms, this is simply due to the historical success of this strategy.

For example, EOS, Ethereum and Waves all did ICOs to raise initial capital for their projects and are now amongst the biggest and most successful blockchain platforms in the world. So too does it appear that UTOs will also be the best option for teams building Decentralized Apps (Dapps) on top of these blockchains e.g. games, lending platforms, sharing economy apps etc.

Furthermore, reiterating what was previously mentioned about STOs – I do believe they will be a viable alternative to legacy systems (VCs, Angel Investors and IPOs) but the timeline will be much longer than the community perceive and there are other questions that need to be answered before we can go forward.

Due to the immaturity of the industry and no precedent having yet been set to call upon, I will leave you with some open-ended questions to consider with regard to the role of STOs in the TOE:?

How hard/long/expensive is it to become a registered STO in your jurisdiction and is it worth it??

How big is the liquidity pool for these STO exchanges (plus their secondary markets)??

What exactly can be considered an STO and will we need another token sale model in order to make the TOE a reality?

In summary, the token sale market is shrouded with uncertainty at this time; there are a lot of big claims being thrown around but little evidence to show their viability at this moment.

That being said, token sales and their applications to the technology industry can offer massive benefits relative to legacy systems, especially for those who do not have access to sophisticated and fairly stable financial systems (like we do in Europe), and the fact that they raised over $21 Billion in 2018 is an indicator of this truth.

What we need to see going forward is attention being paid to the development of the infrastructure for these markets and clearer governmental frameworks surrounding the space.

There must be substantial progress in both of these areas before the Tokenization of Everything can occur and unlock the entrepreneurial potential pent up in entrepreneurs and innovators all across the world.

By Anthony Broderick – Cryptocurrency Analyst & Media Editor atCoinSchedule

CoinSchedule Limited is an Information Society Service Provider. If you would like to have your company featured in the Irish Tech News Business Showcase, get in contact with us at [email protected] or on Twitter: @SimonCocking-

- 1

Francisco Gimeno - BC Analyst Tokenisation of Everything should be considered a long term goal. As it is now, not everything should be tokenised and not all tokens are useful. But we believe the road to full implementation of the 4th IR leads to tokenisation as the way to create a new economy and furthermore, to empower the whole society to fully participate, and not be anymore passive users of financial schemes of those in charge now.

-

-

Facebook CEO Mark Zuckerberg is exploring the possibility of leveraging blockchain technology for the company’s third-party login services.

Facebook CEO Mark Zuckerberg is exploring the possibility of leveraging blockchain technology for the company’s third-party login services.

In an interview with Harvard Law Professor Jonathan Zittrain on Wednesday, Zuckerberg said a move from the existing centralized Facebook Connect to a distributed system could empower users and app developers alike.Volume 0% Multiple reports have been floating since last year on Facebook‘s possible plans with blockchain technology, but this marks the first time a company representative has shared any tangible details.

According to Zuckerberg, the users would be able to store their information on a decentralized system and have the choice of logging into various platforms without going through an intermediary — in this case, Facebook. Zuckerburg says this should give users greater control over their data.

Zuckerberg pointed out that this system would also benefit app developers whose access to users’ data can be cut by intermediaries like Facebook and Google at any time, if they are found to be in violation of their policies.It’s worth noting that Facebook won’t be the first one to explore this concept.

Indeed, a ton of blockchain startups have raised money over the years promising to make this blockchain dream a reality. Unsurprisingly, none of them have yet succeeded in creating a useful identity management solution.Zuckerberg himself admits that he hasn’t yet found a way for blockchain-powered logins to work in reality.

But even if with all its resources and technical talent, Facebook manages to make this a reality, will it make user data more secure? The use of blockchain technology can ensure greater security and privacy during the transaction process of the information itself, but the data will be accessible and retainable to other parties in the same manner as with centralized means.

The user will still have no control over how the information is treated once they have chosen to share it with the third party. Unfortunately, this is where most data breaches take place.Consider the infamous Cambridge Analytica incident, for example. Facebook users thought they were giving consent to have their data shared with an app developed by a Cambridge University psychology professor.

In turn, the professor ended up sharing the data with third parties leading to one of the largest political scandals in the digital age’s history.The use of blockchain for giving consent in this case couldn’t have prevented this incident. But it would have shifted the responsibility of securing personal information the users themselves instead of Facebook. It’s unlikely that individual users will be better equipped to tell apart bogus apps than the social media giant.

In light of the multiple data breach revelations that came in the aftermath of Cambridge Analytica, Facebook has been facing scrutiny from multiple federal agencies in the US and authorities elsewhere in the world.It is no wonder that the company is looking into options on limiting its legal liabilities. A blockchain-based login system could allow exactly that, with the onus of securing their personal information shifting entirely to the users themselves.

Nevertheless, it will be no cakewalk to make this concept a reality, even for a company like Facebook.In addition to the usual challenges faced with building products on blockchain, Facebook has to battle the fact that the use of blockchain is completely antithetical to Facebook‘s existence.

Zuckerberg kept talking about removing the intermediary from this process throughout the interview. But, Facebook is the intermediary as himself admits. Essentially, Facebook wants to offer a service to ensure that the users don’t have to rely on Facebook to securely login on a third-party app?

Someone solve this riddle for me.It doesn’t sound like Facebook has its idea sorted out. I, for one, won’t be expecting to see this proposition come to life anytime soon.-

Francisco Gimeno - BC Analyst Facebook continues to be the opposite of what blockchain means in social media. Facebook uses its users. Blockchain empowers users to get rewards, to be active owners and handlers of their own data. How is FB going to react long term to this? Unless they deeply change their concept of data handling, the perspective is not good.

-

-

In his 2008 white paper that first proposed bitcoin, the anonymous Satoshi Nakamoto concluded with: “We have proposed a system for electronic transactions without relying on trust.” He was referring to blockchain, the system behind bitcoin cryptocurrency.

In his 2008 white paper that first proposed bitcoin, the anonymous Satoshi Nakamoto concluded with: “We have proposed a system for electronic transactions without relying on trust.” He was referring to blockchain, the system behind bitcoin cryptocurrency.

The circumvention of trust is a great promise, but it’s just not true. Yes, bitcoin eliminates certain trusted intermediaries that are inherent in other payment systems like credit cards. But you still have to trust bitcoin—and everything about it.WIRED OPINION

ABOUT

Bruce Schneier is a security technologist who teaches at the Harvard Kennedy School. He is the author, most recently, of Click Here to Kill Everybody: Security and Survival in a Hyper-Connected World.

Much has been written about blockchains and how they displace, reshape, or eliminate trust. But when you analyze both blockchain and trust, you quickly realize that there is much more hype than value. Blockchain solutions are often much worse than what they replace.

First, a caveat. By blockchain, I mean something very specific: the data structures and protocols that make up a public blockchain. These have three essential elements.

The first is a distributed (as in multiple copies) but centralized (as in there’s only one) ledger, which is a way of recording what happened and in what order.

This ledger is public, meaning that anyone can read it, and immutable, meaning that no one can change what happened in the past.

The second element is the consensus algorithm, which is a way to ensure all the copies of the ledger are the same.

This is generally called mining; a critical part of the system is that anyone can participate. It is also distributed, meaning that you don’t have to trust any particular node in the consensus network. It can also be extremely expensive, both in data storage and in the energy required to maintain it.

Bitcoin has the most expensive consensus algorithm the world has ever seen, by far.Finally, the third element is the currency. This is some sort of digital token that has value and is publicly traded. Currency is a necessary element of a blockchain to align the incentives of everyone involved. Transactions involving these tokens are stored on the ledger.

Private blockchains are completely uninteresting. (By this, I mean systems that use the blockchain data structure but don’t have the above three elements.) In general, they have some external limitation on who can interact with the blockchain and its features.

These are not anything new; they’re distributed append-only data structures with a list of individuals authorized to add to it. Consensus protocols have been studied in distributed systems for more than 60 years. Append-only data structures have been similarly well covered.

They’re blockchains in name only, and—as far as I can tell—the only reason to operate one is to ride on the blockchain hype.All three elements of a public blockchain fit together as a single network that offers new security properties. The question is: Is it actually good for anything? It's all a matter of trust.

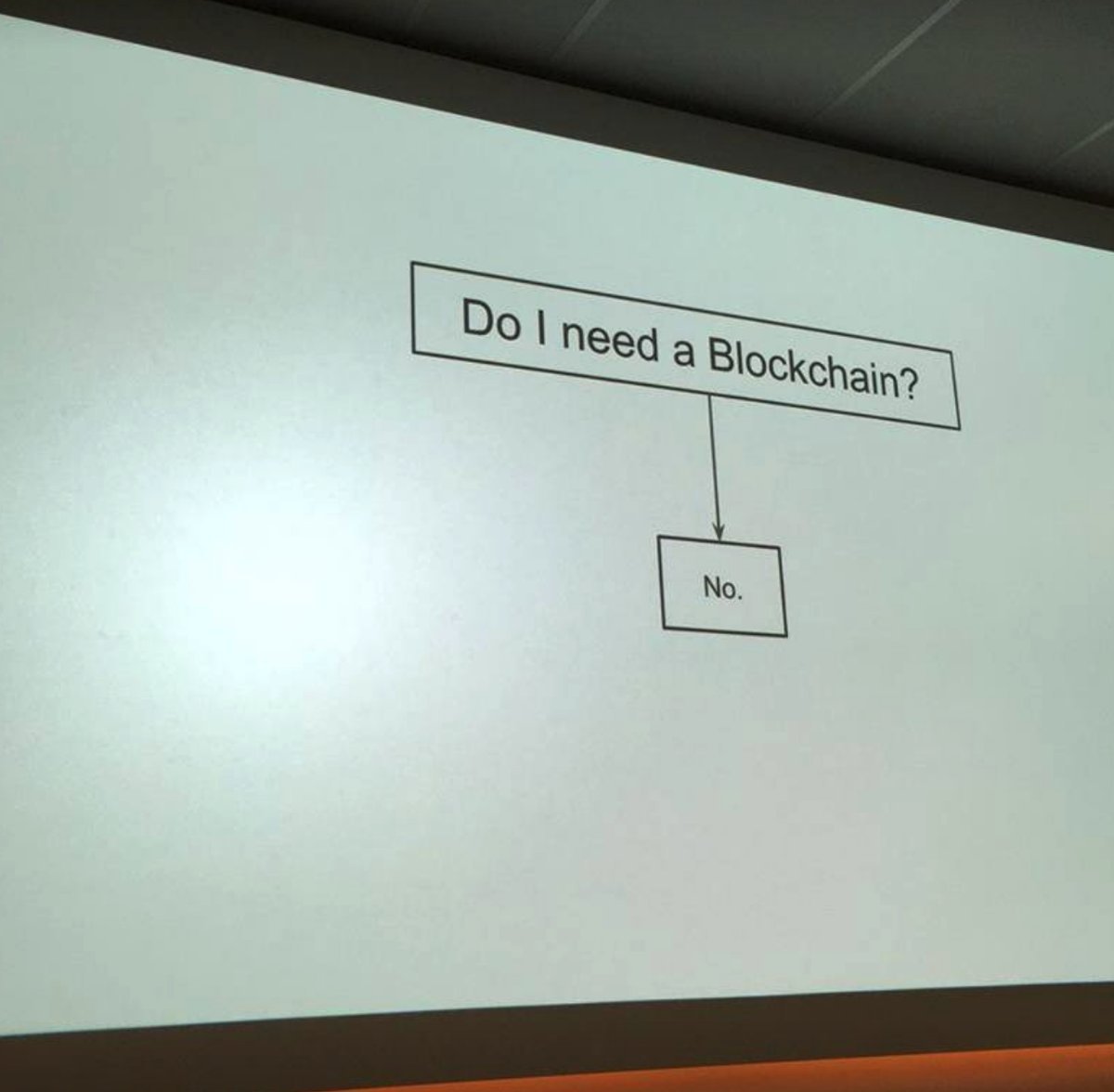

View image on Twitter

11.8K people are talking about thisTwitter Ads info and privacy vinton g cerf@vgcerfSimple flowchart:

vinton g cerf@vgcerfSimple flowchart:

32.3K6:49 PM - Jul 19, 2018

Trust is essential to society. As a species, humans are wired to trust one another. Society can’t function without trust, and the fact that we mostly don’t even think about it is a measure of how well trust works.The word “trust” is loaded with many meanings.

There’s personal and intimate trust. When we say we trust a friend, we mean that we trust their intentions and know that those intentions will inform their actions. There’s also the less intimate, less personal trust—we might not know someone personally, or know their motivations, but we can trust their future actions.

Blockchain enables this sort of trust: We don’t know any bitcoin miners, for example, but we trust that they will follow the mining protocol and make the whole system work.Most blockchain enthusiasts have a unnaturally narrow definition of trust.

They’re fond of catchphrases like “in code we trust,” “in math we trust,” and “in crypto we trust.

” This is trust as verification. But verification isn’t the same as trust.In 2012, I wrote a book about trust and security, Liars and Outliers. In it, I listed four very general systems our species uses to incentivize trustworthy behavior. The first two are morals and reputation.

çThe problem is that they scale only to a certain population size. Primitive systems were good enough for small communities, but larger communities required delegation, and more formalism.

The third is institutions. Institutions have rules and laws that induce people to behave according to the group norm, imposing sanctions on those who do not. In a sense, laws formalize reputation.

Finally, the fourth is security systems. These are the wide varieties of security technologies we employ: door locks and tall fences, alarm systems and guards, forensics and audit systems, and so on.

These four elements work together to enable trust. Take banking, for example.

Financial institutions, merchants, and individuals are all concerned with their reputations, which prevents theft and fraud. The laws and regulations surrounding every aspect of banking keep everyone in line, including backstops that limit risks in the case of fraud.

And there are lots of security systems in place, from anti-counterfeiting technologies to internet-security technologies.In his 2018 book, Blockchain and the New Architecture of Trust, Kevin Werbach outlines four different “trust architectures.” The first is peer-to-peer trust.

This basically corresponds to my morals and reputational systems: pairs of people who come to trust each other. His second is leviathan trust, which corresponds to institutional trust.

You can see this working in our system of contracts, which allows parties that don’t trust each other to enter into an agreement because they both trust that a government system will help resolve disputes. His third is intermediary trust. A good example is the credit card system, which allows untrusting buyers and sellers to engage in commerce.

His fourth trust architecture is distributed trust. This is emergent trust in the particular security system that is blockchain.

What blockchain does is shift some of the trust in people and institutions to trust in technology. You need to trust the cryptography, the protocols, the software, the computers and the network. And you need to trust them absolutely, because they’re often single points of failure.

When that trust turns out to be misplaced, there is no recourse. If your bitcoin exchange gets hacked, you lose all of your money. If your bitcoin wallet gets hacked, you lose all of your money. If you forget your login credentials, you lose all of your money.

If there’s a bug in the code of your smart contract, you lose all of your money. If someone successfully hacks the blockchain security, you lose all of your money. In many ways, trusting technology is harder than trusting people. Would you rather trust a human legal system or the details of some computer code you don’t have the expertise to audit?

Blockchain enthusiasts point to more traditional forms of trust—bank processing fees, for example—as expensive. But blockchain trust is also costly; the cost is just hidden.

For bitcoin, that's the cost of the additional bitcoin mined, the transaction fees, and the enormous environmental waste.

Blockchain doesn’t eliminate the need to trust human institutions. There will always be a big gap that can’t be addressed by technology alone. People still need to be in charge, and there is always a need for governance outside the system.

This is obvious in the ongoing debate about changing the bitcoin block size, or in fixing the DAO attack against Ethereum. There’s always a need to override the rules, and there’s always a need for the ability to make permanent rules changes.

As long as hard forks are a possibility—that’s when the people in charge of a blockchain step outside the system to change it—people will need to be in charge.Any blockchain system will have to coexist with other, more conventional systems. Modern banking, for example, is designed to be reversible. Bitcoin is not.

That makes it hard to make the two compatible, and the result is often an insecurity. Steve Wozniak was scammed out of $70K in bitcoin because he forgot this.Blockchain technology is often centralized.

Bitcoin might theoretically be based on distributed trust, but in practice, that’s just not true. Just about everyone using bitcoin has to trust one of the few available wallets and use one of the few available exchanges.

People have to trust the software and the operating systems and the computers everything is running on. And we've seen attacks against wallets and exchanges. We’ve seen Trojans and phishing and password guessing.

Criminals have even used flaws in the system that people use to repair their cell phones to steal bitcoin.Moreover, in any distributed trust system, there are backdoor methods for centralization to creep back in. With bitcoin, there are only a few miners of consequence. There’s one company that provides most of the mining hardware.

There are only a few dominant exchanges. To the extent that most people interact with bitcoin, it is through these centralized systems. This also allows for attacks against blockchain-based systems.

These issues are not bugs in current blockchain applications, they’re inherent in how blockchain works. Any evaluation of the security of the system has to take the whole socio-technical system into account. Too many blockchain enthusiasts focus on the technology and ignore the rest.To the extent that people don’t use bitcoin, it’s because they don’t trust bitcoin.

That has nothing to do with the cryptography or the protocols. In fact, a system where you can lose your life savings if you forget your key or download a piece of malware is not particularly trustworthy.

No amount of explaining how SHA-256 works to prevent double-spending will fix that.Similarly, to the extent that people do use blockchains, it is because they trust them. People either own bitcoin or not based on reputation; that’s true even for speculators who own bitcoin simply because they think it will make them rich quickly.

People choose a wallet for their cryptocurrency, and an exchange for their transactions, based on reputation. We even evaluate and trust the cryptography that underpins blockchains based on the algorithms’ reputation.To see how this can fail, look at the various supply-chain security systems that are using blockchain.

A blockchain isn’t a necessary feature of any of them. The reasons they’re successful is that everyone has a single software platform to enter their data in. Even though the blockchain systems are built on distributed trust, people don’t necessarily accept that.

For example, some companies don’t trust the IBM/Maersk system because it’s not their blockchain.

Irrational? Maybe, but that’s how trust works. It can’t be replaced by algorithms and protocols. It’s much more social than that.

Still, the idea that blockchains can somehow eliminate the need for trust persists. Recently, I received an email from a company that implemented secure messaging using blockchain. It said, in part: “Using the blockchain, as we have done, has eliminated the need for Trust.

” This sentiment suggests the writer misunderstands both what blockchain does and how trust works.

Do you need a public blockchain?

The answer is almost certainly no. A blockchain probably doesn’t solve the security problems you think it solves. The security problems it solves are probably not the ones you have. (Manipulating audit data is probably not your major security risk.) A false trust in blockchain can itself be a security risk.

The inefficiencies, especially in scaling, are probably not worth it. I have looked at many blockchain applications, and all of them could achieve the same security properties without using a blockchain—of course, then they wouldn’t have the cool name.Honestly, cryptocurrencies are useless.

They're only used by speculators looking for quick riches, people who don't like government-backed currencies, and criminals who want a black-market way to exchange money.

To answer the question of whether the blockchain is needed, ask yourself: Does the blockchain change the system of trust in any meaningful way, or just shift it around?

Does it just try to replace trust with verification? Does it strengthen existing trust relationships, or try to go against them? How can trust be abused in the new system, and is this better or worse than the potential abuses in the old system?

And lastly: What would your system look like if you didn’t use blockchain at all?If you ask yourself those questions, it's likely you'll choose solutions that don't use public blockchain.

And that'll be a good thing—especially when the hype dissipates.

WIRED Opinion publishes pieces written by outside contributors and represents a wide range of viewpoints.

Read more opinions here. Submit an op-ed at [email protected]-

Admin

Admin - 2 comments

- 5 likes

- Like

- Share

-

Aleksandar Mladenovic very nice

-

Francisco Gimeno - BC Analyst We actually like this article. And not because of the evident "missing the whole point" the author is having, but because talks about trust, and the confusion many bitcoin or crypto or blockchain maximalists have with that particular word. Blockchain, we always say, is a tool. And we trust the tool to perform if WE are using it properly. Blockchain is not a promise of salvation in which we should put blind faith. Blockchain IS A TOOL, which together with robotics, AI, IoT, etc, will bring the new economy and, hopefully, a better society in the 4th IR we are already living. We also hope, with the author, that the hype dissipates soon. And then, useless products, useless cryptos, etc. Bitcoin and other solid cryptos will stay. Well founded blockchain platforms will thrive. We will be then on the right track, without the hype fog.

-

-

Blockchain has yet to become the game-changer some expected. A key to finding the value is to apply the technology only when it is the simplest solution available.

Blockchain over recent years has been extolled as a revolution in business technology. In the nine years since its launch, companies, regulators, and financial technologists have spent countless hours exploring its potential. The resulting innovations have started to reshape business processes, particularly in accounting and transactions.

Amid intense experimentation, industries from financial services to healthcare and the arts have identified more than 100 blockchain use cases. These range from new land registries, to KYC applications and smart contracts that enable actions from product processing to share trading. The most impressive results have seen blockchains used to store information, cut out intermediaries, and enable greater coordination between companies, for example in relation to data standards.

One sign of blockchain’s perceived potential is the large investments being made. Venture-capital funding for blockchain startups reached $1 billion in 2017. IBM has invested more than $200 million in a blockchain-powered data-sharing solution for the Internet of Things, and Google has reportedly been working with blockchains since 2016. The financial industry spends around $1.7 billion annually on experimentation.

There is a clear sense that blockchain is a potential game-changer. However, there are also emerging doubts. A particular concern, given the amount of money and time spent, is that little of substance has been achieved. Of the many use cases, a large number are still at the idea stage, while others are in development but with no output.

The bottom line is that despite billions of dollars of investment, and nearly as many headlines, evidence for a practical scalable use for blockchain is thin on the ground.Infant technology

From an economic theory perspective, the stuttering blockchain development path is not entirely surprising. It is an infant technology that is relatively unstable, expensive, and complex. It is also unregulated and selectively distrusted. Classic lifecycle theory suggests the evolution of any industry or product can be divided into four stages: pioneering, growth, maturity, and decline (exhibit).

Stage 1 is when the industry is getting started, or a particular product is brought to market. This is ahead of proven demand and often before the technology has been fully tested. Sales tend to be low and return on investment is negative. Stage 2 is when demand begins to accelerate, the market expands and the industry or product “takes off.”Exhibit

Across its many applications, blockchain arguably remains stuck at stage 1 in the lifecycle (with a few exceptions). The vast majority of proofs of concept (POCs) are in pioneering mode (or being wound up) and many projects have failed to get to Series C funding rounds.

One reason for the lack of progress is the emergence of competing technologies. In payments, for example, it makes sense that a shared ledger could replace the current highly intermediated system. However, blockchains are not the only game in town.

Numerous fintechs are disrupting the value chain. Of nearly $12 billion invested in US fintechs last year, 60 percent was focused on payments and lending. SWIFT’s global payments innovation initiative (GPI), meanwhile, is addressing initial pain points through higher transaction speeds and increased transparency, building on bank collaboration.

Blockchain players in the payments segment, such as Ripple, are increasingly partnering with nonbank payments providers, the businesses of which may be a better fit for blockchain technology. These companies may also be willing to move forward more rapidly with integration.

In addition, the payments industry faces a classic innovator’s dilemma: incumbents understand that investing in disruption, and the likely resulting rise in customer expectations for faster, easier, and cheaper services, may lead to cannibalization of their own revenues.

Given the range of alternative payments solutions and the disincentives to investment by incumbents, the question is not whether blockchain technology can provide an alternative, but whether it needs to? Occam’s razor is the problem-solving principle that the simplest solution tends to be the best. On that basis blockchain’s payments use cases may be the wrong answer.Industry caution

Some sense of this dilemma is starting to feed through to industry. Early blockchain development was led by financial services, which from 2012 to 2015 assigned big resources where it was felt processes could be streamlined.

Banks and others saw activities such as trade finance, derivatives netting and processing, and compliance (alongside payments) as prime candidates. Numerous companies set up innovation labs, hired blockchain gurus, and invested in start-ups and joint ventures.

A leading industry consortium attracted more than 200 financial institutions to its ecosystem, conceived to deliver the next generation of blockchain technology in finance.

As financial services led, others followed. Insurers saw the chance for contract and guarantee efficiencies and the potential to share intelligence on underwriting and fraud. The public sector looked at how it could update its sprawling networks, creating more transparent and accessible public records.

Automakers envisaged smart contracts sitting on top of the blockchain to automate leasing and hire agreements. Others spotted a chance to modernize accounting, contracting, and fractional ownership and to create efficiencies in data management and supply chains.

By the end of 2016, blockchain’s future looked bright. Investment was soaring and some of the structural challenges to the industry appeared to be fading. Technical glitches were being resolved and new, more private versions of the ledger were launched to cater to business demands.

Regulators appeared to be more sanguine than previously, focusing on communication, adaptation, and debate rather than impediment.From an industry lifecycle perspective, however, a more complex dynamic was emerging.

Just as the financial services industry’s blockchain investments were reaching the end of Stage 1—theoretically the moment when they should be gearing up for growth—they appeared to falter.Emerging doubts

McKinsey’s work with financial services leaders over the past two years suggests those at the blockchain “coalface” have begun to have doubts. In fact, as other industries have geared up, the mood music at some levels in financial services has been increasingly of caution (even as senior executives have made confident pronouncements to the contrary).

The fact was that billions of dollars had been sunk but hardly any use cases made technological, commercial, and strategic sense or could be delivered at scale.

By late 2017, many people working at financial companies felt blockchain technology was either too immature, not ready for enterprise level application, or was unnecessary. Many POCs added little benefit, for example beyond cloud solutions, and in some cases led to more questions than answers. There were also doubts about commercial viability, with little sign of material cost savings or incremental revenues.

Another concern was the requirement for a dedicated network. The logic of blockchain is that information is shared, which requires cooperation between companies and heavy lifting to standardize data and systems. The coopetition paradox applied; few companies had the appetite to lead development of a utility that would benefit the entire industry.

In addition, many banks have been distracted by broader IT transformations, leaving little headspace to champion a blockchain revolution.The key question now is whether those doubts are still justified. Or whether it is just that progress in blockchain development has been slower than expected.

Over recent months some financial institutions have begun to recalibrate their blockchain strategies. They have put POCs under more intense scrutiny and adopted a more targeted approach to development funding. Many have narrowed their focus from tens of use cases to one or two and have doubled down on oversight of governance and compliance, data standards, and network adoption.

Some consortia have shrunk their proof of concept rosters from tens in 2016 to just a handful today.The emergence of cryptocurrencies, and in particular Bitcoin, as potential mainstream financial instruments prompted financial services to move first on blockchain experimentation, placing them 18 to 24 months ahead of other industries on the industry lifecycle.

Given that gap, it is not surprising that the earlier concerns in banking are now emerging elsewhere, with initial enthusiasm being eroded by a growing sense of underachievement.

The reality is that rather than following the classic upward curve of the industry lifecycle, blockchain appears to be stalled in the bottom left-hand corner of the X-Y graph. For many, stage 2 isn’t happening. As we enter 2019, blockchain’s practical value is mainly located in three specific areas:- Niche applications: There are specific use cases for which blockchain is particularly well-suited. They include elements of data integration for tracking asset ownership and asset status. Examples are found in insurance, supply chains, and capital markets, in which distributed ledgers can tackle pain points including inefficiency, process opacity, and fraud.

- Modernization value: Blockchain appeals to industries that are strategically oriented toward modernization. These see blockchain as a tool to support their ambitions to pursue digitization, process simplification, and collaboration. In particular, global shipping contracts, trade finance, and payments applications have received renewed attention under the blockchain banner. However, in many cases blockchain technology is a small part of the solution and may not involve a true distributed ledger. In certain instances, renewed energy, investment, and industry collaboration is resolving challenges agnostic of the technology involved.

- Reputational value: A growing number of companies are pursuing blockchain pilots for reputational value; demonstrating to shareholders and competitors their ability to innovate, but with little or no intention of creating a commercial-scale application. Arguably blockchains focused on customer loyalty, IoT networking and voting fall into this category. In this context, claims of being “blockchain enabled” sound hollow.

A future for blockchain?

Given the lack of convincing at-scale use cases and the industry’s seemingly becalmed position in the industry lifecycle, there are reasonable questions to ask about blockchain’s future. Is it really going to revolutionize transaction processing and lead to material cost reductions and efficiency gains?

Are there benefits to be accrued that justify the changes required in market infrastructure and data governance? Or is a secure distributed ledger primarily just one option when contemplating possible replacements for legacy infrastructure?Certainly, there is a growing sense that blockchain is a poorly understood (and somewhat clunky) solution in search of a problem.

The perspective is exacerbated by short-term expense pressures, cultural resistance in some quarters (blockchains may threaten jobs), and concern over disruption to healthy revenue streams. T

here are challenges in respect of governance—making decisions in a decentralized environment is never easy, especially when accountability is equally decentralized. And there are technical impediments, for example in respect to blockchains’ data storage capacity.

It’s estimated there will be over 20 billion connected devices by 2020, all of which will require management, storage, and retrieval of data. However, today’s blockchains are ineffective data receptacles, because every node on a typical network must process every transaction and maintain a copy of the entire state.

The result is that the number of transactions cannot exceed the limit of any single node. And blockchains get less responsive as more nodes are

added, due to latency issues.

Finally, there are security concerns. In smaller networks where validation relies on a majority vote there is manifest potential for fraud (the so-called “51 percent problem”). Another potential security challenge arises from advances in quantum computing.

Google said in 2016 its quantum prototype was 10 million times faster than any computer in its lab. That raises the possibility that quantum computers will be able to hack codes used to authorize cryptocurrency transactions; a particularly troubling threat for a network that claims to be fraud resistant.

Still, all is not lost. It’s likely that many of the validation protocols used today will be upgraded or replaced in the next two to three years, and innovators are already finding solutions.

Cardano, for example, is a so-called third-generation technology and the industry’s first platform to leverage peer-reviewed open source code. The protocol is designed to be quantum-computing resistant.

Private blockchains, meanwhile, are being built to give network members control over who can read the ledger and how nodes are connected.In addition, there have been some promising advances in use cases, particularly away from the financial industry.

Recent experiments in supply chains, identity management, and sharing of public records have been positive. We have seen grocery stores target customers with blockchain-enabled products and services, and shipping executives launch a new real-time registry of containers underpinned by blockchain.

An emerging perspective is that the application of blockchain can be most valuable when it democratizes data access, enables collaboration, and solves specific pain points. Certainly, it brings benefits where it shifts ownership from corporations to consumers, sharing “proof” of supply-chain provenance more vertically, and enabling transparency and automation.

Our suspicion is that it will be these species of uses cases, rather than those in financial services, that will eventually demonstrate the most value.Moving through the cycle: Three key principles

There is no guarantee that any blockchain application will make a sustained move to the second stage in the industry lifecycle. To do so will require a strong rationale, significant capital, and increased standardization.

Fintech leaders will need to take a more nuanced view of their target industries and hire the right talent. However, where there is potential to address pain points at scale, the opportunity remains in place.To get there we see three key principles as minimum conditions for progress:- Organizations must start with a problem. Unless there is a valid problem or pain point, blockchain likely won’t be a practical solution. Also, Occam’s razor applies—it must be the simplest solution available. Firms must honestly evaluate their risk-reward appetite, level of education, and potential gain. They should also assess the potential impact of any project and supporting business case.

- There must be a clear business case and target ROI: Organizations must identify a rationale for investment that reflects their market position and which is supported at board level and by employees, without fear of cannibalization. Companies should pragmatically consider their power to shape ecosystems, establish standards, and address regulatory hurdles, all of which will inform their strategic approach.

- Blockchain’s value comes from its network effects, so a majority of stakeholders must be aligned. There must be a governance agreement covering participation, ownership, maintenance, compliance, and data standards. Finance arrangements must be agreed in advance so that sufficient funding through to commercial launch is guaranteed.

- Companies must agree to a mandate and commit to a path to adoption. Once a use case is selected, companies must assess their ability to deliver. Sufficient economic and technological support is essential. If they pass those hurdles, the next stage is to launch a design process and gather elements including the core blockchain platform and hardware.

- They must then set performance targets (transaction volume and velocity). In parallel, companies should put in place the necessary organizational frameworks, including working groups and communications protocols, so that development, configuration, integration, production, and marketing (to drive adoption at scale) are sufficiently supported.

Conceptually, blockchain has the potential to revolutionize business processes in industries from banking and insurance to shipping and healthcare. Still, the technology has not yet seen a significant application at scale, and it faces structural challenges, including resolving the innovator’s dilemma.

Some industries are already downgrading their expectations (vendors have a role to play there), and we expect further “doses of realism” as experimentation continues.

Companies set on taking blockchain forward must adapt their strategic playbooks, honestly review the advantages over more conventional solutions, and embrace a more hard-headed commercial approach.

They should be quick to abandon applications where there is no incremental value. In many industries, the necessary collaboration may best be undertaken with reference to the ecosystems starting to reshape digital commerce. If they can do all that, and be patient, blockchain may still emerge as Occam’s right answer.

Stay current on your favorite topicsSUBSCRIBEAbout the author(s)Matt Higginson is a partner in McKinsey’s Boston office, Marie-Claude Nadeau is a partner in the San Francisco office, and Kausik Rajgopal is a senior partner in the Silicon Valley office.-

Francisco Gimeno - BC Analyst Blockchain will be used and widely accepted only if its solutions are the most simple, cheaper and interesting than there already existent. This is the Occam's razor. We agree with the author of this report. We strongly believe 2019 is a consolidation year for companies to focus on where and how use blockchain to solve real problems in ways which are better, faster and simpler than other ones.

-

JP Morgan Analysts: Bitcoin Price Could Sink Even Further, Crypto Values Unprove... (cointelegraph.com)Analysts at JP Morgan have predicted that Bitcoin (BTC) could fall below $1,260, while banks will not benefit from blockchain for at least three to five years, Reuters reported on Jan. 24.

JP Morgan Analysts: Bitcoin Price Could Sink Even Further, Crypto Values Unprove... (cointelegraph.com)Analysts at JP Morgan have predicted that Bitcoin (BTC) could fall below $1,260, while banks will not benefit from blockchain for at least three to five years, Reuters reported on Jan. 24.

According to Reuters, analysts from the major global investment bank think that the true value of cryptos is still unproven, and that they only make sense in a hypothetical “dystopian” event, wherein investors have lost faith in major traditional assets like gold and the U.S. dollar. The analysts stated in a report:“Even in extreme scenarios such as a recession or financial crises, there are more liquid and less-complicated instruments for transacting, investing and hedging [than cryptocurrencies].”

JP Morgan also said that institutional involvement in the crypto market has slumped over the past six months, with individual traders making up the majority of the market. In its crypto report, the company claimed that using crypto for payments will remain “challenged,” adding that the firm was unable to find any major retailers that accepted crypto in 2018.

JP Morgan’s analysts have further suggested that Bitcoin is likely to drop to around $2,400, and could even fall below $1,260 if the current bear market persists. At press time, the biggest cryptocurrency is trading at $3,595, down around 1.7 over the past week, according to data from CoinMarketCap.

While JP Morgan forecasted that “widely-hyped” blockchain technology will not make any real difference for banks at least three to five years, the investment bank still concluded that distributed ledger technology (DLT) has potential to cut costs for global banks and digitize various complex processes.

JPMorgan CEO Jamie Dimon is vocally critical of cryptocurrencies, including Bitcoin, which he calleda “fraud” in September 2017.

While previously stating that he does not “really give a sh*t” about Bitcoin, he admits blockchain’s potential, saying, “Blockchain is real, it’s technology, but Bitcoin is not the same as a fiat currency.”-

Francisco Gimeno - BC Analyst Good news here. Crypto is not meant for speculation, and blockchain is yet in its infancy. There are many challenges yet and we needed to get rid of the over hype and the speculation both in crypto and blockchain. Crypto needs a better user friendly mode and more use cases, and blockchain protocols will grow stronger giving powerful solutions to many sectors. This is already coming.

-

-

CNBC Bitcoin News | Crypto valuations will increase, says Circle founder

CNBC Bitcoin News | Crypto valuations will increase, says Circle founder

Is Jeremy Allure right, are we near the bottom?-

Francisco Gimeno - BC Analyst Good words from Circle's founder: "Cryptographic tokens will represent every form of financial asset in the world." We understand that price is not everything in crypto, but its valuation. The market is here to stay and its long term is to deal with tokenisation of world finances. What do you think?

-

-

From banking to shipping to entertainment to higher education, industries are testing the revolutionary potential of blockchain technology. What sectors will pioneer the most radical advancements?

From banking to shipping to entertainment to higher education, industries are testing the revolutionary potential of blockchain technology. What sectors will pioneer the most radical advancements?

Which start-ups or established companies will lead them? And where are the investment opportunities?

Moderator

Garrick Hileman

Head of Research, Blockchain

Speakers

Jamie Burke

CEO, Outlier Ventures

Sally Eaves

CEO, Sustainable Asset Exchange (SAX), Forbes Technology Council and Professor of Advanced Technologies

Sean Kiernan

CEO, Dag Global

Ioana Surpateanu

Co-Head of European Government Affairs, Citi-

Admin

- 2 comments

- 6 likes

- Like

- Share

-

Jorn van Zwanenburg Blockchain researcher & Tokenomist Great panel discussion.

"platform monopolies have led to data monopolies which have led to AI monopolies." Dr Goertzel is trying to build what Jamie Burke is describing.

"In order to create large scale decentralized systems, you need three things: mechanisms of enforcement, incentive mechanisms and reputation mechanisms." -

Francisco Gimeno - BC Analyst Fantastic debate on blockchain already being seriously considered to transform business by very smart people in business, education and governments. It is very important to note how blockchain is being distinguished from all crypto as the important global and disrupting concept, where crypto is a central element for the tokenisation of digital economy.

-

-

The former chief economist of the International Monetary Fund (IMF) has characterized Bitcoin (BTC) as “a lottery ticket,” in an article for major United Kingdom daily broadsheet The Guardian Dec. 10.

The former chief economist of the International Monetary Fund (IMF) has characterized Bitcoin (BTC) as “a lottery ticket,” in an article for major United Kingdom daily broadsheet The Guardian Dec. 10.

Writing in the midst of the recent crypto market price collapse, current Harvard University Professor of Economics and Public Policy Kenneth Rogoff suggested that the “overwhelming sentiment” among crypto advocates is that the total “market capitalisation of cryptocurrencies could explode over the next five years, rising to $5-10 [trillion].

”The historic volatility of the emerging asset class, he conceded, indeed indicates that Bitcoin’s decline from its all-time highs of $20,000 to under $3,500 earlier today is “no reason to panic.”Nonetheless, the economist dismissed the “crypto evangelist” view of Bitcoin as digital gold, calling it “nutty,” stating its long-term value is “more likely to be $100 than $100,000.”

Rogoff argued that unlike physical gold, Bitcoin’s use is limited to transactions – making it purportedly more vulnerable to a bubble-like collapse. Additionally, the cryptocurrency’s energy-intensive verification process is “vastly less efficient” than systems that rely on “a trusted central authority like a central bank.

”Even if Bitcoin should not necessarily be “worth zero,” Rogoff argued that national governments and “regulators are gradually waking up to the fact that they cannot countenance large expensive-to-trace transaction technologies that facilitate tax evasion and criminal activity.

”This, in his view, places Bitcoin in a double bind, with implications for its future value: “take away near-anonymity and no one will want to use it; keep it and advanced-economy governments will not tolerate it.

”While the economist noted that governments worldwide may in due time “regulate and appropriate” the innovations of the new asset class –– as shown by the interest of multiple central banks in digital currency issuance –– he argued that coorinatinated global regulation would eventually seek to “stamp out privately constructed systems,” with only certain geopolitical outliers as a possible exception:“The right way to think about cryptocurrency coins is as lottery tickets that pay off in a dystopian future where they are used in rogue and failed states, or perhaps in countries where citizens have already lost all semblance of privacy. It is no coincidence that dysfunctional Venezuela is the first issuer of a state-backed cryptocurrency (the “petro”).”

Rogoff’s argument that “disgruntled” nation states –– Cuba, Iran, Libya, North Korea, Somalia, Syria, and Russia –– are turning to cryptocurrencies under the burden of sanctions has been raised by multiple analysts previously.

A report earlier this fall indicated that the government of North Korea was “laundering” crypto into fiat to evade U.S. sanctions. Iran is going one step further, exploring the creation of its own national cryptocurrency, according to a report this summer.-

Francisco Gimeno - BC Analyst In our eyes, the opinion of the article is one more to be read as an example of someone who has not fully understood what the digital economy is going to be. This won't be a different dog with the same collar and same owner, but a different way of doing things, a real digital and social revolution, which will come before than later and will surprise everyone.

-

-

A recent article in Barron’s describes Angus Champion de Crespigny, who spent ten years at professional services firm Ernst and Young and led the blockchain financial services division for years and was the subject of the article entitled “This Blockchain Believer Turned Heretic Is Still Bullish On Bitcoin,” as a “major skeptic.” Champion de Crespigny describes himself as an “experienced executive with 11 years in financial services, evangelist for bitcoin and cryptocurrencies, and a pragmatist for distributed and decentralized systems.

A recent article in Barron’s describes Angus Champion de Crespigny, who spent ten years at professional services firm Ernst and Young and led the blockchain financial services division for years and was the subject of the article entitled “This Blockchain Believer Turned Heretic Is Still Bullish On Bitcoin,” as a “major skeptic.” Champion de Crespigny describes himself as an “experienced executive with 11 years in financial services, evangelist for bitcoin and cryptocurrencies, and a pragmatist for distributed and decentralized systems.

”Through the course of the interview, Champion de Crespigny speaks on his learned experience regarding the blockchain and how it transformed him from a “believer” to his present state as a pessimist regarding the blockchain and what it can actually do for businesses. The article is quick to note that the former employee does not speak for EY – in a statement to the publication they said blockchains “really can provide value.”On its website, Ernst & Young claims an even more positive outlook on blockchain:Blockchain technology has the potential to universally reshape the way business transacts across nearly every industry in the global economy.

They note that their clients collectively have more than 50 blockchain-enabled products around the world. And as we recently reported here at CCN, EY and several other firms of similar nature have an insatiable need for blockchain experts. EY also very recently launched its own blockchain product.But Angus Champion de Crespigny, who was down in the trenches with the blockchain, isn’t so positive on it.

He left college the very year Bitcoin was finishing up development and was a very junior associate at EY when the Bitcoin blockchain first launched. EY obviously had no blockchain division at that time, and Champion de Crespigny took an interest in Bitcoin well in advance of the company taking an interest. As he told Barron’s:I got very involved in the community then, which was quite small. […] I started advising on regulatory considerations, which are now kind of commonplace. Over time at EY, as more and more clients were asking about it, I was more and more the go-to guy. We eventually formed a group. So while I was actively working on it starting in 2014, the group was really formalized in 2015.

He says he had a very optimistic view of the blockchain before and after the formal creation of a job advising on the financial aspects of it. “It would be silly for me to say otherwise. My views were aligned with a lot of the common views at the time. ”Champion de Crespigny describes the problematic nature of a public blockchain as regards the needs of private enterprise. In his view, from his experience, the usual problem was that of coordination on standards for a given blockchain product.[…] if everyone agrees on the standards—then it would be a great setup. In reality the process to get there is just incredibly, incredibly complicated. Typically, as it evolves, you end up having to coordinate everyone. And if you can coordinate everyone, then there is often a better technology to use than a blockchain.

Legal Contracts Over Smart Contracts

The rules of advanced, permissioned blockchains become “very, very complicated” when multiple entities need to make demands of them. Champion de Crespigny says that usually a central trusted entity is resorted to anyway, thereby defeating the purpose of “trustless” ledgers. He points out a known fact: centralized distributed ledgers are faster, and the reason they are faster is “because it is all built around a central controlling entity.

” The obvious counter-argument is that the central entity in charge of a centralized distributed ledger becomes an attack vector. But Champion de Crespigny addresses this as well, saying:You want a blockchain when you don’t know who you can trust, because you don’t want any one party being able to arbitrarily change those things. The thing is that in the business world, we have legal contracts to do that.

Perhaps the most pessimistic statement comes next: “People are now being sold a dream that a blockchain is going to be easier to do all of this, and I just don’t think that’s accurate. ”Headline Chasers and A Lack of Added Value

Champion de Crispigny says that some businesses would go with a blockchain even when he bluntly told them it was unnecessary or less efficient than traditional options such as Oracle. Companies would reportedly want to explore the technology, and EY would help them do so.

Then there is the hype factor – plenty of companies have dabbled in blockchain just to enter the current news cycle, which hardly does a full spin without some mention of crypto, blockchain, et cetera. As he says, “I won’t comment on specific companies, but there is a certain amount of headline chasing.

”As to cryptocurrencies themselves and the persistent view of many in traditional finance – “blockchain not Bitcoin” – Champion de Crispigny believes that Westerners discount the valuable role cryptos can play in the lives of people who don’t necessarily trust their local fiat currency.

Venezuela comes to mind.But as far as the blockchain fully revolutionizing every sector of business, Champion de Crispigny just doesn’t see it. “I didn’t see where private blockchains could create any value to business,” he says.

Featured image from Shutterstock

Get Exclusive Crypto Analysis by Professional Traders and Investors on Hacked.com. Sign up now and get the first month for free. Click here.-

Francisco Gimeno - BC Analyst Whoever is disillusioned by the blockchain as this stage will find a lot of reasons why. Blockchain evangelising gave a lot of big hopes and a huge hype has been built around it, selling blockchain as THE revolution. We use to say that blockchain is a tool, together with robotics, AI, etc, which should be used to lead the transition to the new digital economy and society of the 4th IR. The hype being over, the emperor naked, is time to really build use cases and work on the rapidly coming change. Blockchain is here to stay until another better tool comes (maybe quantum technologies?).

-

-

Cryptocurrency’s economic delusions are unravelling. None of Bitcoin’s utopian promises have come to pass, but regulators must stay vigilant.

By Lionel Laurent

Bitcoin turns 10 this year, but there’s not much to celebrate. Its price has tumbled to near $4,000, down 30 percent in a month, 50 percent in six months and almost 80 percent since December.

The cryptocurrency experts, who clearly didn’t see this coming, are blaming all sorts of temporary culprits — from jittery markets to “hard forks” (blockchain jargon for radical technical changes in a digital currency). But they’re kidding themselves. This is a long-term unraveling of all of the lies, exaggeration and populist fantasies that drove last year’s market mania.

Bitcoin was meant to make all of its investors rich, something that held particular appeal to a millennial generation hungry for a financial boost in a world of crushing student debt, income inequality and low-quality jobs. It was meant to be free of Wall Street’s corruption and the U.S. government’s meddling technocrats.

It was meant to be secure, with a price that would go ever higher. For the hardcore evangelists, it would reward its acolytes when the inevitable financial apocalypse arrived. The dollar was destined for scrap.And it was meant to show that we should all stop listening to fuddy-duddy “experts” like Jamie Dimon, Warren Buffett and Jack Bogle.

The old, closed ways of investing would be usurped by the buying power of the masses.

Unsurprisingly, none of this has come to pass. The Bitcoin bubble of 2017 — mercifully short and economically contained — has enriched only insiders such as mining companies and crypto-exchanges, and the early birds and tech elites who cashed in at the right time.

For the patsies who arrived late to the party, it has been a tool of financial impoverishment. About $700 billion has been wiped from the value of digital money since January. One Korean teacher told the New York Times in August: “I thought that cryptocurrencies would be the one and only breakthrough for ordinary hard-working people like us.”Destroyer of Value

Bitcoin and the cryptocurrency universe has been slumping since the end of last year

Nothing on the Bitcoin label turned out to be in the bottle. As a means of payment, it is cumbersome, volatile and expensive. It has destroyed value rather than storing it. Its decentralized technology was sold to investors as being unique.

It has been anything but.Those “hard forks” have created numerous Bitcoin spin-offs over the past year, and the vested interests of those who make money from doing this — by shifting their own coin to the new spin-off, bringing the miners along, and effectively taking control of the new currency — have triumphed over the dreams of a neutral blockchain system that would treat everybody equally.The Bitcoin Rich List

Cryptocurrency's gains are not evenly distributed

Even the hedge fund folk, who thought they could use sophisticated options to bet on the boom while covering their downside, have been proven wrong in a market where prices and information flow are not transparent — and are often manipulated.

Of course, bubbles and crashes are a part of history. If regulators and journalists do their job of warning consumers of the risks — and they did with Bitcoin — then why shouldn’t people be free to do what they like with their cash?

But while Bitcoin is on the ropes, it certainly hasn’t gone away, and global regulators still need to find an effective way to rein in the cowboys. And while this hasn’t been a systemic risk this time, the eventual spread of digital currencies will mean that isn’t always the case.

Finally, if the frustrations that drove people to chuck their savings at a virtual Ponzi scheme aren’t resolved, we’re only setting ourselves up for bigger political trouble down the line.This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Lionel Laurent at [email protected]

To contact the editor responsible for this story:

James Boxell at [email protected]-

Francisco Gimeno - BC Analyst We love this article. This will be one to be read again at the end of 2020 as an example of very poor research. The author looks like unable to understand markets, and the long term idea of bitcoin and what it means as a disruptive idea to change the financial world and with it the whole society. It is not the dream of an anarchist utopian only, but a force to reckon in the present and next future.

-